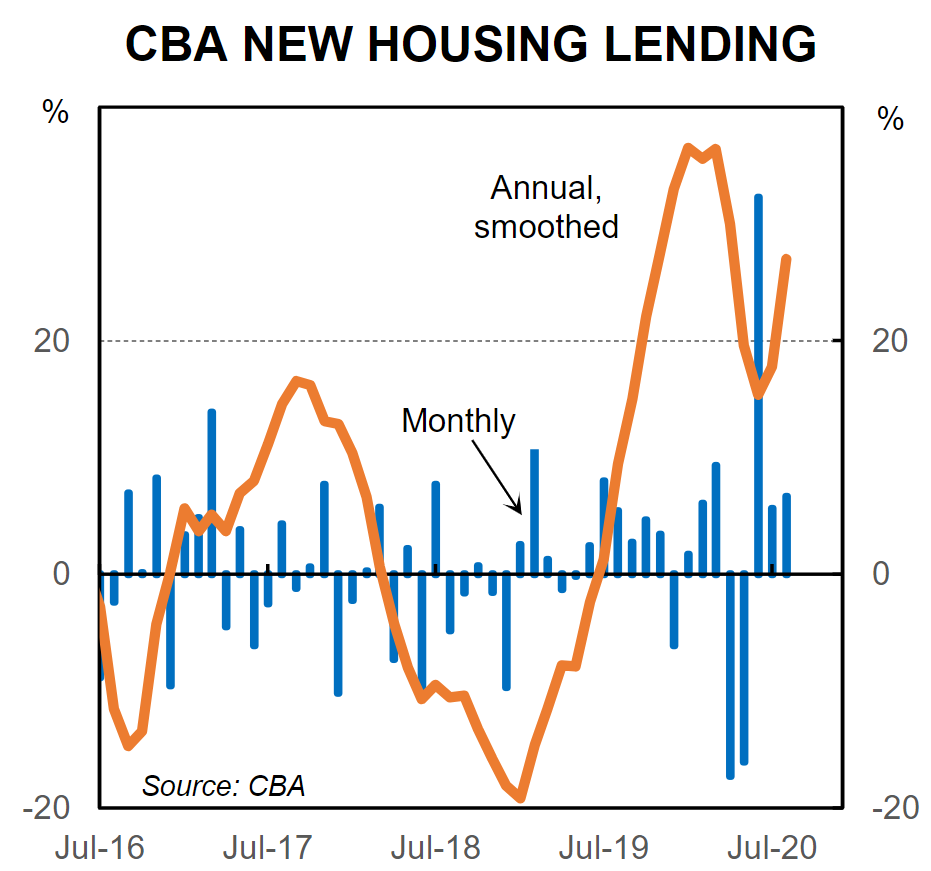

According to CBA’s internal data, Australian mortgage lending surged again in August:

New lending for housing rose again in August. A recovery in lending is one factor behind our view that dwelling prices will fall only modestly over the next 6months. And we expect dwelling prices to rise solidly in H2 21 (see here).

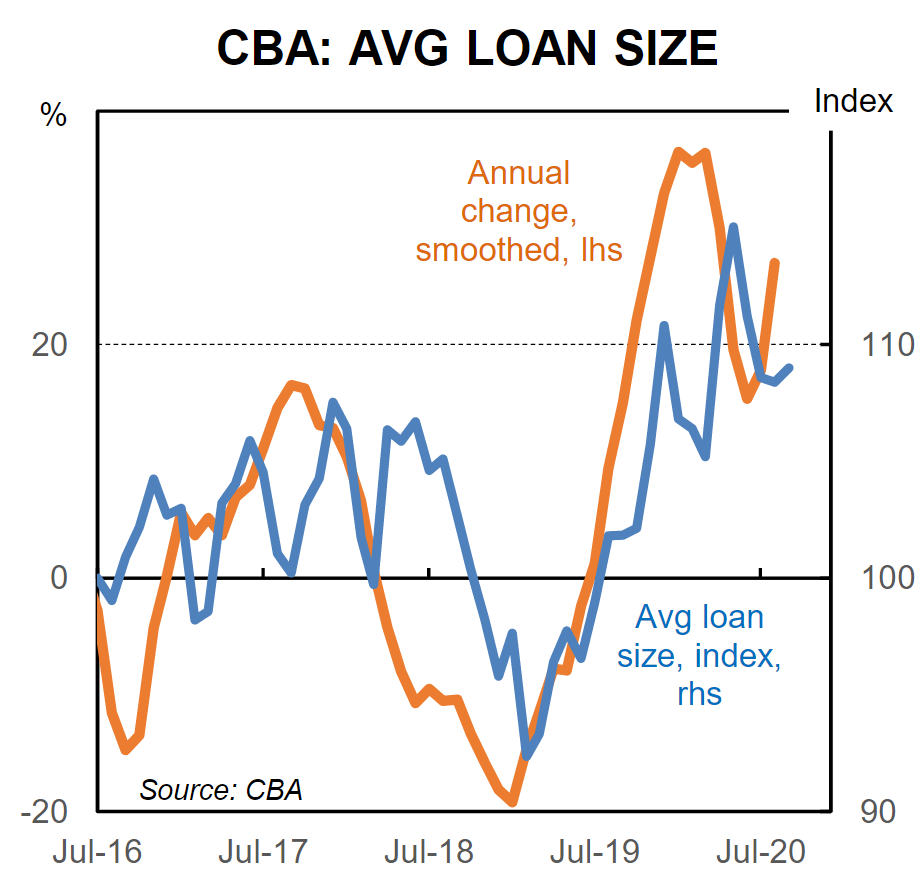

The average loan size was steady in August. The average loan size is higher than a year ago as lower mortgage rates mean that people are able to service a higher level of debt for a given level of income.

