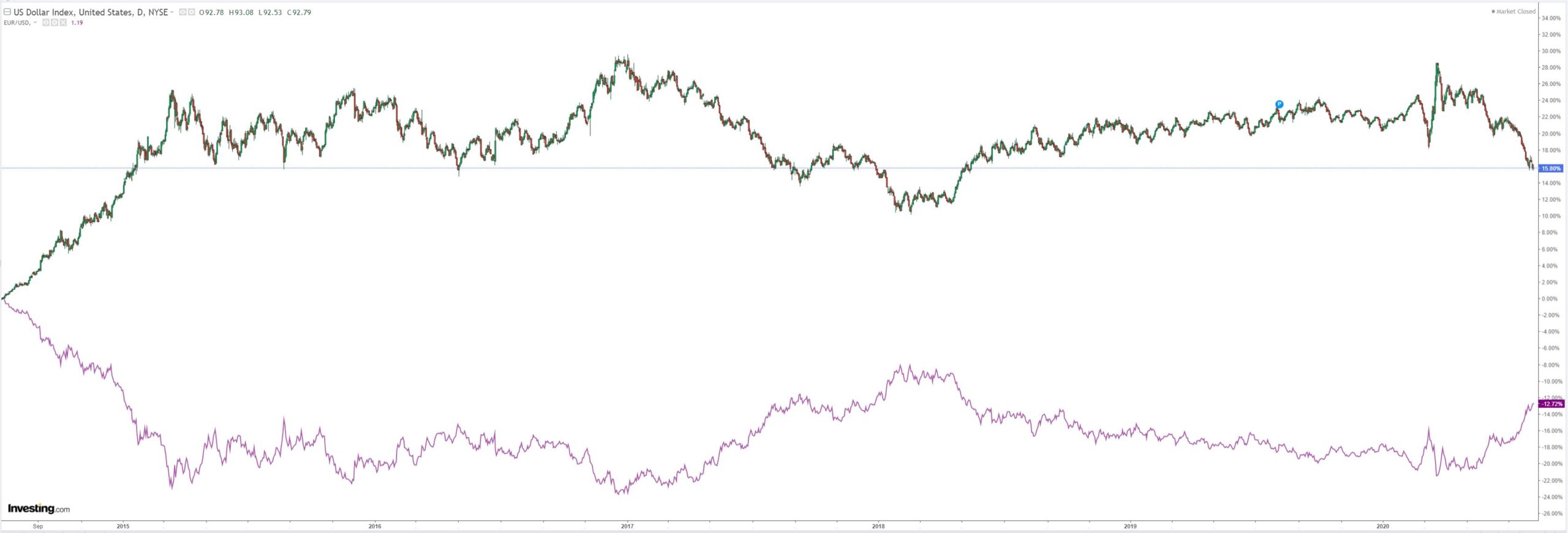

DXY is struggling to hold support:

