That’s the question asked by the ABC’s Daniel Ziffer in the segment above.

Ziffer’s accompanying article highlights the problem awaiting the housing market and economy:

‘Extend and pretend’

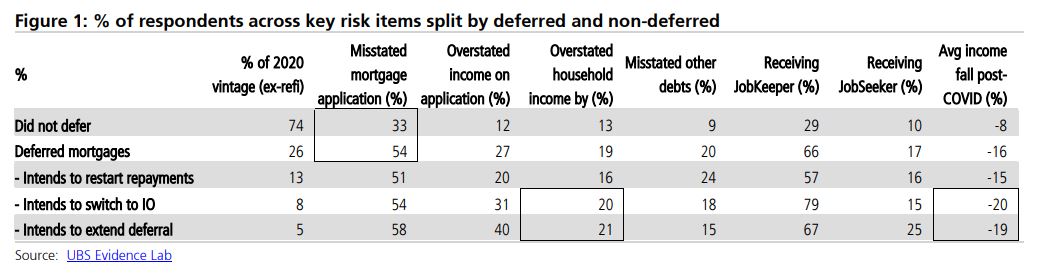

The good news is that almost half of customers who deferred mortgages intend to revert to normal payments, according to new data from banking analysts at UBS.

An anonymous survey of almost 1,000 people with a mortgage found a further third intend to switch to interest-only payments, meaning they will be “servicing” the loan but will not be reducing the capital amount they owe.

But one-in-five intend to extend the deferral. And it gets worse from there.

“The credit quality of customers intending to ask their bank to extend their deferral is concerning,” the report noted.

“Of these customers we found: 40 per cent overstated their income in their mortgage application; 15 per cent understated other debts; 67 per cent are on [wage subsidy] JobKeeper; 25 per cent are on [unemployment benefit] JobSeeker.”

Both JobSeeker and JobKeeper are about to be trimmed back.

For those on JobSeeker, it means their income will drop from $558 to $408 a week.

The full-time JobKeeper rate falls from $1,500 to $1,200 a fortnight and a part-time rate is being introduced that will halve payments for those working less than 20 hours a week..

That is a big issue, because incomes have already been smashed by the coronavirus crisis and the recession.

Customers who deferred mortgages were already much more likely to have lost income. That means customers who overstated their income on their original application are now in a much worse position than their bank potentially understands.

JobKeeper changes are now set in stone

“An overstatement of income by around 20 per cent would suggest that their income is around 40 per cent lower than the banks had expected since the mortgage had been taken out,” the report warned.

UBS is suggesting a practice called “extend-and-pretend” could be the best option, essentially kicking the problem further down the road and hoping things improve.

It is urging banks to do “significant due diligence” before extending deferrals or moving people to interest-only loans.

That is because many borrowers are “likely to be under more stress than the banks perceive” and many “should be considered delinquent, in our view.”

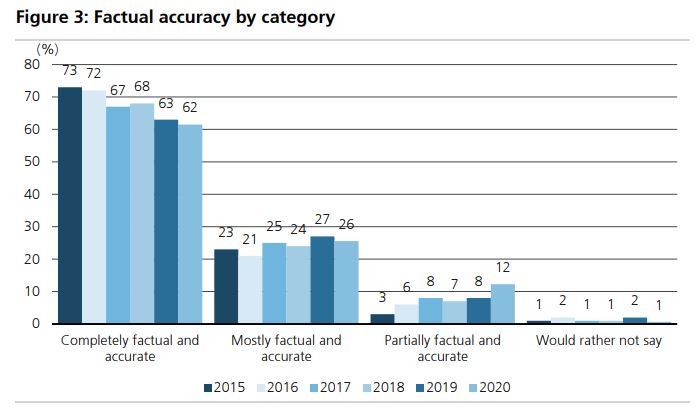

‘Factually inaccurate’ mortgagors – higher credit risk now being seen

We found the credit quality of the home buyers (‘front book’) in the survey is weaker than data shown by both the banks and APRA (‘back-book’). This is in-line with expectations as home buyers (survey excludes refi) are more likely to be younger and more highly leveraged than the book as a whole. Once again, we found 37% of the sample stated their mortgage application was not “completely factual and accurate”, a level consistent with the previous five vintages. Of more concern, the credit quality of customers who misstated their mortgage were significantly weaker than truthful customers. We found that factually inaccurate mortgagors: (1) have seen household income fall an average of 13%; (2) 36% have deferred repayments; (3) 66% have a household member on JobKeeper/JobSeeker; (4) 71% withdrew Superannuation.

What do deferred mortgagors intend to do? How stressed are they?

As the bulk of mortgagors approach the end of their six month deferral period, we found: 47% of deferred mortgagors intend to revert to normal payments; 32% intend to switch to Interest Only (IO); 21% intend to ask to extend deferral. However, the credit quality of customers intending to ask their bank to extend their deferral is concerning. Of these customers we found: (1) 40% overstated their income in their mortgage application (by 21% on average); (2) 15% understated other debts; (3) 67% are on JobKeeper; (4) 25% are on JobSeeker; (5) They have seen their income fall 19% since COVID on average (in addition to the amount they overstated). Unfortunately, we found the financial position of those asking to move to IO is only marginally better.

“Extend-and-pretend” may not be the best option

The 2020 survey illustrates factually inaccurate mortgages are materially higher credit risk. APRA has stated mortgage deferrals should only be extended on a case-by-case basis. We believe the banks need to undertake significant due diligence before extending deferrals or moving deferred customers to IO, as a large number of these borrowers are likely to be under more stress than the banks perceive. Many of these customers should be considered delinquent, in our view. Given this stress, a recovery in employment and house prices is critical to the banks’ performance.

According to APRA’s latest mortgage deferral data, there were 393,467 mortgages were deferred as at 31 August, accounting for 7% of total mortgage facilities.

Thus, if UBS’ estimates are correct and one-in-five intend to extend the deferral, then that’s around 80,000 mortgage borrowers that are struggling financially.

Advertisement

If a significant number of these borrowers are eventually forced to sell, then this could place significant downward pressure on property values.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.