CBA’s head of Australian economics, Gareth Aird, has released research showing that underlying demand for new housing has cratered due to a significant decline in immigration:

Key Points

A significant decline in the rate of population growth due to the drop in net overseas migration has reduced underlying demand for new housing.

Falling dwelling prices and heightened uncertainty around the economic outlook will also weigh on new residential construction.

But alterations and additions look set to increase due to record low interest rates and government support.

Overview

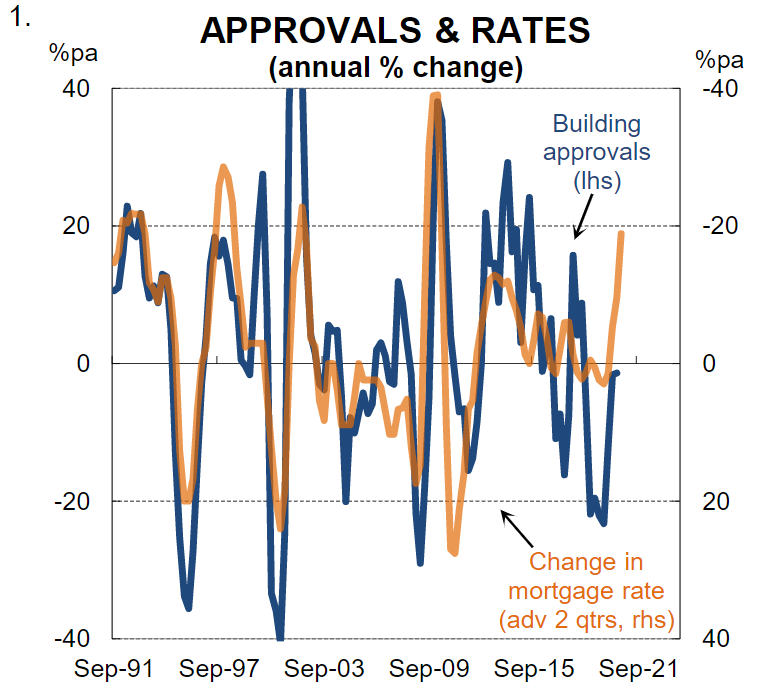

Historically changes in mortgage interest rates have been the primary driver of the residential construction cycle (chart 1). It is generally well understood that dwelling construction is one of the most interest rate sensitive parts of the economy. As such, when the Reserve Bank of Australia (RBA) resumed cutting the cash rate in June 2019, having left monetary policy on hold for almost three years, a lift in dwelling investment was expected. Indeed in the RBA’s February 2020 Statement on Monetary Policy (SMP) it was noted that, “the trough in dwelling investment is expected to occur in the second half of 2020, before a recovery in residential construction gets underway through 2021”. At the time we agreed.

But there are other dynamics now in play due to the COVID-19 pandemic that will shape outcomes from here. More specifically, the shock to population growth due to the plunge in net overseas migration is unprecedented and will dramatically reduce underlying demand for new housing. The upshot is that we believe we will see an unusual disparity open up between new residential construction and renovation activity over H2 20 and 2021.

New residential construction will be heavily negatively impacted by the sharp drop in population growth. Falling dwelling prices, heightened uncertainty around the economic outlook and rising vacancy rates will also weigh on new building at the margin. But the outlook for alternations and additions looks a lot brighter. Record low interest rates due to RBA rate cuts as well as government support is expected to result in an increase in the volume of renovation work done.

In this note we discuss the outlook for residential construction both from an output and employment perspective. We table our updated forecasts for new dwelling commencements and dwelling investment (both new construction and alternations and additions). A state breakdown is also provided for commencements.

