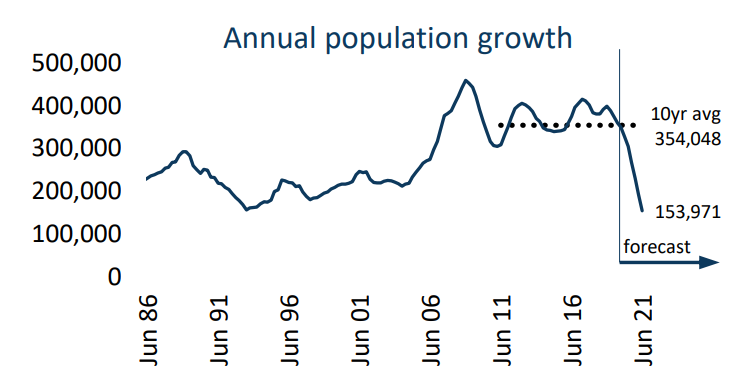

Recent forecasts from Treasury indicate annual population growth across Australia is set to slow from around 1.4% pre-COVID, to 0.6% through the 2020/21 financial year. In raw numbers, that implies Australia’s annual population growth will reduce from around 350,000 in 2019 to 154,000 over the year ending June 2021 – a reduction of 56% relative to 2019 levels.

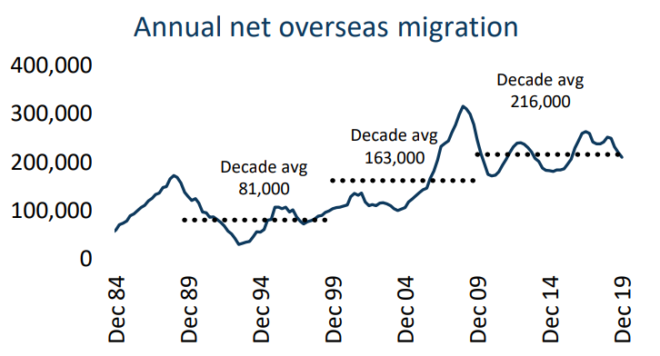

If the Treasury forecasts are right, this means the rate of population growth (a proxy for underlying housing demand) will be the lowest since 1917. Most of the forecast decline in population growth is due to stalled net overseas migration, which is expected to drop from around 232,000 net migrants in the 2018/19 financial year to just 31,000 in 2020/21. This will be disruptive to housing demand. However, the impact will not be evenly spread…

Previous research from the Australian Treasury showed approximately 85% of recent skilled migrants were renters and around 80% of those arriving on humanitarian grounds rented. The same research showed almost 90% of temporary skilled worker visa arrivals rented or lived in employer provided housing. Intuitively, the longer the migrant has lived in Australia, the more likely they will be seeking to purchase a home.

Considering the substantial skew towards temporary migrants within the NOM figures, as well as the assumption that most permanent migrants will initially rent rather than buy, the greatest impact from a sharp drop in migration rates is likely to be in weaker rental demand than demand for established home sales. This also implies a sharp drop in demand for new home construction targeted towards the rental market.

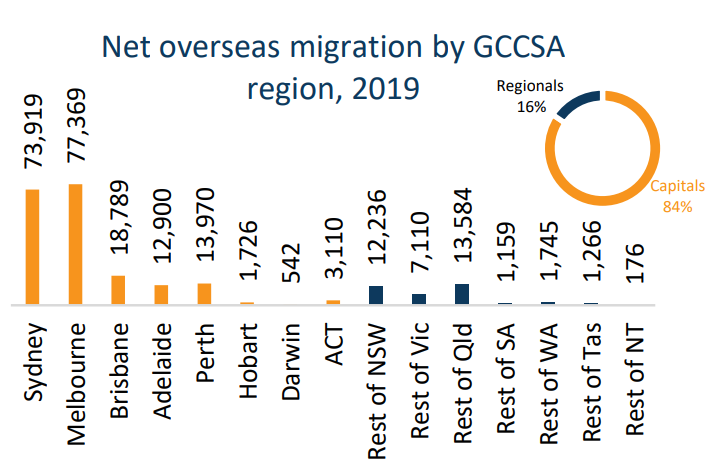

Geographically, stalled NOM will impact on Melbourne and Sydney the most. Last year 84% of all overseas migration flowed into the capital cities. Three quarters of those capital city migrants arrived in Sydney and Melbourne. Within the cities, the largest number of overseas migrants are generally centered around the CBD, and precincts close to the CBD, where high density housing options are common, and to a lesser extent, middle ring suburbs close to educational precincts or transport hubs such as Parramatta in Sydney or Clayton in Melbourne.

