Via UBS:

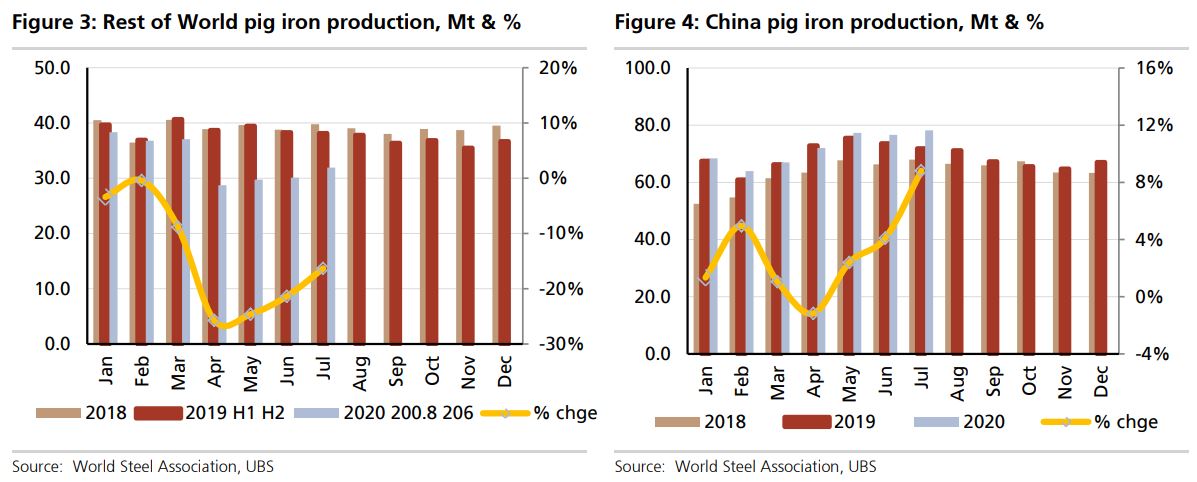

Will the restart of blast furnaces ex-China impact iron ore demand in 2H h/h?

No. Over the last month a number of steel producers have restarted BFs which were hot-idled due to COVID-19. We estimate in total ~22 BFs are being restarted around the world or ~30% of the total idled. In our opinion, this is not a surprise given the time-constraints of hot idling & as demand is picking up. We expect most idled BFs to restart by end-20; this is needed for pig iron production ex-China to be flat h/h in 2H.