Lower population growth means less new housing construction

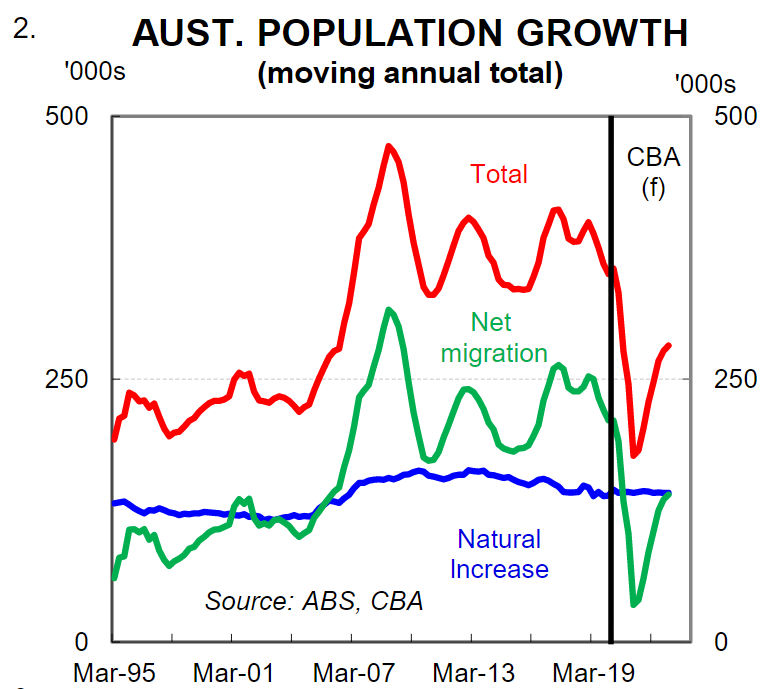

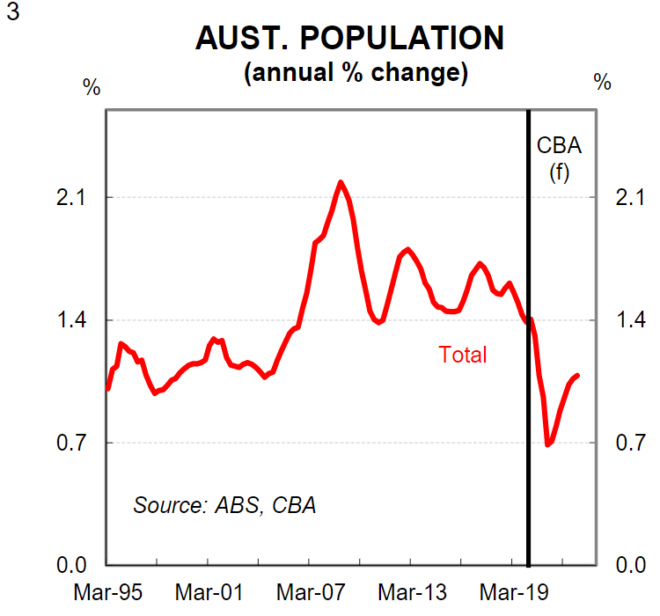

The dynamics around population growth are very important for new housing construction. Net overseas migration (NOM) and in turn population growth will decline significantly over the short run due to the COVID-19 pandemic. The Australian Government expects NOM to have fallen by ~30% in 2019/20 and to fall by ~85% in 2021/22. This means that there is an expected shortfall of around ~310k in NOM over the next 18 months compared to original estimates (chart 2). Population growth will slow sharply from 1.5% to 0.7%/yr over that period (chart 3).

Clearly nobody at this stage knows when the international borders will be reopened and when NOM will start back up. But we don’t think it’s simply a matter of turning the tap back on to the pre-COVID level of NOM. The Australian labour market will have an elevated level of slack for many years. That means that there will a lot of Australian residents who are either unemployed or underemployed. Both politically and economically boosting labour market supply when the supply of labour already exceeds the demand for labour makes little sense. Therefore we think that it is more likely than not that when the borders reopen NOM will be materially lower for several years than it was before the pandemic. There are clear implications for new housing construction.