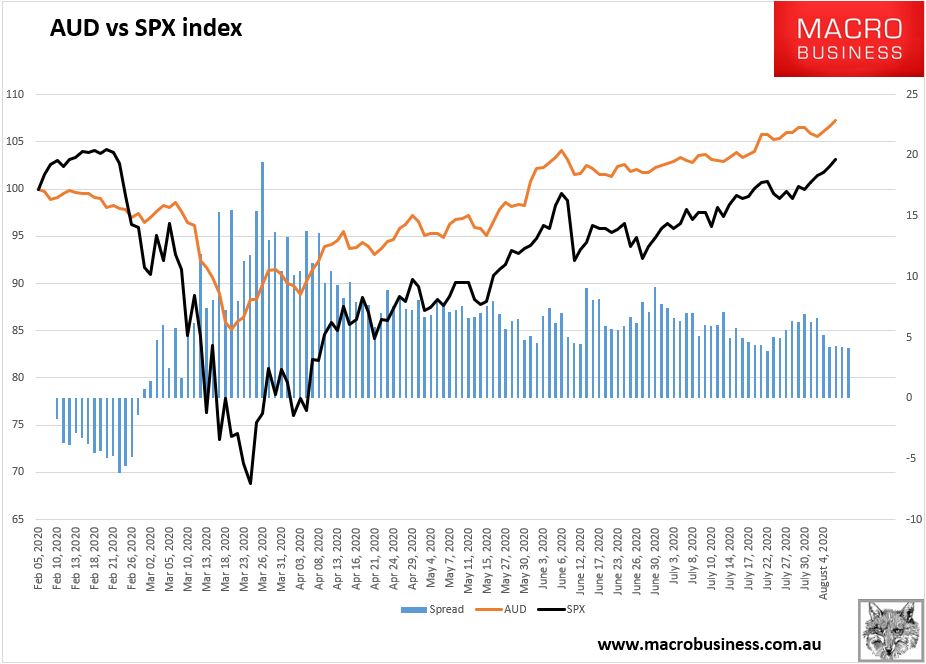

The Australian dollar scorched everything in sight:

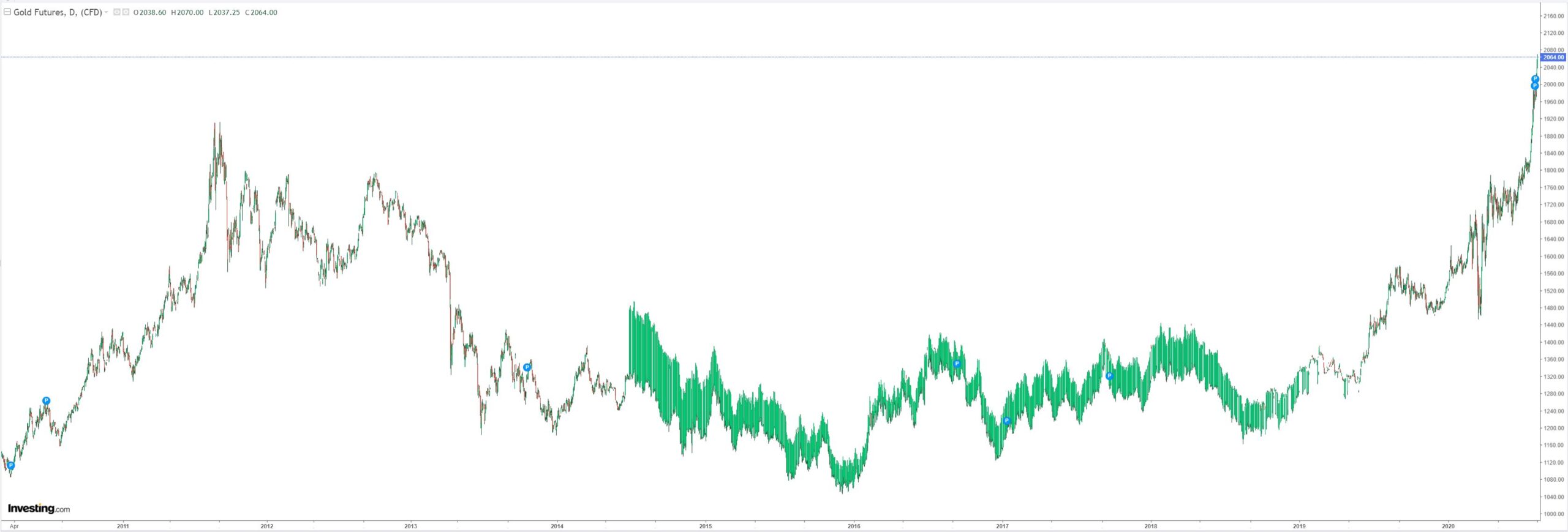

Gold mania:

Oil flamed out:

