CBA’s head of Australian economics has revised down its forecast for peak-to-trough property price falls and now believes that values will rebound strongly in 2021:

Key Points

The COVID-19 pandemic has had a negative impact on Australian residential property prices, but outcomes vary significantly by capital city.

We expect dwelling prices to continue to decline at a modest pace and to trough in Q1 21.

But we expect a solid recovery in prices from H2 21 as the borrowing cost once again becomes the dominant influence on prices.

We expect Melbourne property prices to significantly underperform against the national benchmark.

Overview

In April 2020 we published updated dwelling price forecasts to reflect the impact of theCOVID-19 pandemic on the Australian property market. Our central scenario was that dwelling prices nationally would fall by around 10% from their April peak. It is now September so we think that it’s an opportune time to revisit our forecasts in the context of how the housing market has performed over the past six months and how our views on the economic outlook have evolved.

In doing so, two things immediately stand out to us:

(i) the fall in dwelling prices to date has been a lot smaller than we anticipated; and

(ii)the variation between capital cities has been a lot larger than we expected.

For the record, we had always expected Melbourne and Sydney to underperform relative to the national average. The NSW and Victorian economies have more exposure to the most heavily impacted services sectors and less exposure to some of the more insulated sectors (i.e. mining and agriculture). In addition, the Sydney and Melbourne housing markets are more reliant on strong population growth via net overseas migration to underpin demand. But what we didn’t know of course was that COVID-19 would have a much bigger impact on the Melbourne economy relative to the other capital cities.

Parking the Melbourne issues to one side, what has genuinely surprised us is the resilience of house prices in some of the other capital cities considering the negative shock to labour markets around the country.

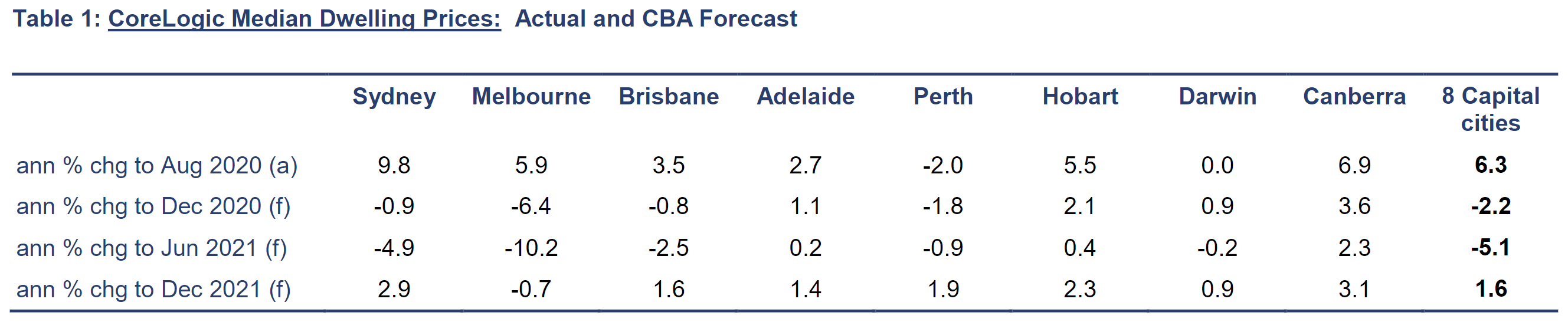

We continue to expect prices to ease. But we are now looking for a national peak to trough fall of 6% versus our previous call of 10%. We now expect that trough to arrive in Q1 2021 (versus end 2020 previously). And we expect a much larger disparity between outcomes by capital city than initially forecast. For example, we have forecast a fall in Melbourne property prices of 12% from April 20 to Q1 2021, whilst prices are expected to increase modestly in Hobart and the ACT over that period.