Lower growth in the population means less demand for new housing and less residential construction than would otherwise be the case. For Australia the impact of lower NOM on new dwelling construction will be very significant. Australia’s population grew by ~380k per annum over the two years prior to the pandemic. That meant underlying demand for new housing had been running at ~185k dwellings per year (i.e. based on the assumption of 2.1 persons per dwelling and the demolition rate). But with population growth set to drop to ~180k in 2020/21 the underlying demand for new housing plummets to 95k.

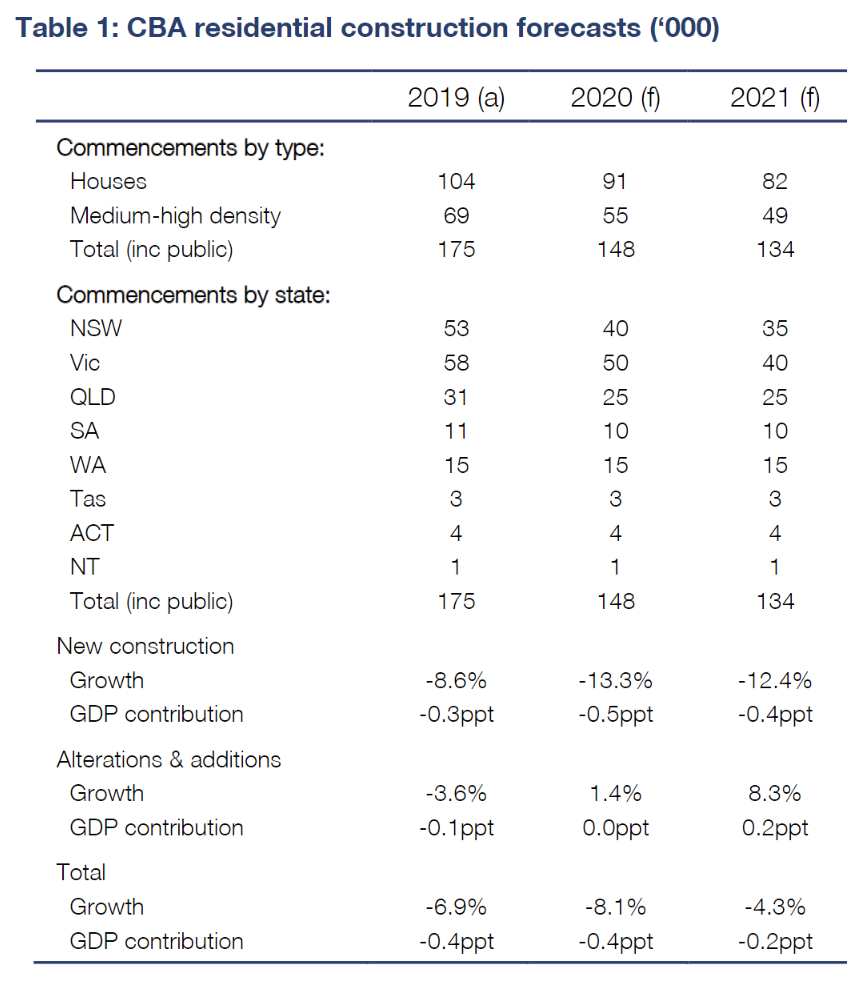

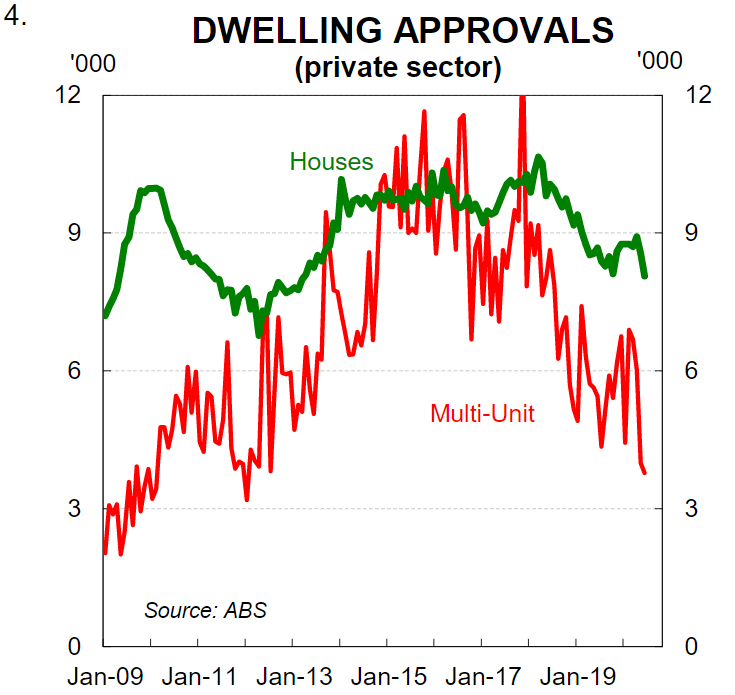

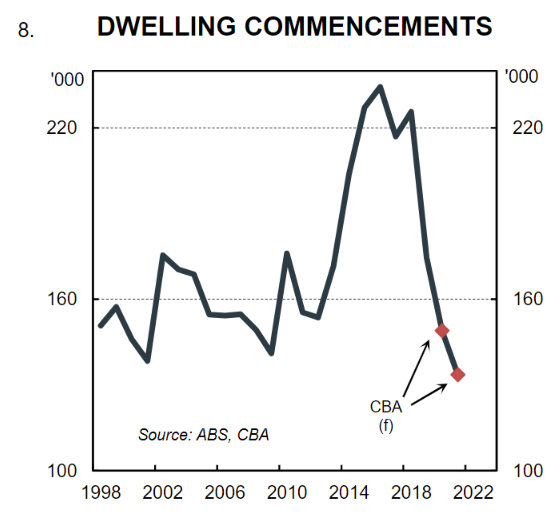

Building approvals, which are the best near term forward looking indicator of residential construction, have fallen since the pandemic arrived in Australia (chart 4). But they have not dropped as quickly as the expected decline in NOM would imply. Further falls in approvals are anticipated, but on our estimates dwelling commencements will likely exceed underlying demand for housing over the next year. That means some excess supply in the short term. Our forecast is for dwelling commencements of 148k in 2020 and 134k in 2021 (commencements were 175k in 2019).