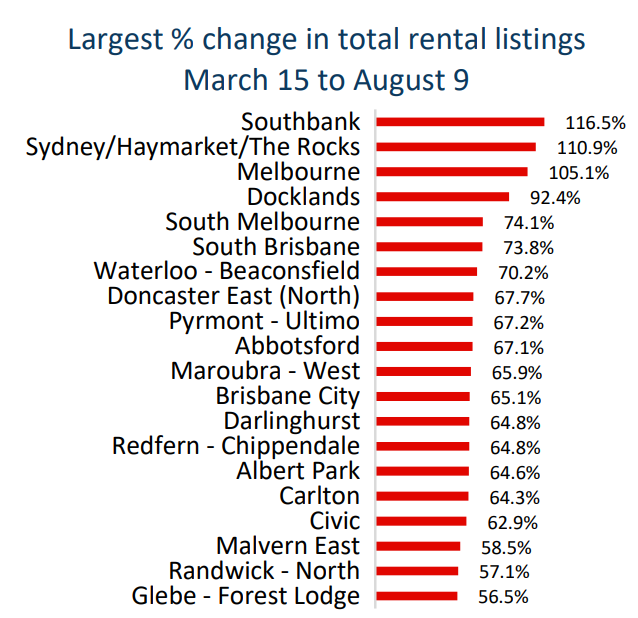

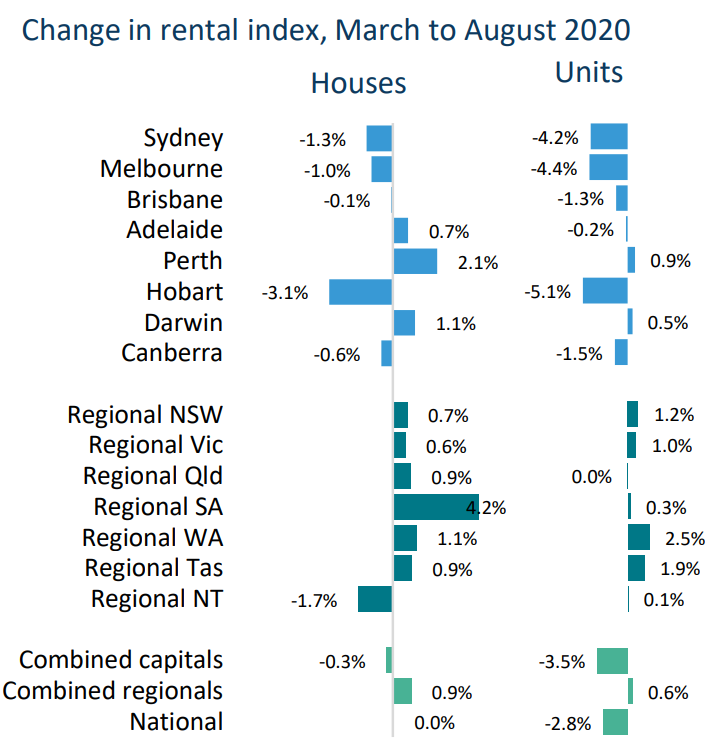

The impact of the sharp fall in overseas arrivals can already be seen in surging inner city rental advertisements, with rental listings more than doubling across some key inner city unit precincts. Between mid-March and early-August, the number of homes available for rent in Melbourne’s Southbank rose by 117% to reach 1,230 advertised rental listings. Rental ads were up 111% across the Sydney CBD/Haymarket/The Rocks region to reach 776 and Melbourne’s CBD saw a 105% lift in advertised rentals taking the total number of homes available to rent to 2,184.

High density, multi-unit dwellings in these precincts are popular with investors due to what has historically been strong rental demand. This historically strong rental demand was underpinned by overseas student numbers, but also domestic students, visitors and workers requiring accommodation close to the CBD.

The demand shock in these areas has been broader than the impact of stalled NOM. Rental demand is also impacted by weaker labour market conditions amongst highly casualised industry sectors such as food, accommodation, arts and recreation workers. Workers in these segments are more likely to be renters than home owners relative to other industries of employment. Additionally, fewer workers may be demanding rentals in the CBD’s due to remote working arrangements.

The rise in available rental stock in these precincts is already weighing on rental income. Every capital city is showing a larger fall in unit rents relative to house rents through the COVID period to-date, with a more significant difference in Melbourne and Sydney where unit rents are down more than 4% since March.

The flipside is that outside of Melbourne and Sydney, housing demand derived from NOM is less significant…

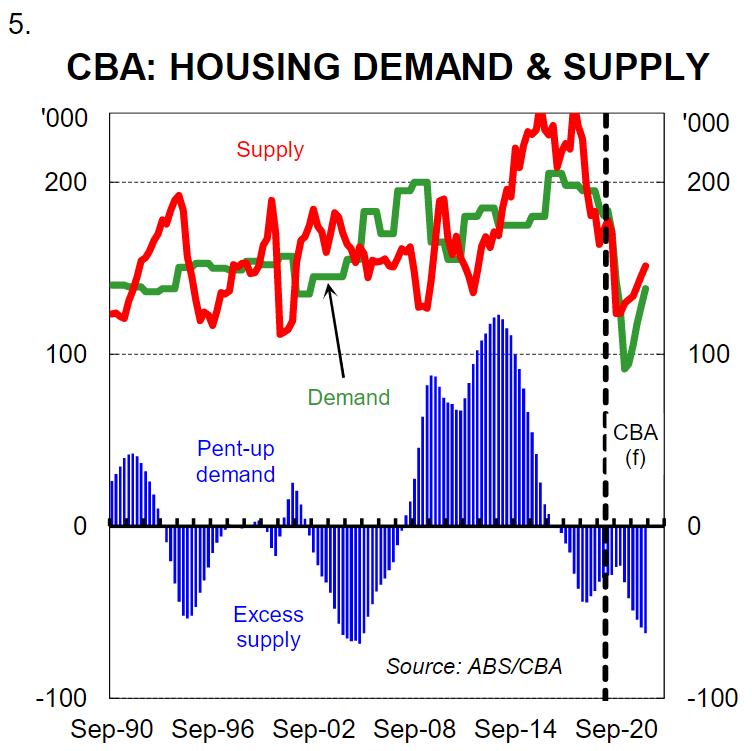

This follows analysis from CBA last week, which forecast that population growth would drop to ~180k in 2020/21, reducing the underlying demand for new housing from ~185k dwellings per year (i.e. based on the assumption of 2.1 persons per dwelling and the demolition rate) to 95k. This, in turn, will drive a significant oversupply of housing:

No wonder the property lobby are squealing like stuck pigs and seeking to reboot mass immigration ASAP.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.