Our forecast profile for dwelling prices has been extended to end-2021. Our central scenario is that dwelling prices plateau in Q2 21 before rising over H2 21. Our forecast is for solid price growth in H2 21 as the economic recovery gains traction and incredibly low interest rates once again become the dominant influence on dwelling prices. This note outlines our views on dwelling prices, our underpinning assumptions and the risks to our forecasts.

Recent story

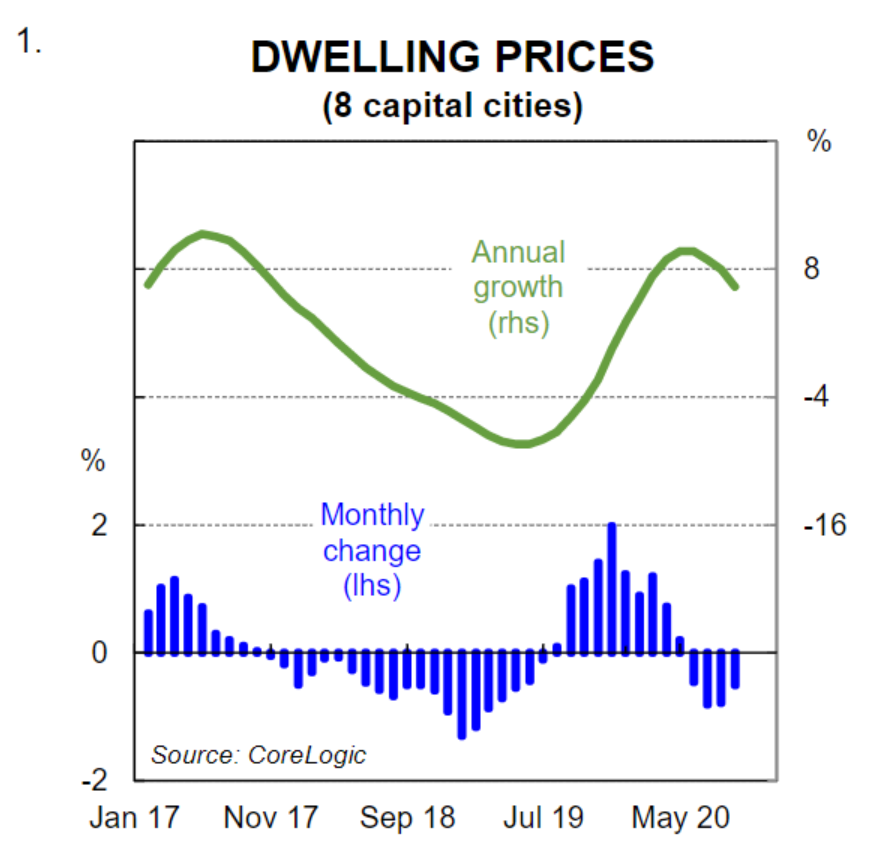

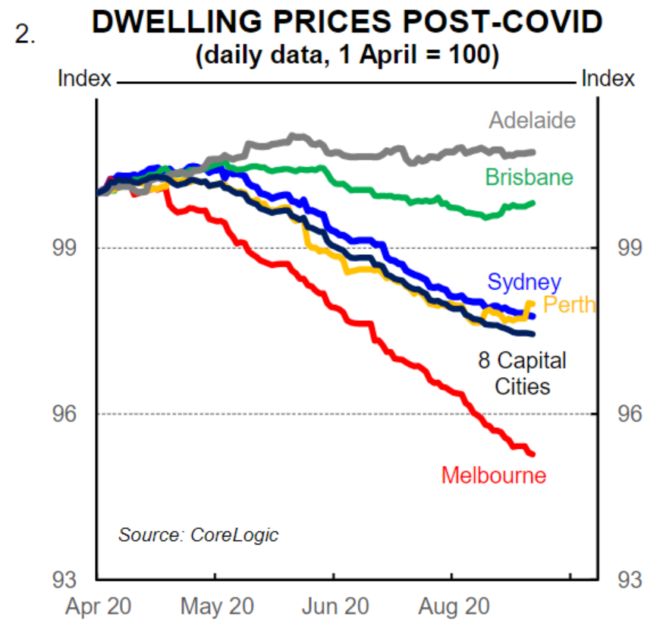

According to Corelogic, national dwelling prices peaked in April and have trended lower ever since (charts 1 & 2). Between April and August (latest available) price falls have been largest in Melbourne (-4.3%) and Sydney (-2.6%) – it’s worth remembering that price rises were strongest in Melbourne and Sydney in the year leading up to the pandemic so the negative wealth effect on consumption is negligible at this stage. Prices have also declined in Perth (-2.2%) since April, but they are little changed in Brisbane (-0.9%) and Darwin (-0.7%) and have risen in Adelaide (+0.3%), Hobart (+1.0%) and the ACT (+1.8%).