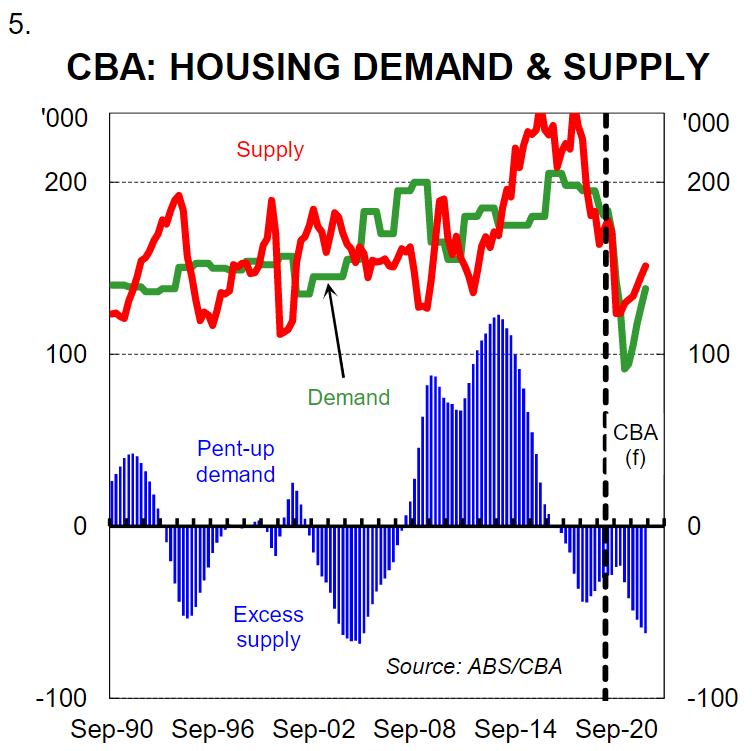

We should point out here that there are often mismatches over the short run between housing supply and demand (chart 5). Historically such mismatches have had a greater impact on rents than dwelling prices. Indeed a look at previous cycles indicates that over the short run both new residential construction and dwelling prices can decouple from underlying demand. But ultimately an equilibrium is reached over the medium to longer run as new dwelling construction either accelerates or declines to match underlying demand. Our expectation is that the excess supply in 2020 relative to underlying demand will result in a further fall in commencements in 2021 even if population growth starts to lift. These falls are anticipated to be concentrated in NSW and Victoria. Overall we expect a prolonged period of falling new dwelling investment(-13¼% in 2020 and -12½% in 2021).