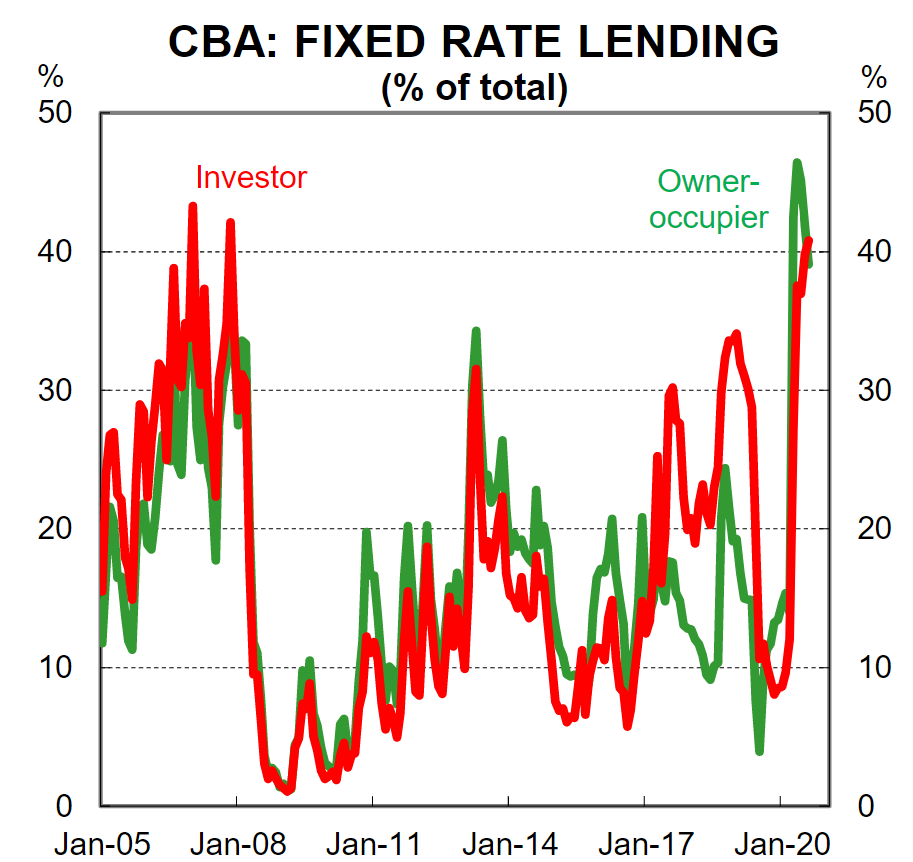

The share of fixed rate lending remained at a high level in August. The share of fixed rate lending has lifted for both owner-occupiers and investors. Fixed mortgage rates are generally lower than variable rates at present.

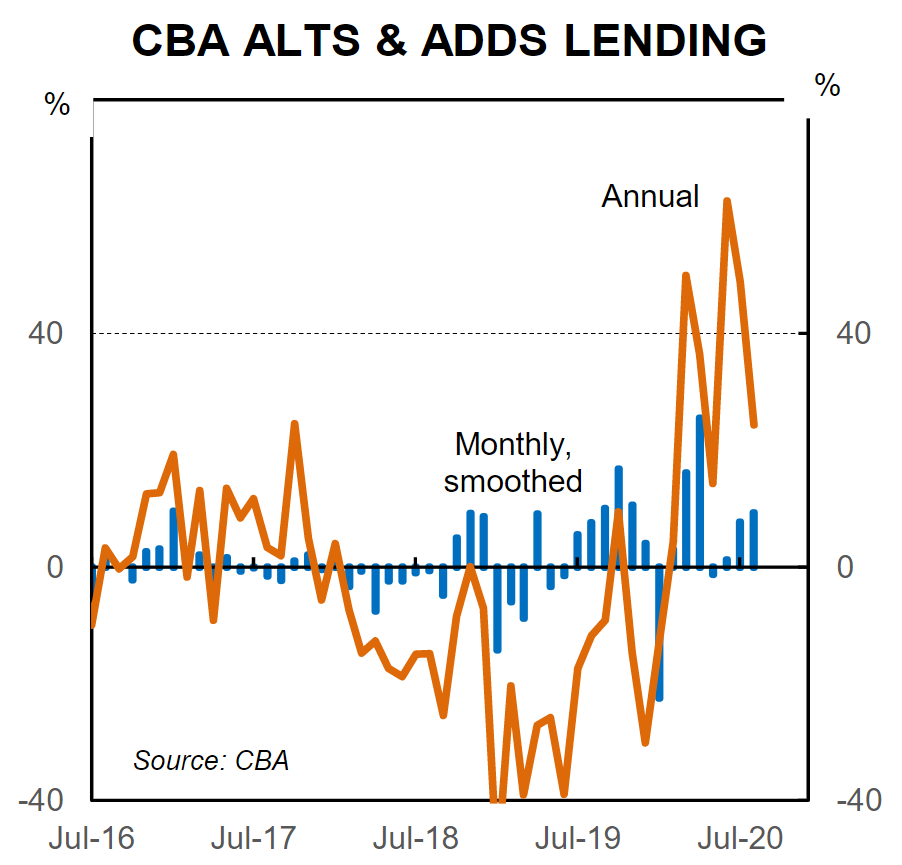

Lending for renovations is growing at a solid pace. Many people are undertaking home renovation work while spending more time at home. That said, stage 4 restrictions are currently limiting renovation activity in Melbourne.

It must be noted that CBA’s mortgage book is growing faster than the system, so there’s some market share impact at play. Nevertheless, the bounce recorded by CBA over previous months was reflected in the latest ABS mortgage data.

Thus, it could point to rebounding property demand.