In the context of an extraordinary negative economic shock the fall in national dwelling prices is modest. And whilst momentum in the Melbourne market is clearly negative, it is not particularly soft in Sydney and is holding up elsewhere. The reason for Melbourne’s underperformance is obvious – the stage 3 and stage 4 lockdowns from July. It is clear that had Melbourne not gone back into lockdown price falls would be more modest.

National prices are likely to continue to slide in the near term, primarily because of the situation in Melbourne. Unemployment has not yet peaked in Victoria and rising unemployment is a clear headwind for property prices (note that it is the direction in unemployment that matters most for property prices as opposed to the level of unemployment). In addition the household perception of the national market is consistent with a further softening in prices and the demand impulse from net overseas migration is non-existent. This is more acutely felt in Melbourne and Sydney.

How much further will prices fall?

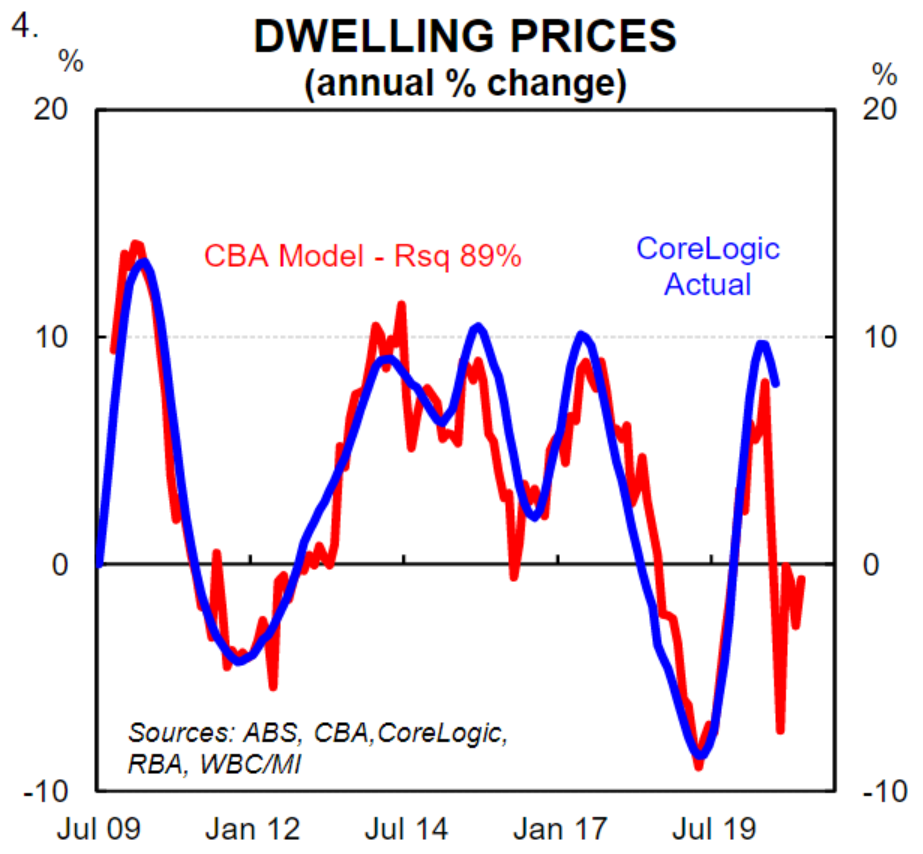

As a starting point we have input the latest leading indicators of the property market into our model. The CBA dwelling price model has a good track record in predicting national near term price movements (chart 4).