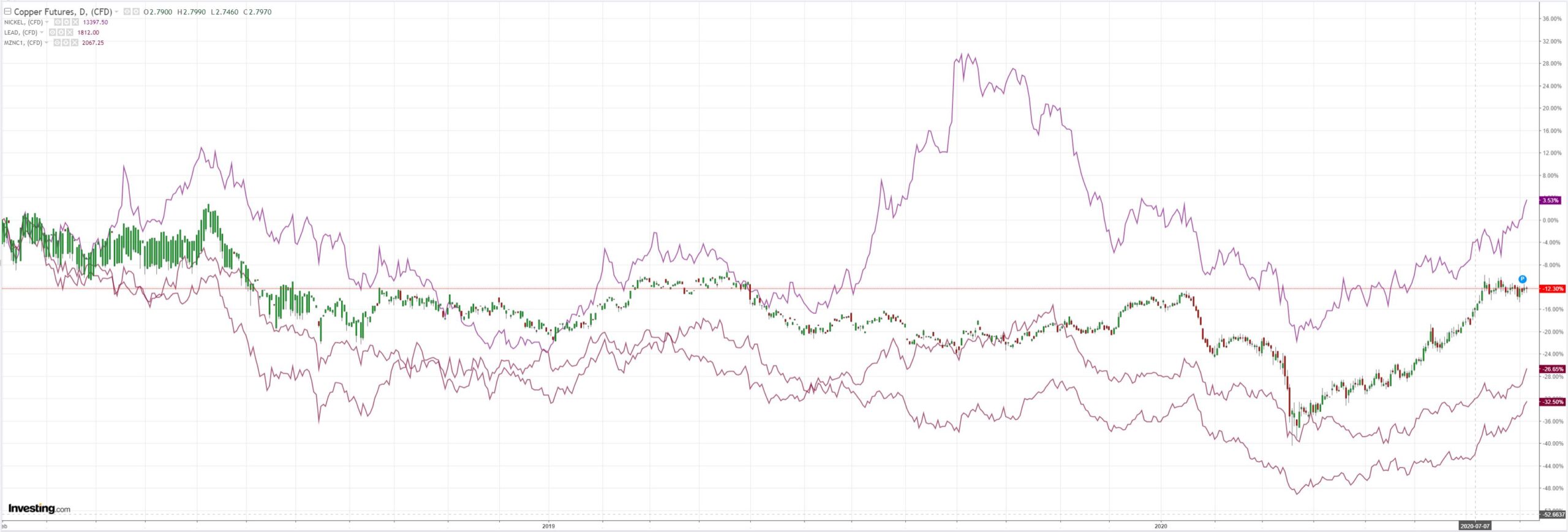

Metals mania:

But a GLEN shocker landed on miners:

EM stock breakout:

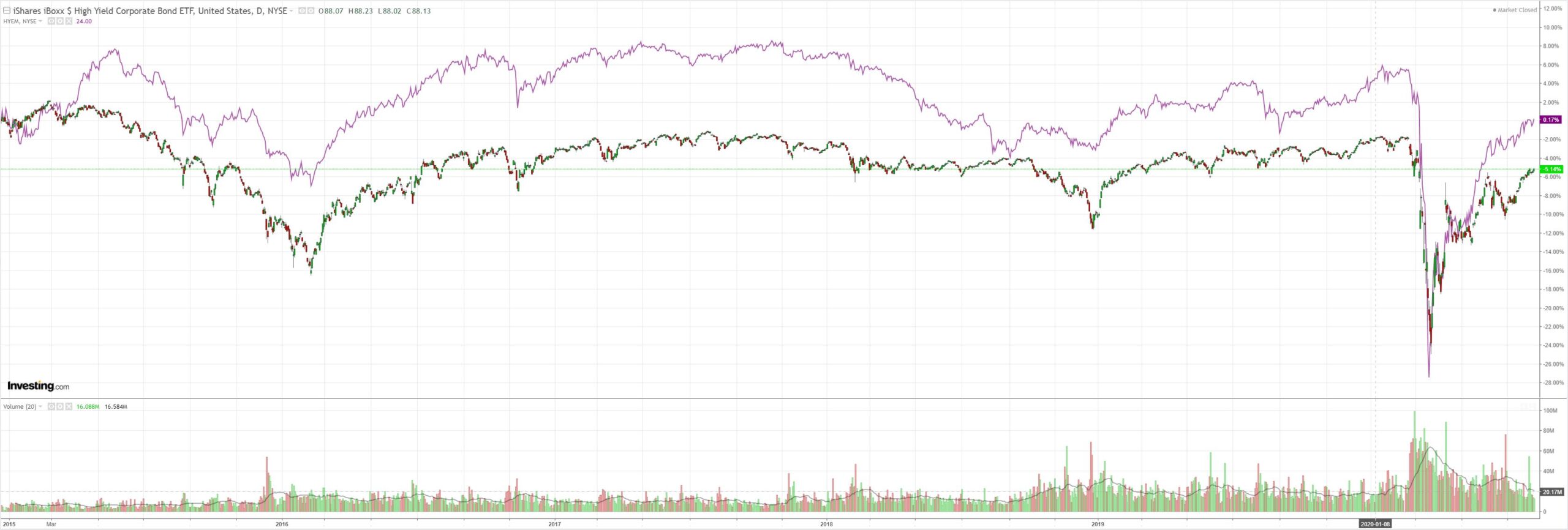

Junk fine:

