Why the RBA doesn’t care about the property bubble

From Karen Maley at the AFR today:

…”To the extent that an easing of monetary policy helps people gets jobs, it will help private-sector balance sheets and lessen the number of problem loans. In doing so, it can reduce financial stability risks,” Lowe argued.

…Other economists point out that a further drop in home loan borrowing costs will probably provide a further support for housing prices, even as the banks progressively wean people off their loan repayment deferrals.

…Robust house prices boost overall financial stability because it means Australian banks will probably suffer fewer losses from home loan defaults.

Economists point out that although the RBA clearly sees the potential for further monetary easing to push house prices higher, it doesn’t seem too concerned about the possibility of prices rising too sharply.

That is because the pandemic has unleashed structural changes in the market, which will probably keep investors on the sidelines for several years.

There is one other reason that the RBA isn’t worried about house prices. That’s not its job. The responsibility passed implicitly to APRA in the last cycle when it deployed macroprudential tools to end the price boom. APRA’s intervention was triggered by exactly the same conditions we face today, the combination of weak economic growth and an overly high currency pushed up by other central bank easing.

Again the AFR can’t bring itself to discuss this fundamental change and tenet of Australian monetary policymaking, preferring the dated and silly game of RBA-watching, even though it now has a total of 25bps left to cut (until it goes negative, as it eventually will).

It’s freakin’ ridiculous. There are so many unanswered questions about APRA’s new role in monetary policy it’s crazy. Why wouldn’t a journalist ask them? Should it be rejoined with the RBA? Why has APRA been allowed to exist in such secrecy? Why has it survived the Hayne RC humiliation without a scratch? What are the new tools that it will eventually deploy? What are the triggers to deploy them? How do other central banks do it? What is the endgame of this new monetary structure?

It’s like everybody has dropped monetary Mogodon at the AFR.

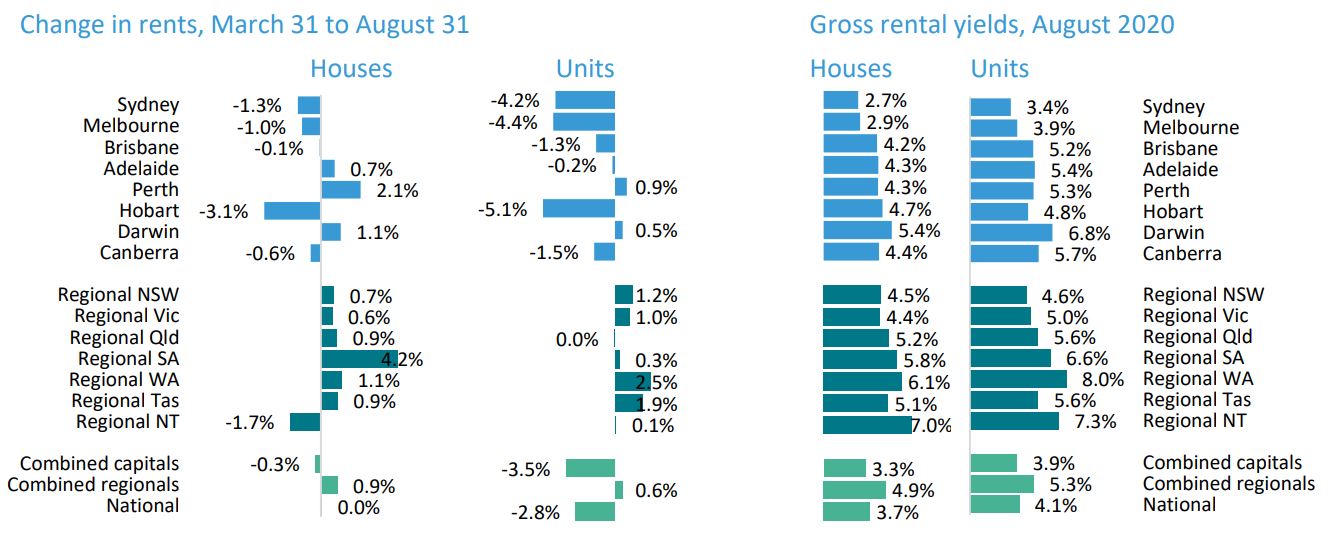

Anyways, I more or less agree with the conclusions of the piece. I don’t expect investors to rip back in when rents are crashing and there is no demand from the migration segment. But that is a Sydney and Melbourne argument. Other, less migration dependent cities, which also happen to be in the non-virus zones, will see rising owner-occupier and investor demand. Especially since they offer much better demand and supply balances and decent yields, as well as possible rental growth. There’s plenty of room to make these yields uneconomic yet too:

This means that both the RBA and APRA will remain on the sidelines in terms of tightening for the foreseeable future.