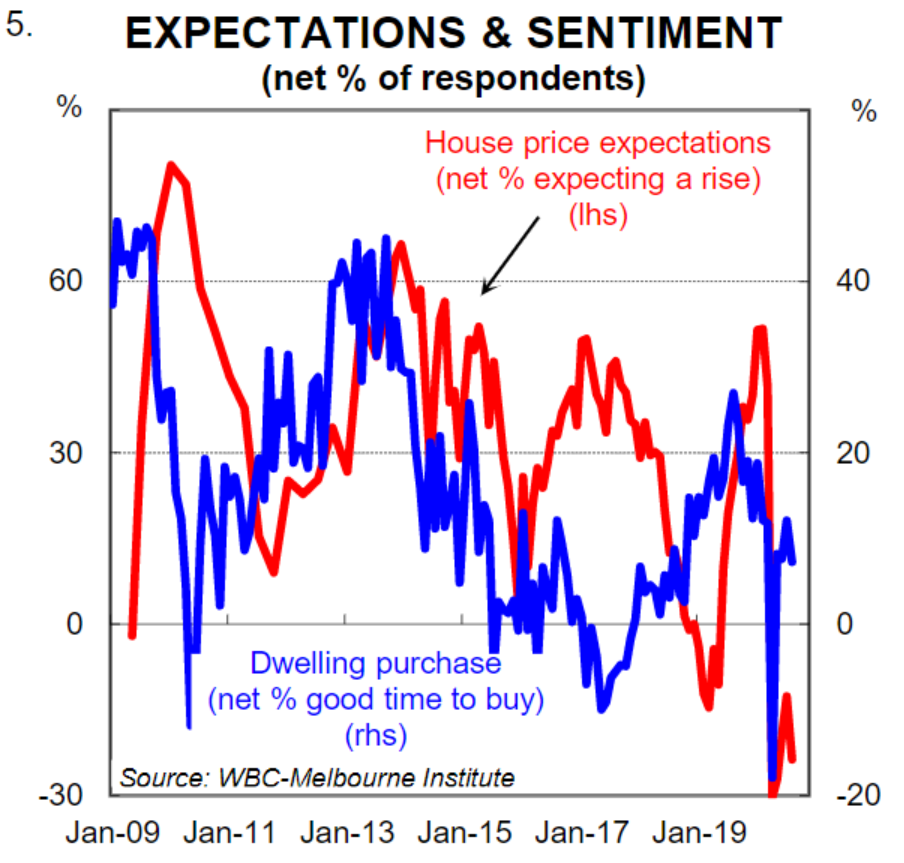

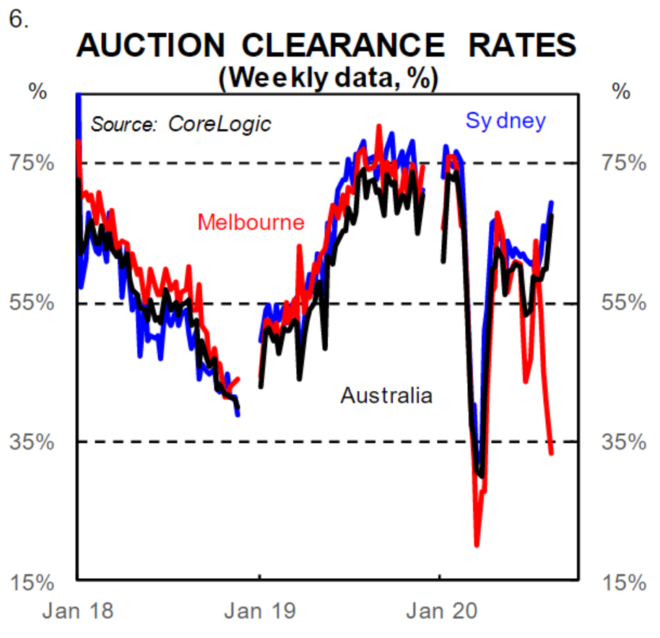

Our model puts the annual change in national dwelling prices as a function of the annual change in mortgage rates (1 year advanced), the annual change in the flow of credit (six months advanced), auction clearance rates (four months advanced) and the house price expectations index from the WBC/MI Consumer Sentiment survey (2 months advanced). The results are interesting because the inputs into the model are sending mixed signals.

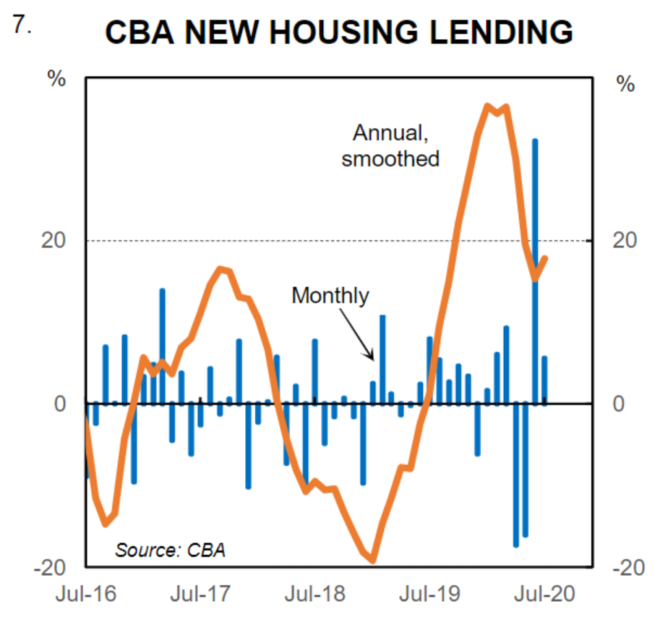

House price expectations remains in the doldrums, but the national auction clearance rate is holding at a decent level (charts 5 and 6). The disparity is unusual. And whilst new lending is lower than its pre-COVID level, it has picked up in recent months (chart 7).

Our top down modelling points to prices falling by a modest ~0.6% a month over the remainder of 2020. Our bottom up approach by capital city suggests a similar outcome. We therefore expect national dwelling prices to be down by -1.8%/yr at December 2020 (implying a ~5.0% fall in prices from April 2020). We have pencilled in a further small fall in Q1 20 which takes the total peak to trough fall to ~6%. From there our central scenario is for a stabilisation in prices before a solid recovery fromH2 21 (+3% over six months or an annualised pace of ~6%).

