Back in 2016, Australian economics titan, Tim Toohey, forecast a new Australian boom:

Goldman Sachs has upgraded its Australian dollar and economic growth forecasts.

“As we look out to 2017 and beyond, we believe Australia has moved through an important transition point and with it has emerged the prospect of stronger and less volatile real economic growth,” GS economist Tim Toohey says.

Mining to be a driver in the 2017 growth equation for Goldman Sachs.

He now expects 78, 77 and 75 US cents for the Australian dollar on a three, six and twelve-month horizon. He also expects GDP to average 2.8 per cent in 2017, 2.9 per cent in 2018, 3.0 per cent in 2019 and 3.3 per cent in 2020.

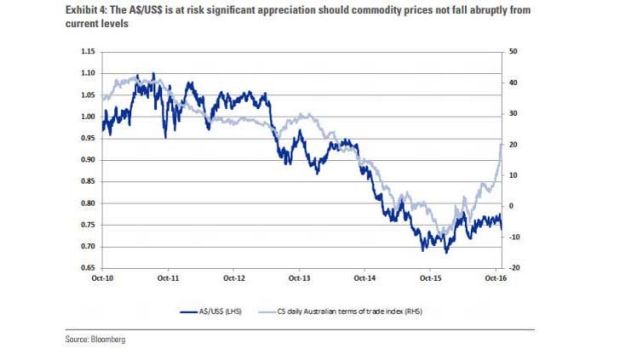

“A sharp turn in Australia’s national income dynamic now looks likely to move significantly higher following the spikes in coal and iron ore prices in the closing months of 2016,” the Toohey says.

While he expects bulk commodity prices to fall from current levels, Toohey says the recent surge has transformed his expectation for a modest rise in Australia’s terms of trade in 2017 to a material 8 per cent gain with most of the export price spike to be registered in late 2016 andearly 2017.

“This is likely to set off a chain of events through the Australian economy in coming months,” Toohey adds.

“The resulting surge in national income should be reflected via much stronger mining profits, a large taxation windfall for the Federal government and elimination of the threat of a sovereign downgrade, a restarting of idle capacity in the coal sector, a better climate for broader business investment and ultimately better employment and wage outcomes. It also sows the seeds for a more material handover of the economic growth baton to the private sector, and importantly this transition can proceed despite our forecast of a sharp decline in new dwelling investment in 2017-18. Perhaps the most dramatic transformation will come via Australia’s external accounts with a run of trade surpluses now in prospect for 2017 – indeed the combination stronger commodity prices and the ramp-up of LNG production suggests Australia will post the largest trade surpluses as a share of GDP during 2017 since any time since the early 1970s. Ultimately the state of the external accounts is the truth serum for the currency, and as such we acknowledge clear upside risk to the A$ from current levels.”

Toohey continues to forecast that the RBA will commence increasing interest rates in 1Q18, but says the skew is now towards an earlier kick-off in 2H17.

As I said then:

Readers will know that I have a lot of time for Tim Toohey. But I cannot agree here. The bulk commodity surge has a kernel of truth to it but most of it is bubble and will reverse by mid next year with rebounding supply, plateauing Chinese demand, diminishing speculation and the USD headwind.

Moreover, although national income is going to get a nice boost, the channels that usually operate to spread it across the economy – mining dividends, Federal government tax take and rising wages via increased investment – are this time much more limited. Only the first is set to grow this time given the government will still be under pressure to rein unaltered deficits and there will be very little new investment in iron ore or coal. In fact, broader mining investment will keep on falling.

Given the dwelling boom will begin to roll over late next year, and vehicle assembly shuts as well, what part of the private sector is going to take up the “growth baton”? What is going to tighten up the soggy labour market and turn wage deflation?

The only thing is tradables and they’ll need a lower dollar and more rate cuts.

Then, late last year as COVID-19 bubbled away in China, Tim Toohey declared another new Australian boom:

Advertisement

“We’re going to see another 12 to 18 months of an upswing here,” he said.

“The financial markets have been obsessing about 2020 being the year of the global recession but that veil’s been lifted.”

“The rate of change in [quantitative easing] shows very clearly that there was a very dramatic revision, or dramatic withdrawal, of US dollar liquidity from the central banks from the early part of 2018 through to the very recent period,” he said.

