Industry Super Australia (ISA) commissioned modelling by actuaries Rice Warner, which shows that freezing the compulsory superannuation guarantee (SG) at 9.5% would cost the federal budget over the long-term:

Freezing the rate at which employers contribute to superannuation would cost the federal government billions of dollars in the long term, modelling by actuaries Rice Warner shows.

The modelling, conducted for the industry super sector, shows that a freeze at the current rate of 9.5% of wages would bolster the budget in the short term, but by the mid-2040s this would be outweighed by the increased cost of pension payments…

In its report, Rice Warner said that freezing the super guarantee at 9.5% “would have a modest budget benefit in the short term through higher taxation revenue but this will be offset over time by lower superannuation earnings tax and increased age pension expenditure with a net negative budget impact evident after 25 years”…

The deputy chief executive of Industry Super Australia, Matt Linden, said critics of the super system often talked about the large cost to the budget of the tax concessions given to super savings.

“But they’re not taking into account that without compulsory savings and the provision of this private savings pool in fact government would be on the hook for a much higher level of publicly funded pension, and that’s the experience overseas,” he said.

You know what they say about economic modelling: garbage in, garbage out. Obviously, any modelling commissioned by ISA would support the group’s position and cannot be considered impartial.

This is an important point because previous modelling by Rice Warner showed unambiguously that lifting the SG would cost the federal budget over both the short and long-term:

Advertisement

Our modelling shows that the legislated increase in the SG will not have much impact on the Age Pension for many years but will reduce it by about 0.1% of GDP in the second half of this century on current means testing settings. Conversely, the tax concessions from the increase are more immediate and they will average about 0.22% of GDP throughout this century.

In other words, the federal government wouldn’t break even on compulsory superannuation until well into the 22nd century. Hardly sound like a wise policy, does it?

Let’s also remember that impartial modelling from the Grattan Institute also showed that “both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments”:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

Advertisement

Seriously, where is the sense in raising the SG when we know that, because of the 15% flat tax on contributions/earnings, the lion’s share of benefits will flow to higher income earners?

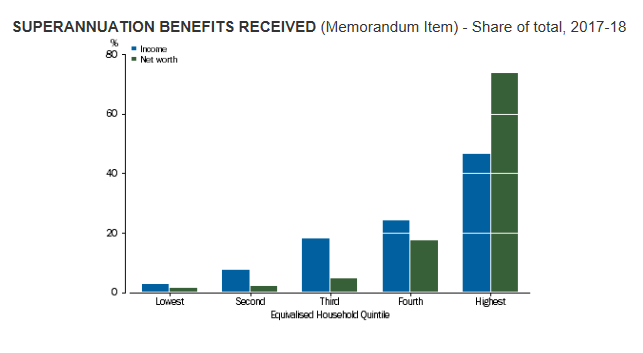

In 2017-18, total household superannuation benefits received was $112,009m. Households in the highest income and net worth quintile received 47% and 74% of total household superannuation benefits, by comparison households in the lowest income and net worth quintile received 3% and 2% of total household superannuation benefits. There was an increase in the share of total household superannuation benefits received by households in each quintile from the lowest to the highest for both income and net worth quintiles, with the increase being particularly steep from the fourth to the highest net worth quintiles. The ratio of the value of the highest to lowest quintiles was 15.5 and 45.7 for income and net worth quintiles for superannuation benefits received.

Advertisement

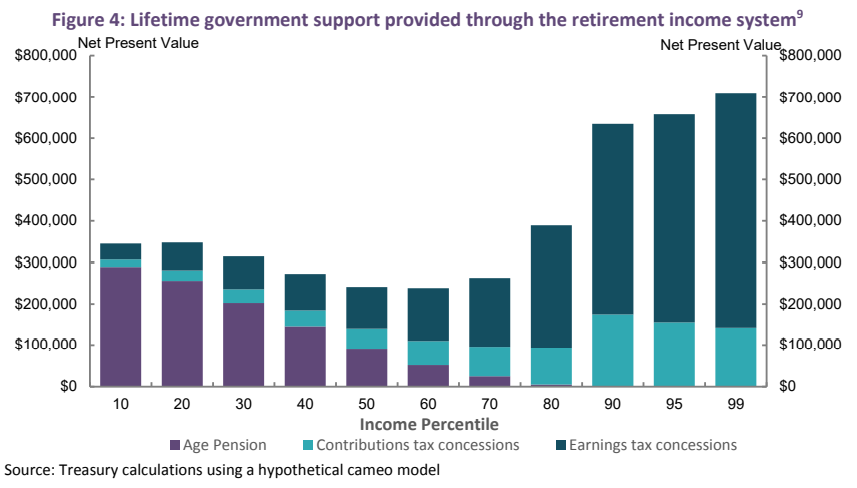

As does the next chart from the Australian Treasury, which shows that higher income earners receive a disproportionate share of superannuation concessions:

As shown above, the top 1% of earners are projected by the Treasury to receive more than $700,000 in superannuation concessions over their working lives, which dwarfs the $50,000 of concessions received by the bottom 10% of income earners.

Advertisement

Accordingly, Australia’s compulsory superannuation system is actually enshrining inequality by concentrating asset ownership among the wealthy.

For these reasons, Australia’s superannuation system is really more of a tax avoidance scheme for the rich than a genuine retirement pillar.

Rather than blindly raising the SG, superannuation concessions should be made more progressive. This way, low income workers could enjoy a boost in their retirement savings without also incurring a reduction in their take home pay and destroying the federal budget, while also improving equity.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.