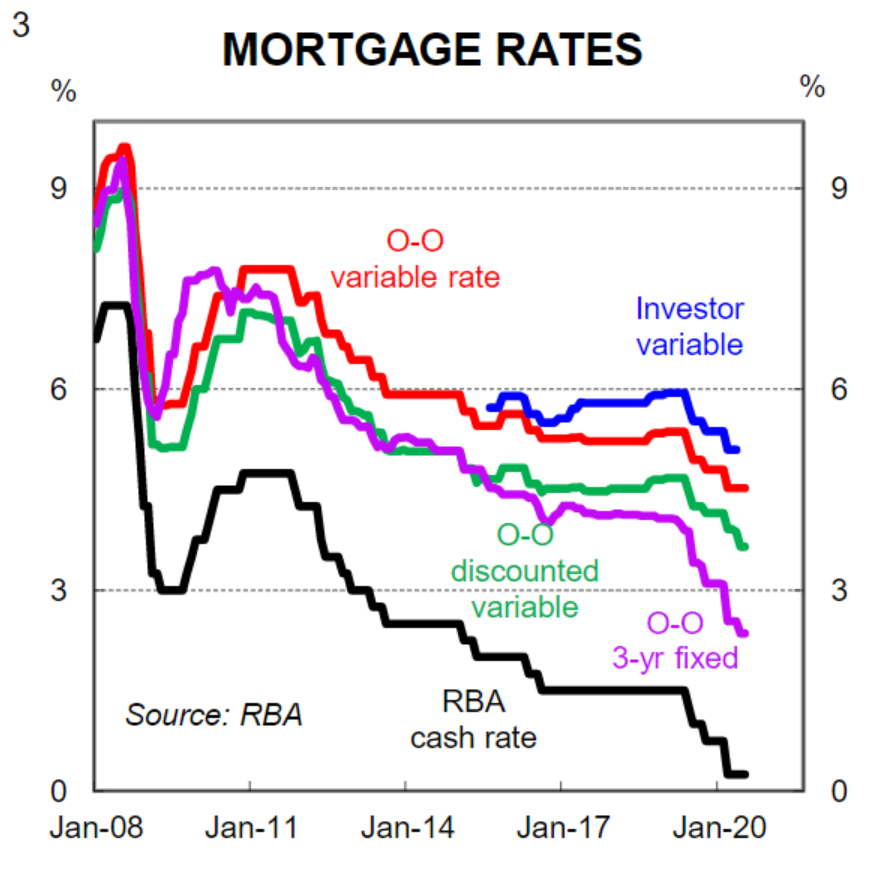

Why prices could bounce sharply in H2 21 The RBA cuts to the cash rate in 2019 and 2020 that took mortgage rates to record lows are the main reason why dwelling prices nationally have not fallen all that much considering the huge negative shock to the economy. As the economy recovers and the headwinds of rising unemployment and falling rents dissipate, we believe the borrowing cost will once again become the dominant driver of dwelling prices.

The RBA has tended to play down the influence of monetary policy decisions on dwelling prices. But we believe that changes in interest rates are the single most important driver of real property prices over the longer run.

The relationship between dwelling prices and monetary policy is quite straight forward: lower (higher) interest rates essentially means that for a given level of income a borrower can service a bigger (smaller) mortgage, all else equal. That means that lower (higher) interest rates put upward (downward) pressure on the demand for credit and therefore dwelling prices. We saw the profound impact that RBA rate cuts had on the property market as recently as last year. The housing market was reignited following three 25bp cuts to the cash rate in June, July and October2019and prices rose briskly until the pandemic arrived.

