According to Richard Gluyas at The Australian, Australia’s major banks have deployed more staff to their financial hardship units as loan deferral periods for mortgage and small business customers begin to wind down. The banks are also anticipating a sharp rise in loan defaults as government stimulus measures begin to be scaled back.

National Australia Bank has begun contacting customers who had deferred their loan repayments, but CEO Ross McEwan recently told a parliamentary committee that 20% of these customers have failed to respond to its calls, emails and text messages:

“The thing that distresses me right now is, when we’re making calls to customers to check in, 20 per cent won’t pick the phone up or call back, even if we text, email and phone,” Mr McEwan told the committee…

The revelation prompted a special plea to bank customers from AFCA chief executive David Locke… “If you received a deferral on loan repayments from your bank earlier this year and continue to experience financial hardship as a result of COVID-19, it is extremely important that you contact your bank as soon as possible to talk about the options available to you”…

The concern among the banks is the extent to which $240bn in deferred loans — including $167bn in housing credit (9 per cent of total accounts) and $55bn in SME loans (17 per cent of total accounts) — turn sour after deferrals expire at the end of March next year…

“It’s not so much the calm before the storm; it’s more like the nirvana before the storm,” Jefferies’ veteran bank analyst Brian Johnson said.

“No one really knows what’s going to happen when the support is withdrawn, but it’s hard to conclude that things are not going to get a lot tougher.”

Mr Johnson said it was “alarming” that 20 per cent of NAB’s customers on repayment holidays had failed to respond to the bank’s calls.

The amount of economic support scheduled to be withdrawn over the next month is going to be massive.

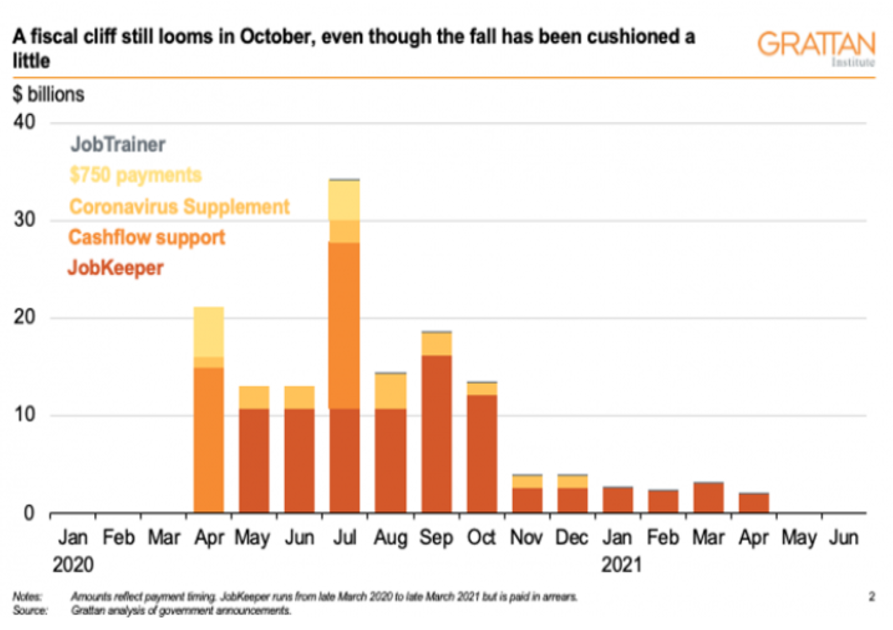

The Grattan Institute estimates that emergency income support will be reduced from $18 billion a month (10.7% of monthly GDP) to $3 billion a month (1.9% of GDP) for the six months beyond:

The deadline for withdrawing superannuation is also set for 31 December. Early superannuation release has also provided $33 billion of additional disposable income to households. Thus, its removal will drain household disposable incomes further.

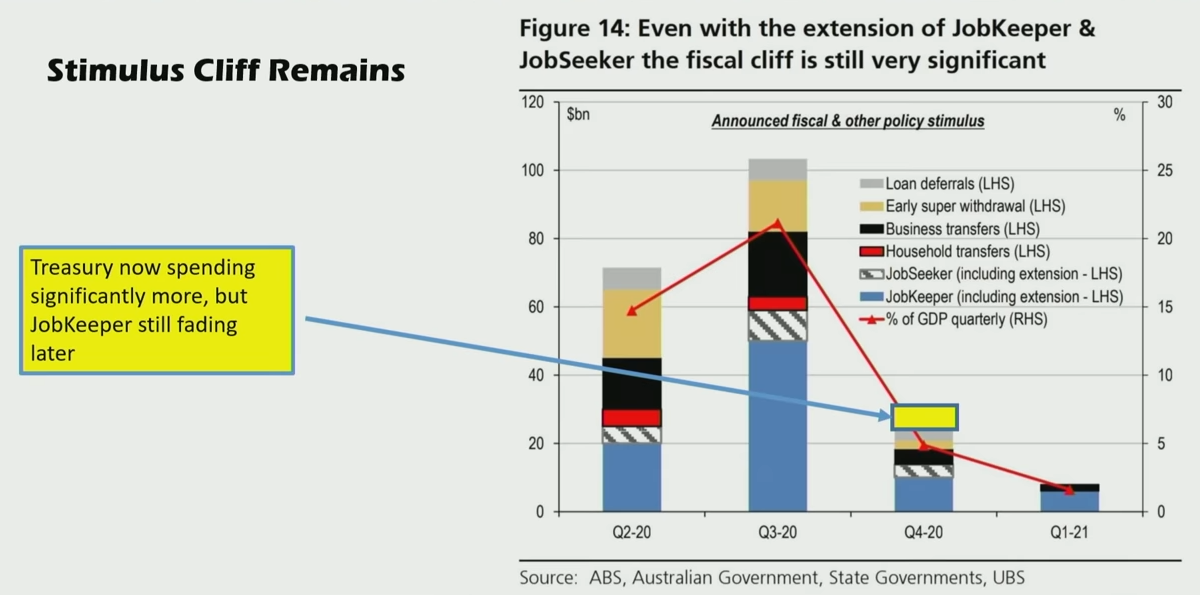

UBS has estimated a similar collapse in emergency support:

As you can see, emergency support is scheduled to fall from more than $100 billion in Q3 to around $30 billion in Q4 and then less than $5 billion in Q1 2021.

When viewed in this light, there is a good chance that many thousands of Aussie households will be unable to meet their mortgage repayments and will be forced to sell. If this happens, it will obviously place significant downward pressure on property prices.