Renovations

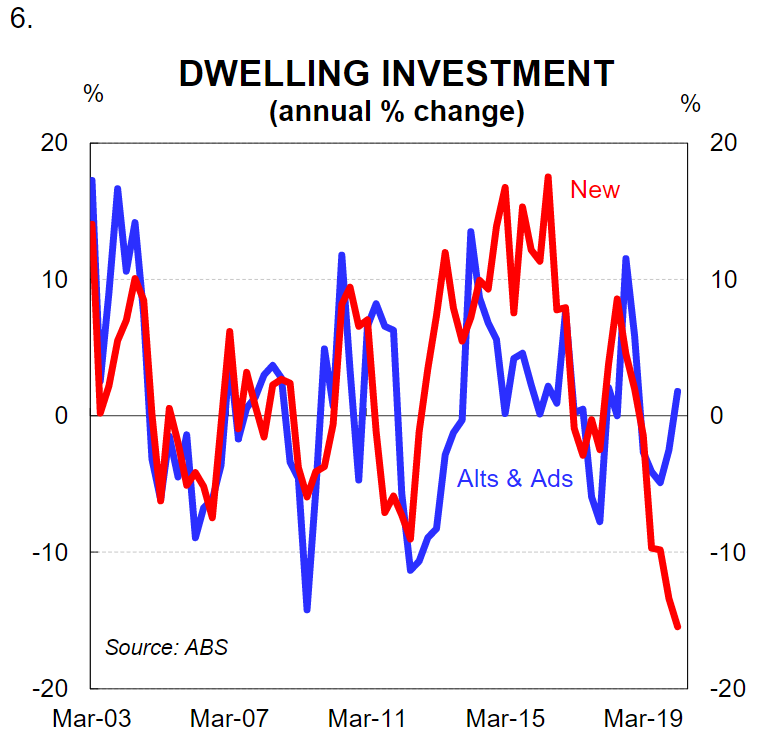

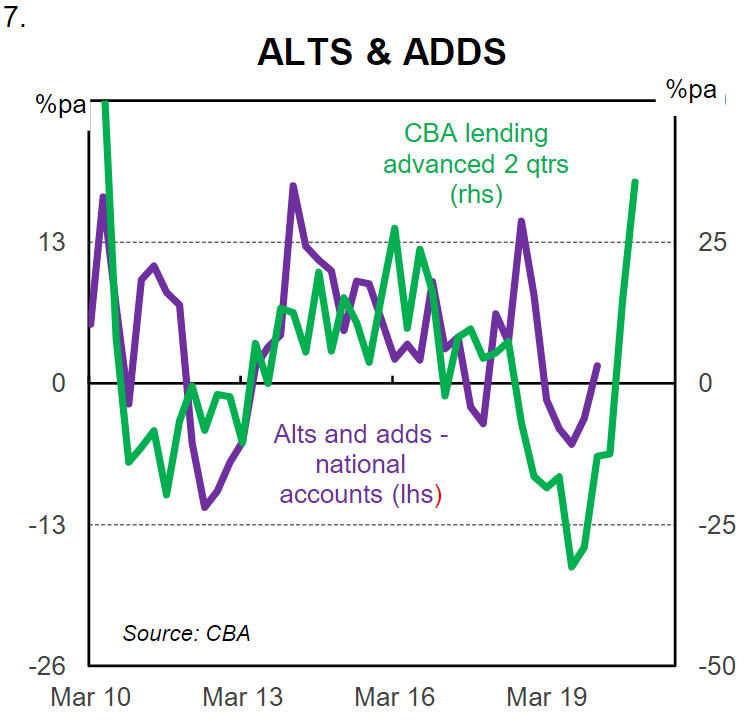

We believe that the outlook for alteration & additions (i.e. renovations) is very different to the outlook for new construction. In the past alterations & additions and new construction have generally moved up and down together (chart 6). Changes in interest rates have been the dominant driver of both. But this time will be different because of the big shock to underlying demand from the drop in NOM.

Our expectation is that the decline in interest rates will still support alterations & additions as has historically been the case. Falling population growth in and of itself does not mean renovation spend should be impacted. Indeed our internal lending data on alterations & additions, which has historically been a good leading indicator of renovation spend, supports this view. We have seen a material increase in lending for alterations & additions over the past few months (chart 7). Borrowing rates have come down considerably since June 2019 and this is having a lagged positive impact on new lending–activity will follow. Government support is also helping through the HomeBuilder program.

Table 1 contains our forecast for new commencements, new dwelling investment and alterations and additions in 2020 and 2021.