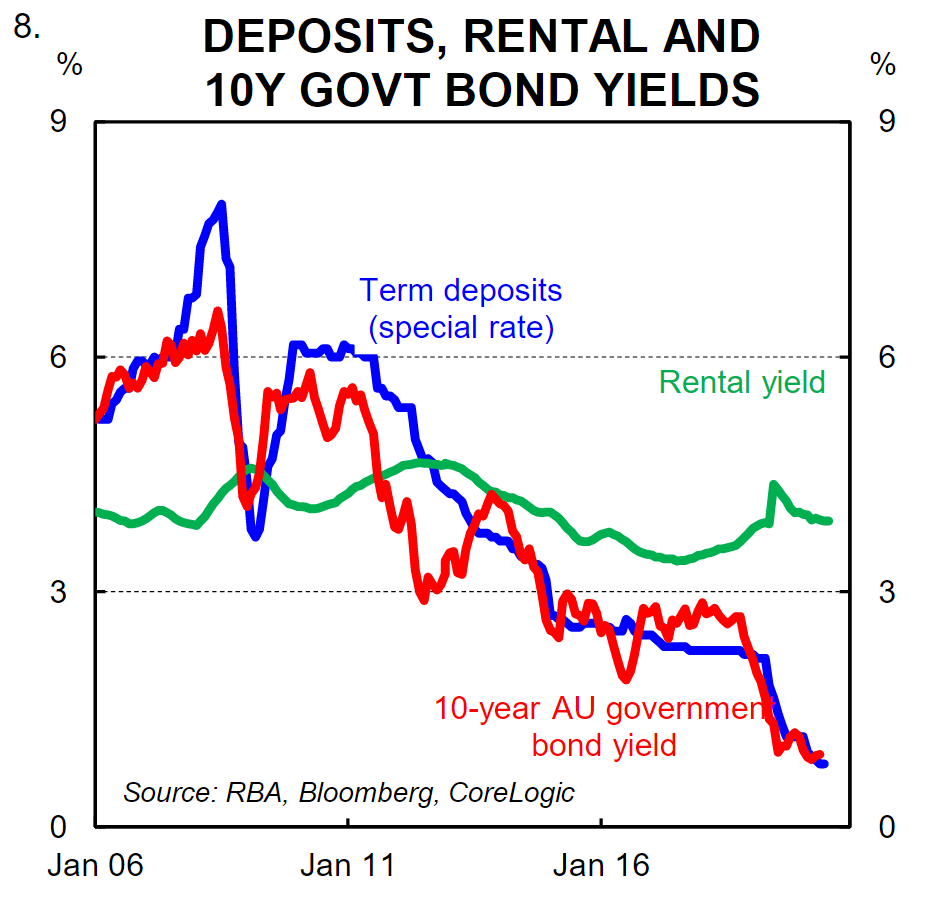

Importantly, lower interest rates don’t just have an impact on housing prices because households can borrow more for a given level of income. They also increase the attractiveness of property from an investment perspective because the yield on property is compared to the risk free rate (i.e. the term deposits rate for households–chart 8). It’s a similar story for equities, whereby lower interest rates push up equities prices, all else equal. Put another way, lower interest rates increase the demand for dwellings for both owner-occupiers and investors and they influence the price at which buyers and sellers will transact.

