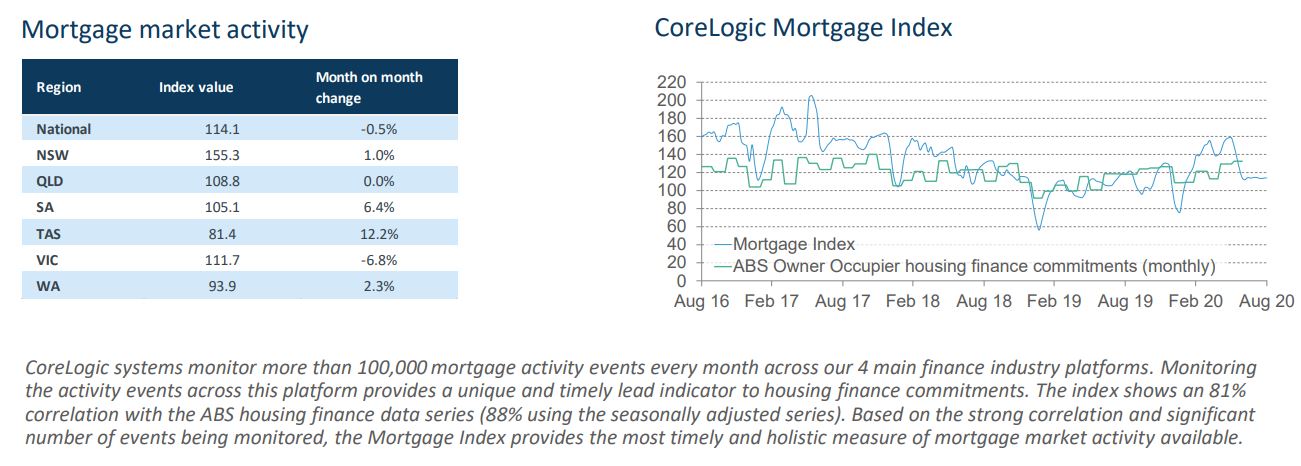

Via CoreLogic weekly indicators. Leading mortgages for owner-occupiers have no pulse, down materially year on year and flatlined:

Weak listings are some support for prices but for how long as we go over the fiscal and prudential cliffs:

Advertisement

Does anyone doubt that if the RBA had any kind of power left in the monetary defibrillator then it would be complusively jerking the trigger? Full report.