Industry Super Australia (ISA) were doing the rounds again yesterday, claiming the Morrison Government’s early release policy will add billions to the cost of the age pension over coming decades, thereby hammering future taxpayers:

“The community knows the government’s dealing with a crisis, but it doesn’t make sense to backflip on the promised super increase when you’ve just let people raid their savings,” ISA chief executive Bernie Dean said…

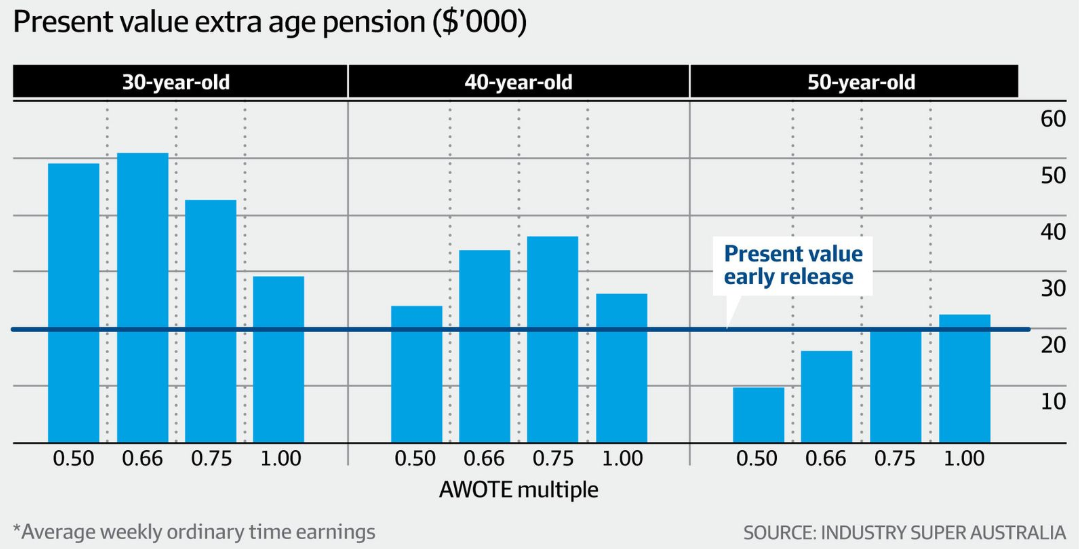

ISA said the scheme was a poor trade-off for individuals and taxpayers in the long run, with the long-term pension costs borne by taxpayers up to twice the present value of the amounts withdrawn.

It found a 30-year-old who withdraws $20,000 could be up to $70,000 worse off over their lifetime, while adding between $17,000 and $50,000 to the overall cost of the age pension. A 30-year-old couple could be up to $120,000 worse off, while adding between $60,000 and $100,000 to the age pension.

Sure, the withdrawal of $32 billion of superannuation savings will have an impact on future Aged Pension costs.

However, ISA has conveniently failed to acknowledge that if these funds were not withdrawn, the federal government would have been required to fill the demand hole by expanding government payments by a similar amount, which would have created an immediate budget cost.

Advertisement

Thus, the federal government has effectively traded off lower budget outlays today in exchange for higher budget outlays in the future. Why won’t ISA be upfront on the issue and admit that early superannuation release creates both benefits and costs for the federal budget?

Moreover, when will ISA acknowledge that superannuation concessions cost the federal budget more than they save in Aged Pension costs. This was made abundantly clear by the Henry Tax Review:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

Advertisement

The Grattan Institute has also comprehensively shown that over “both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments”:

Actuarial firm Rice Warner said that lifting compulsory super contributions to 12% would not have much impact on the age pension for many years, and would save the budget only about 0.1% in lower age pension spending in the second half of this century.

In contrast, extra super tax breaks from higher compulsory super would cost an average of 0.22% of GDP “through this century”…

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.