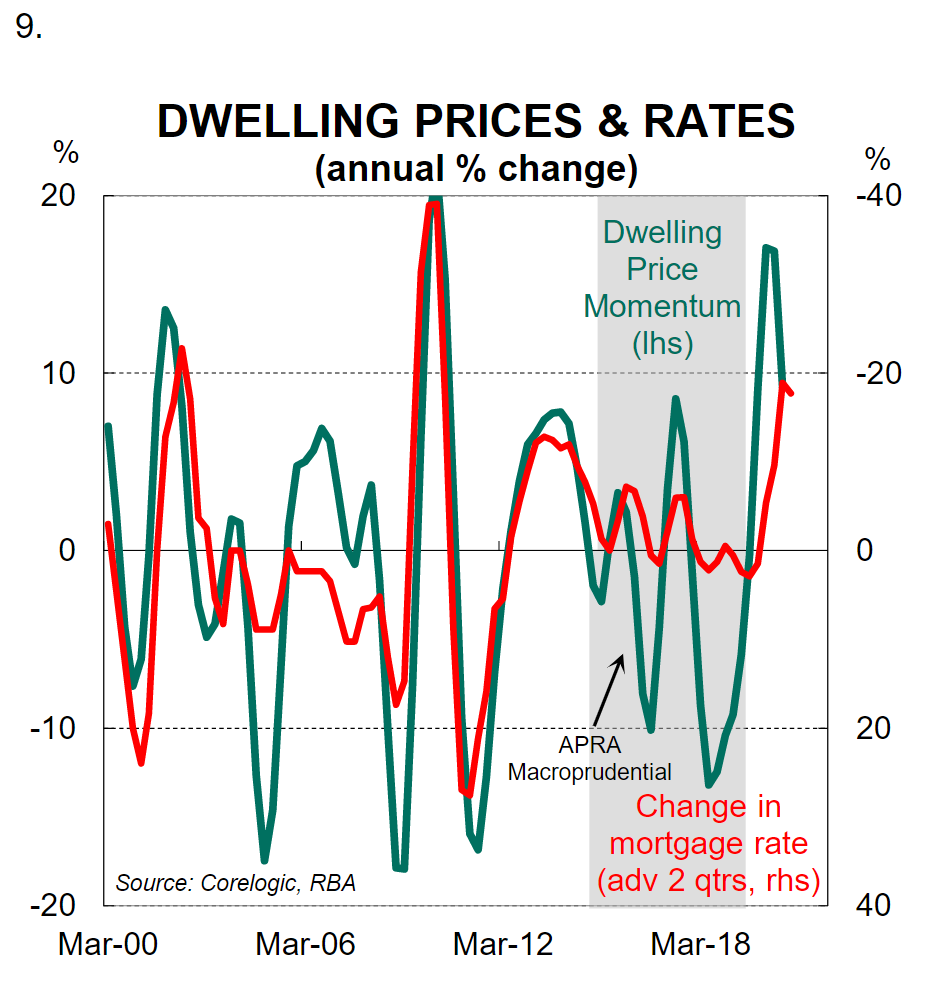

We have dived further into the relationship between interest rates and property priced and the evidence indicates that it is generally the percentage change in interest rates that has the greater impact on dwelling prices as opposed to the percentage point change in interest rates (chart 9). The distinction here is very important.

As interest rates approach the lower bound each percentage point shift lower in mortgage rates has an exponentially large impact on the interest cost of servicing debt because the percentage change in mortgage rates increases. In many ways that explains why property prices accelerated so quickly following the RBA’s rate cuts in 2019 –the percentage change in interest rates was large because mortgage rates were already very low.

Our message here is very simple –the cost of money impacts all asset markets including housing. The reason that asset prices, including dwelling prices, can seemingly decouple from the economy comes down to largely one thing –central bank policy and changes in the cost of money.

Risks

Back in April we wrote the following: “There are both downside and upside risks to our dwelling price forecasts. The risks both hinge on the length of the enforced shutdown and restrictions placed on economic activity. In a best case scenario government restrictions on economic activity could start to be lifted by the end of May. For that to occur, it would probably take several days of zero or very low community transmission of new COVID-19 cases. That is a possible scenario given the current trend in new COVID-19 cases. If that were to occur the plunge in economic activity that we expect would not be as large and the impact on the property market would not be as severe. Indeed the fall in property prices would be significantly smaller than our central scenario, particularly given the extraordinary low borrowing rates currently on offer.

There are scenarios, however, that are significantly worse than our central scenario. If restrictions are eased in Q3 20, as we expect, but a second round of COVID-19 new cases emerge then both the economy and housing market would be adversely impacted again. We would see restrictions return but the hit this time around on the economy and labour markets would be more significant and the damage would be longer lasting. Falls in dwelling prices far greater than our central scenario would be plausible. We believe that policymakers will be acutely aware of the risk of this scenario and as a result they will take a cautious approach to reopening the economy.”

As it turns out both risks essentially materialised. The best case scenario happened for all states other than Victoria where the downside scenario materialised.

Relative to our updated forecasts the risks are skewed to the downside. Any imposition of restrictions would likely see prices fall more than our central scenario which is based on no further lockdowns and a recovery in national economic activity from Q4 2020.

I am actually more bearish on the property market in early 2021. By then, most of the artificial economic supports are scheduled to unwind, including:

Emergency income support (JobKeeper and the JobSeeker supplement);

Mortgage repayment holidays;

Early superannuation release; and

Temporary rules preventing bankruptcies and insolvencies.

Advertisement

The expiry of these measures is likely to usher a significant number of forced sales, placing downward pressure on property prices.

The risks are obviously greatest for Australia’s army of negatively geared landlords caught between falling dwelling values and rents.

Whatever the case, 2021 will be an interesting year with any number of potential scenarios possible for both the economy and property market. It could go any number of ways and one cannot be too confident.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.