Will The Empty Chair block Frydenprime?

Via the ABC:

“Flabbergasted.” That’s the universal response I’ve been hearing from consumer rights advocates to the Federal Government’s proposed abolition of the responsible lending obligations.

They simply can’t understand what the Government is aiming to achieve by freeing banks from their legal obligation to check whether potential borrowers can afford to repay a loan before they are granted it.

Other than a free kick for the banks.

“As we learnt to our cost during the GFC, weaker lending standards mean people will be loaded up with as much debt as possible. There is significant profit to be made in pushing borrowers to the edge,” said Financial Counselling Australia’s Fiona Guthrie.

Guthrie’s organisation helps thousands of Australians every year to pick up the pieces of their financially shattered lives, often after being approved for loans or credit cards they could never hope to afford.

The part of the law that the Government proposes to excise was written a bit over a decade ago to prevent exactly that.

Put simply, it requires lenders to check how much a potential borrower is earning and how much they’re spending and whether there’s enough left over to make their repayments without “substantial hardship”.

‘A solution in search of a problem’

Except that, since being legislated in 2009 it had never really been enforced, at least not against the mainstream lenders. At least until March 1, 2017.

That’s when the corporate regulator ASIC launched a test case against Westpac, alleging that its widespread practice of using a blanket — and many argue low-ball — living expenses benchmark for hundreds of thousands of home loan approvals didn’t cut the mustard.

But the Government isn’t changing the law because Westpac lost.

The bank not only won its initial case, but also an appeal to the full bench of the Federal Court. It could continue using its benchmark, and ASIC opted not to appeal to the High Court.

(Today, perhaps, we found out why. After all, why bother appealing to clarify a law you found out was going to be soon abolished anyway.)

As the Consumer Action Law Centre observed, the Government’s proposed changes to the National Consumer Credit Protection Act are “a solution in search of a problem”.

Treasurer Josh Frydenberg said the changes are designed to “increase the flow of credit to households and businesses”.

But it’s far from apparent that there’s any problem with the flow of credit at the moment.

“The Commonwealth Bank recently said that the flow of credit is above pre-COVID levels and that lending is growing at a strong pace,” noted the Consumer Action Law Centre’s CEO Gerard Brody.

“And none of the big banks opposed the responsible lending laws at the recent House of Representatives Economics Committee hearings.”

CALC and other consumer rights groups also point out that, under the National Credit Act, the responsible lending obligations do not apply to small businesses, a point ASIC also recently made.

To support his case, the Treasurer cited recent testimony from the Reserve Bank governor Philip Lowe at a parliamentary hearing.

“The pendulum has probably swung a bit too far to blaming the bank if a loan goes bad because the bank didn’t understand the customer,” Dr Lowe said.

It is, however, very uncertain that the RBA governor’s solution to the pendulum swinging “a bit too far” would be to hack it off altogether.

Indeed, while noting that credit growth to households was slowing, minutes from the RBA’s most recent meeting didn’t attribute that to any difficulties in getting loan approval.

“This largely reflected reduced demand from borrowers, given the weak and uncertain economic environment and its effect on the housing market,” the board observed.

Hayne train derailed

Moreover, Josh Frydenberg’s own department doesn’t, or at least didn’t in 2018, buy into the argument that responsible lending obligations hurt the economy.

Who was quoting Treasury? Banking royal commissioner Kenneth Hayne, in his final report.

In fact, in its submission in response to Mr Hayne’s interim report, Treasury said not giving loans to people who probably couldn’t afford them was likely to be good for the economy.

“Appropriately managed, ensuring the industry consistently meets the requirements of existing laws will likely enhance rather than detract from macroeconomic performance.”

Testifying before Mr Hayne’s commission, CBA boss Matt Comyn also expressed few concerns about the responsible lending laws, saying his bank was working hard to reduce its reliance on the Household Expenditure Measure – the HEM benchmark that had landed Westpac in court with ASIC.

‘Apply the law as it stands’

In its press release welcoming the announcement, the Australian Banker’s Association made the Orwellian claim that:

“The banking royal commission identified the need to simplify the regulatory landscape. This proposed reform removes duplication and overlap between regulators while continuing to ensure strong protections for consumers.”

But Mr Hayne’s recommendation about what to do with the responsible lending obligations was simple.

Because the ASIC v Westpac case was still running at the time, it wasn’t entirely clear where the law stood and Mr Hayne — a former High Court judge — didn’t want to pre-empt the Federal Court’s decision.