As I said then:

I won’t say it isn’t possible. It is. There are three reasons to see an upswing ahead:

central bank liqudity;

easing trade tensions, and

rebounding US property driving global restocking.

The problem is that there are serious headwinds to each as well:

ECB, PBOC (and BOJ) liquidity rebounds are weak;

easing trade tensions rest on the very shaky assumption that a Hong Kong daisy cutter falling through a clear blue sky won’t land, and

global restocking will be inhibited by tarrifs.

Once we factor in these VERY obvious risks then Tim Toohey’s statement that “the worst of the cycle is behind us, the stimulus that’s in place is important, data is improving” becomes nothing more than a large leap of faith.

Yes, if geopolitics calms down then growth will improve. IF. Tim Toohey clearly has no special insight into that, except to ignore it, which rather suggests the opposite.

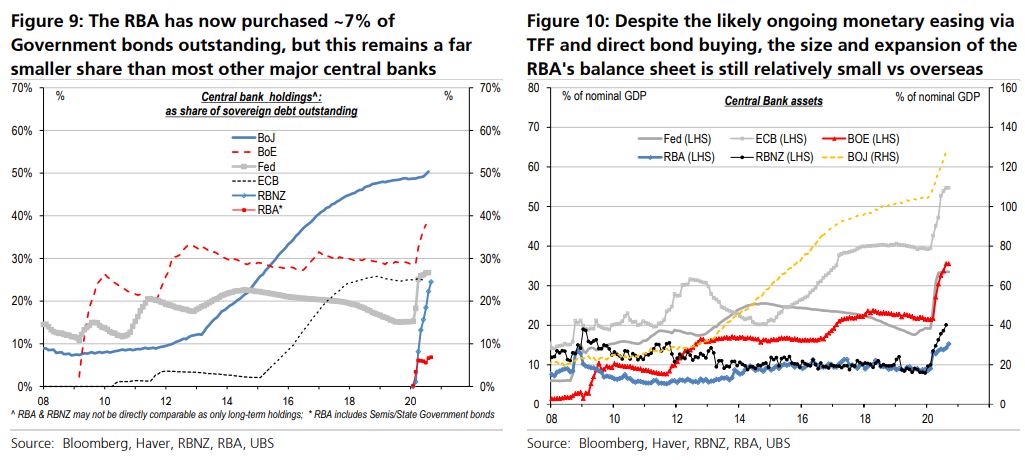

“Governor Lowe directly linked targeting relative long-dated bond yields, relative size of quantitative QE programs between countries and the exchange rate.

…”In the context of the history of Australian monetary policy, that is quite a big deal.”

“Perhaps I’m old-fashioned, but different financial prices for sovereign bonds tend to be associated with different views on the relative fundamental outlook for that economy, even in the presence of QE,” Mr Toohey said.

“A slightly more optimistic view on Australia’s economic prospects can easily be made vis-à-vis the rest of the G7 currently, and it’s hardly surprising that Australian 10-year yields would be slightly higher.

“Trying to design a policy framework to align 10-year yields relative to other countries looks cumbersome. It is debatable what real economic benefit this is really providing.”

It’s not old fashioned, Tim, it’s dated. Why? Five reasons.

First, the RBA is not benchmarked versus other countries. Its goals are Australian jobs and inflation. It failed on this for an entire cycle, thanks to exactly the kind of dated thinking represented in this article.

Advertisement

Second, a lower Aussie dollar provides an enormous stimulatory boost. It lifts commodity revenue and federal taxes, forces more local spending, lifts competitiveness, exports, imports-competers, jobs and inflation. That’s 40% of the economy given a rev-up. What’s not love for the central bank?

Third, a lower Australian dollar helps restructure the economy away from the demand drivers of domestic credit demand and towards tradables helping to offset the rather obvious and rapidly growing geopolitical gale that is Chinese decoupling.

Fourth, Australian growth prospects are not better than elsewhere. They are worse as we hit peak household credit, population bust, a staggeringly deflationary budget and Chinese decoupling all at once.

Advertisement

Fifth, the major reason we had a steeper yield curve is we were the only one not targeting the long end of the bond curve with QE, nor doing enough of it per se:

The RBA has indeed joined the global currency war and thank god for it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.