According to BofA:

Foreign firms looking to move their manufacturing processes outside of China in the wake of coronavirus could face $1 trillion in costs over five years, according to new Bank of America research.

However, the bank argues that such a move would likely be beneficial for companies in the long term.

Even before the pandemic, BofA’s survey of global analysts found that companies were shifting away from globalization and towards a more localized approach when it came to their supply chains. This was due to a host of factors that threatened the network that supplies modern factories, including trade disputes, national security concerns, climate change and the rise of automation.

However, in a new study, BofA Head of Global Research Candace Browning and her team suggested that Covid-19 has catalyzed the reversal of a decades-long shift in manufacturing from the U.S. and Europe to China.

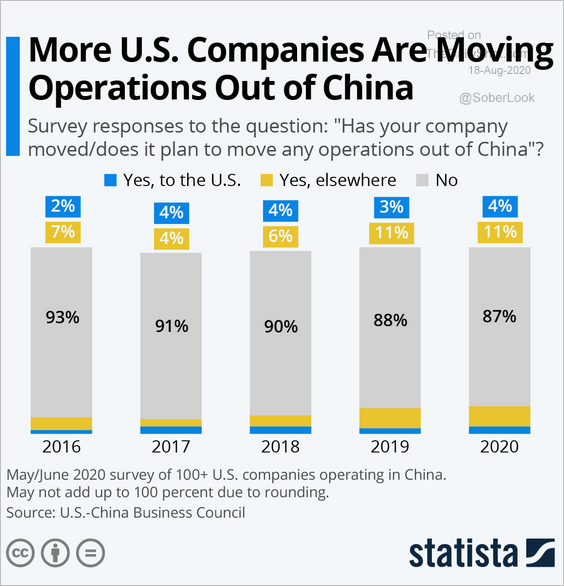

The report revealed that the pandemic had caused 80% of global sectors to face supply chain disruptions, forcing over 75% to widen the scope of their existing re-shoring plans.

“While Covid has acted as a catalyst to accelerate this change, the underlying reasons are grounded in a shift to ‘stakeholder capitalism,’ concluding relocation favors a broader community of shareholders, consumers, employees and the state,” Browning explained.

While each of these stakeholders was approaching relocation from a different perspective, the analysts observed that they were broadly drawing the same conclusion: that portions of supply chains should relocate ideally within national borders, but failing that to countries deemed “allies,” the report said.

Around two thirds (67%) of participants in BofA’s Global Fund Manager survey thought localization or re-shoring of supply chains would be the most dominant structural shift in the post-Covid world.

Shifting all export-related manufacturing that is not intended for Chinese consumption out of China could cost firms $1 trillion over five years, BofA projected.

The analysts said this would likely reduce return on equity by 70 basis points (bp) and free-cash-flow margins by 110bp, offset by a potentially lower risk premium. This would mean that the negative effects would be “significant, but not prohibitive,” analysts suggested.

Return on equity and free-cash-flow margins are both used by investors to asses a company’s profitability and ability to maintain its day-to-day operations.

In order to offset higher operating costs associated with this mass “re-shoring,” policymakers and corporate management would likely act aggressively, Browning’s team anticipated.

“We don’t expect a silver bullet, but we were struck by the universal declaration (in our survey) of intent to automate in future locations,” they revealed.

“Policymakers are also expected to help through tax breaks, low cost loans and other subsidies with recent announcements to that effect from the U.S., Japan, the EU, India and Taiwan (amongst others).”

On a sector level, BofA researchers suggested that stocks in construction engineering and machinery, factory automation and robotics, electrical and electronic equipment manufacturing, application software and other similar services would all stand to benefit from the acceleration of this trend. Meanwhile banks in North America, Europe and South Asia could also receive a boost from greater economic activity that comes with these changes.

It is happening and will accelerate:

Though not necessarily to home countries.

That means just one thing for Australia. China will decline into the middle-income trap meaning its growth slows even more quickly than it has been and commodity prices will fall away hugely from today’s stimulus highs.

The resulting tearing up of the CCP’s social contract with Chinese peoples – that exchanges freedom for prosperity – will end in the CCP invading Taiwan to rally nationalism in place of political legitimacy.

Warfare between the CCP and north Asian democracies will, in one form or another, end the flow of bulk commodities to China and trash Australian volumes after price.

We should have been preparing for this outcome for years already but we can still do ourselves some good by:

- massively taxing iron ore today and saving the proceeds in a sovereign wealth fund:

- blocking all Chinese takeovers and following the US example of non-commodity divestitures;

- pursuing any and all policies for a lower AUD to preserve and grow all non-commodity, non-China exports;

- massively incentivising the rebuilding of our industrial base using industry, energy and tax policy.

LOL!