However, he basically said in his final report that if ASIC lost then legislators should consider changing the law — but to tighten the obligations on banks, not loosen them.

“If the court processes were to reveal some deficiency in the law’s requirements to make reasonable inquiries about, and verify, the consumer’s financial situation, amending legislation to fill in that gap should be enacted as soon as reasonably practicable.”

Mr Hayne’s recommendation is strengthened by the fact that artificial intelligence technologies combined with open banking rules that let customers authorise the sharing of their financial data between institutions now make it easier than ever for banks to quickly and cheaply automatically check and verify their customers’ financial positions.

What will the changes mean?

There’s no doubt the removal of responsible lending obligations should make it easier to get a loan in the short term, once it comes into effect in March 2021, if passed by Parliament.

You might think that will make it easier for first home buyers to buy a house, but that won’t necessarily be the case.

To use a personal example, we bought our home in 2018, just after the royal commission hearings and while ASIC’s Westpac loan case was still in court.

It was when banks were demanding a lot more detail about your income and, particularly, expenses. It took a few hours of going through pay slips, bank and credit card statements to get the information together.

The trade-off was that, as people with relatively steady jobs and reasonable savings, we ultimately had few problems getting a loan approval but some other people, including some property investors, obviously did.

The number of people at open homes dropped dramatically and, as a result, prices were falling.

Any move to relax lending restrictions will have the opposite effect.

While it will be easier for you to get a loan, it will also be easier for a lot of other people to borrow more money.

More competition and bigger loans equals higher home prices. That means even if you end up winning at auction, you’ll likely be left with a larger debt and higher interest repayments.

Which leads us to the broader economic problem.

Australian households are already the second most indebted in the world after the Swiss.

If these changes, as the Treasurer says, make it easier to borrow and increase the flow of loans they may temporarily boost economic growth but will do so by increasing household debt even further.

Ultimately, all that does is set Australia up for a future financial crisis and recession.

And, if that does happen, the banks will be in deep financial trouble.

That’s OK for them, because they have both an explicit Government guarantee on deposits and an unwritten guarantee that at least the big four will be bailed out by the taxpayer if they look like falling over (that’s something factored in to the credit ratings of the major banks by all the major global agencies, who peg the big banks’ ratings to that of the Australian Government).

But it does mean a future Federal Government — and us as taxpayers — might have to pick up the tab for bank failures, possibly while still paying off the cost of coronavirus.

It’s a case of personal responsibility but community liability.

So, while it might be a nice intellectual argument to say borrowers should be more responsible for how much debt they take on, unless we remove those bank guarantees, there’s a strong argument that the public, through the nation’s laws, should have some say in how banks are handing out loans.

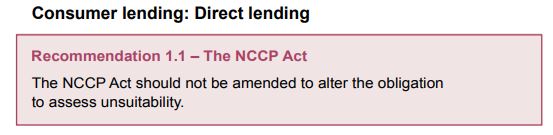

Here is the NUMBER ONE recommendation of the Hayne Royal Commission:

That is precisely what Frydenprime is proposing to do.

So, this maniacal policy idea:

- trashes Labor’s Hayne Royal Commission legacy;

- trashes Labor’s responsible lending laws;

- intrinsically ravages the core Labor constituencies of youth and working classes, and

- is a clearly corrupt endeavour to restore Coalition mates in blood-sucking banks to criminal lending.

Yet I have no idea how The Empty Chair is going to respond. All we got over the weekend was dishwater from Shadow Treasurer Jim Chalmers:

“We want to see households and businesses get sufficient access to finance but we don’t want consumers caught in debt traps or the balance tipped back in favour of shonky lenders,” Dr Chalmers said. “The government has form when it comes to going easy on the banks and loan sharks.”

Labor said Commissioner Kenneth Hayne’s first recommendation in the final banking royal commission report said the government should not amend the National Consumer Credit Protection Act’s obligation to assess unsuitability.

Dr Chalmers said Labor would examine the proposed legislation closely before deciding whether to support it.

Greens senator Nick McKim said the Greens would look for support in the Senate to stop the changes getting through.”The day after Westpac received the largest corporate penalty in Australian history, the government is changing the rules to benefit the banks,” he said. “Looser lending standards will result in higher profits, higher dividends, and more money flowing into the most overpriced housing in the world.

“This is not the pathway to recovery.”

No, it is not. Yet the fire in Labor appears to have gone entirely out as it “small targets” itself into oblivion.