Impact on employment

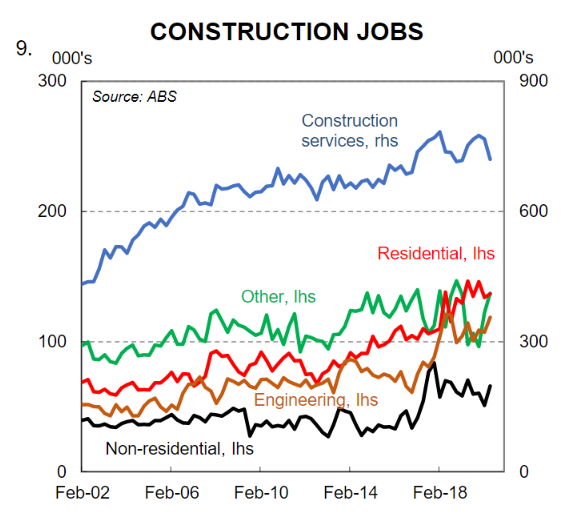

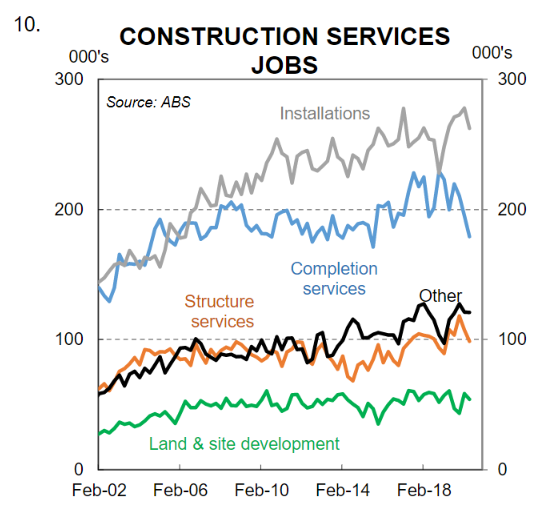

Residential construction is labour intensive and so our forecast for a contraction in dwelling investment of 8.1% in 2020 and 4.3% in 2021 has implications for the labour market. The ABS estimates that 1.18 million people are employed in the construction space split between residential construction, engineering construction, non-residential construction and constructions services (by far the largest component –see charts 9 and 10).

Taking a GDP weighted measure of construction services and adding the direct ABS residential construction jobs estimate leads us to conclude that around ~510k jobs are directly linked to residential construction. We therefore think that direct job losses as a result of the contraction in residential construction are likely to be ~50k-55k spread over an eighteen month period.

I believe total construction jobs could be far higher than 50,000 to 55,000 given business investment is also likely to tumble.

Regardless, the states and federal government better get cracking on infrastructure investment to soften the blow.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.