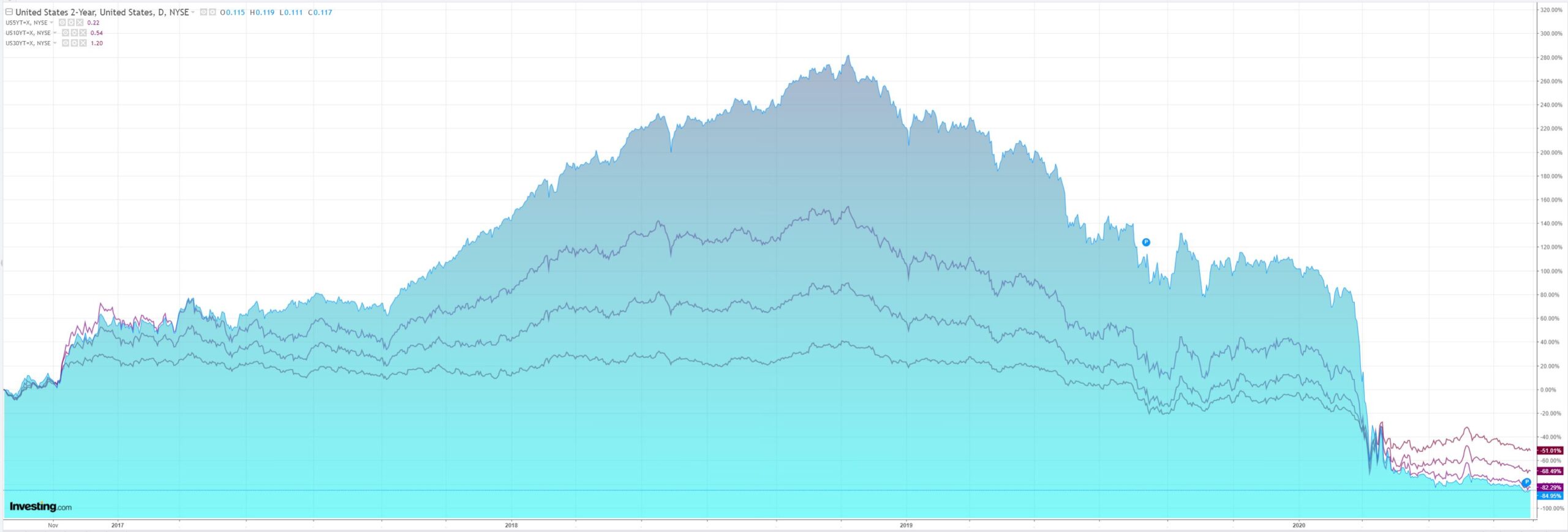

Yields squashed:

Stocks mania though not Europe (or Australia):

The only chart that matters mattered:

Not much happened, via Westpac:

Event Wrap

US initial jobless claims fell 249k to 1,186k in the week ended 1 August (vs 1400k expected), halting a concerning rise in claims over the previous two weeks. Continuing claims declined 844k to 16,107k in the 25 July week (vs 16,900k expected). While the report is better than expected, it still reflects weakness in the labour market.

Event Outlook

Australia: The RBA will release full detail of its updated forecasts in the August Statement on Monetary Policy. Their assessment of the risks ahead will also be of interest. Assistant Governor Economic Luci Ellis will then speak via an ABE webinar.

China: July trade and foreign reserve data is due along with the Q2 current account detail.

US: Nonfarm payrolls are likely to throttle back sharply in July given the rise in new cases and the response of authorities. ADP and the ISM employment measures signal that risks are to the downside. The unemployment rate is likely to fall further, but only at the margin as a result. Average hourly earnings will round out the labour market detail.

We probably can’t go past one more char to explain the AUD with iron ore blasting through $120:

The Great Fakeflation continues without an economy onwards and upwards into whatever, taking the Australian dollar with it.

At least iron ore is real, I guess…