Australia’s mortgage cliff still towers over property market

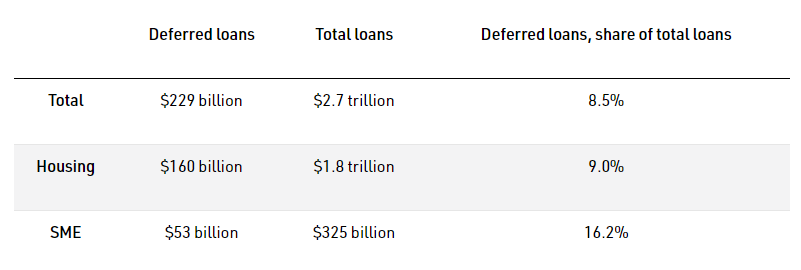

The Australian Prudential Regulatory Authority (APRA) has updated its statistics on Australian loan repayment deferrals, which reveals that there were still $229 billion loans outstanding as at 31 August, accounting for 8.5% of total loans outstanding by value:

Of these, $160 billion of deferred loans were mortgages, accounting for 9.0% of total mortgages outstanding.

In number terms, 393,467 mortgages were deferred as at 31 August, accounting for 7% of total mortgage facilities.

In early September, Australian Bankers Association (ABA) CEO, Anna Bligh, announced that banks would commence “the largest ever customer contact process in the industry’s history” as it seeks to contact around 400,000 customers that have deferred repayments.

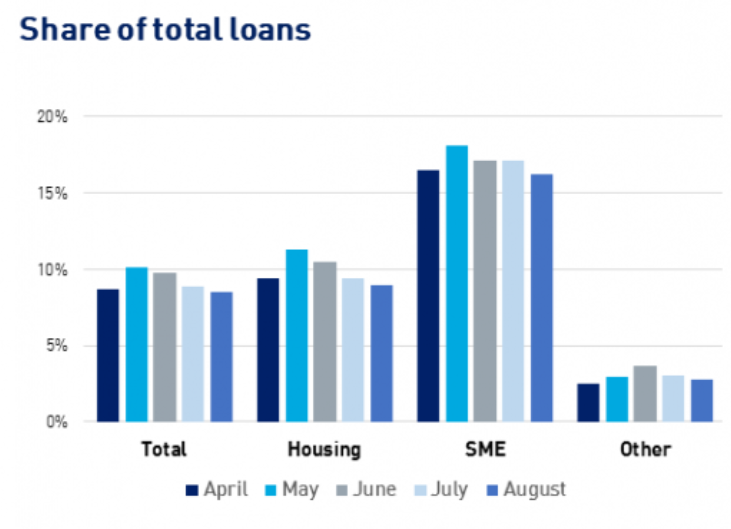

It appears from this data that banks are having difficulty getting customers to recommence payments given the value of mortgages deferred only declined by $7 billion between July and August, from $167 billion to $160 billion. In a similar vein, the number mortgage deferred only declined by around 21,000, from 414,430 in July to 393,467 in August.

In fact, the share of mortgages deferred was roughly the same as at 31 August (9.0%) as it was when the pandemic began in April (also 9.0%):

The Australian Prudential Regulatory Authority has permitted banks to extend mortgage repayment relief until March 2021. But banks are still required to ascertain from borrowers whether they are in a financial position to commence repayments.

Thus, large numbers of deferred mortgages could hang over the housing market and economy for another six months.

This creates a potential ‘perfect storm’. In addition to the expiry of mortgage repayment holidays, emergency income support (JobKeeper and the JobSeeker supplement), early access to superannuation, and the moratorium on personal insolvencies and bankruptcies are all scheduled to end. Although, these too could be extended.