With Australia’s property market now declining for five consecutive months, it’s once again time to compare the current downturn with prior corrections.

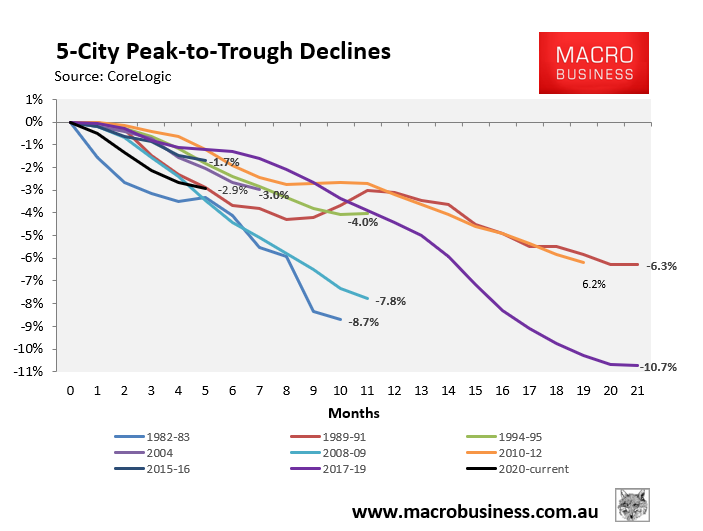

The below chart shows the various dwelling corrections over the past 30-plus years at the 5-city level, as measured by CoreLogic:

As you can see, this correction is so far only mild, with the property market so far falling just 2.9% over five months. Property values across the five major capitals are also falling at their equal third fasted rate on record, behind the 1982-83 and 2008-09 corrections but equal to 1989-91.

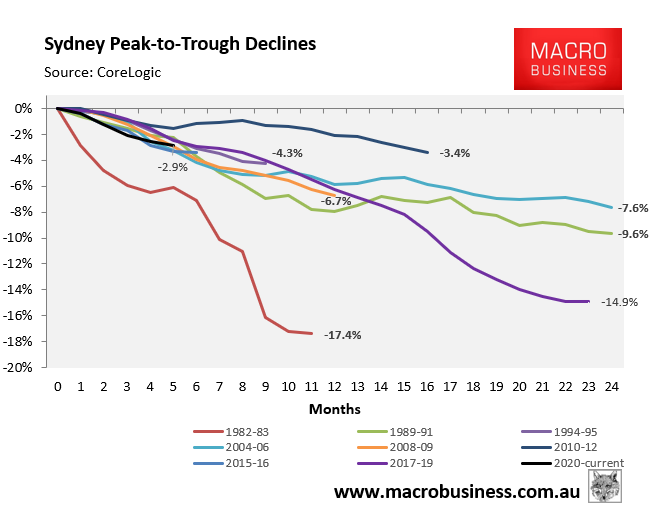

Next is Sydney, whose 2.9% correction has also only been running for five months. Its pace of decline is fairly mild around the middle of the pack:

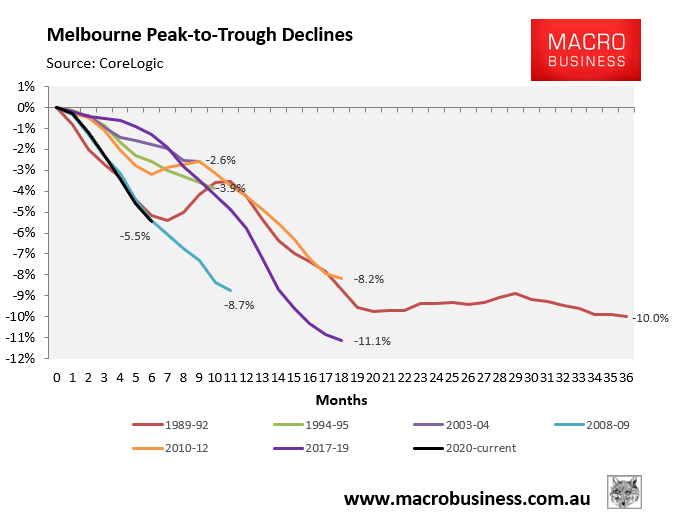

However, Melbourne’s 5.5% correction has been running for six months and is the equal steepest on record, on par with the 2008-09 GFC:

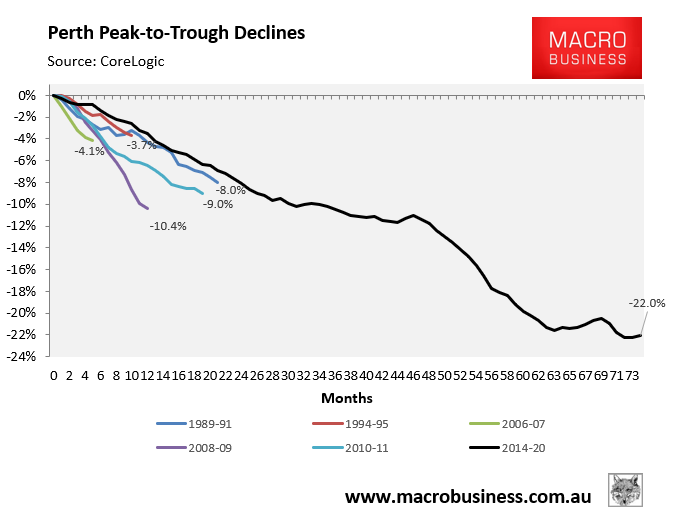

Finally, Perth’s housing market has been in decline for 74 months (~six years), give or take some monthly rises along the way. Perth dwelling values were tracking 22.0% from peak at 30 September – the biggest correction in history:

In forecasting falling property prices this year and next we have been working off the assumption that mortgage rates had bottomed and, as a result, future price growth would need to come from rising household incomes.

So, with net overseas migration crashing alongside high unemployment and the unwinding of emergency income supports, it seemed logical that house prices would fall significantly in Sydney and Melbourne, dragging national values lower (even with modest growth in the smaller capitals).

However, Josh Frydenberg’s recent announcement that he would abolish responsible lending laws was a policy ‘black swan’ and a potential game changer. If qualifying borrowers are permitted to borrow more and previously non-qualifying (sub-prime) borrowers are pulled into the market, alongside the RBA monetising the banks mortgage debt, then this could lead to national property price increases in 2021 as mortgage rates edge lower still and the banks lend to anybody with a pulse.

The upshot is that Australia’s housing market now represents a tug-of-war of war between lower interest rates and easier credit availability on the one side (positive for prices) and collapsing immigration, high unemployment, and unwinding of emergency policy support on the other (negative for prices).

It is already clear that this will lead to a bifurcated market with smaller non-virus capitals prices rising as Sydney struggles and Melbourne falls. There is also a split between all capitals inner-property, and their surrounding rural districts, as work from home becomes the new black post-COVID.

The scale has clearly been tipped in favour of rising prices thanks to Josh Frydenberg’s abolition of responsible lending rules and the likelihood that the RBA will seek to crunch mortgage rates to 1%, which has brightened the outlook for Australia’s property market.