Paul Keating is at it again, attacking those calling for a freeze in the compulsory superannuation guarantee (SG) at the current rate of 9.5%:

The argument that is now being put, erroneously, is that in a period of static real wage growth, any upward shift in the Superannuation Guarantee will cost workers immediate disposable income.

This is demonstrably untrue… were employees to lose the extra 2.5% of legislated superannuation, they would lose that income for the rest of their working lives, because they are certainly not going to get it in wages or somehow recover it later…

This week, the chairman of AMP, David Murray, gave a stern and stentorian warning saying a half point increase to super would be “economic madness” in the current climate…

Chris Richardson, of Deloitte Access Economics, was at it too. He went on to tell us that any further increase in the Superannuation Guarantee may not be “smart play” – arguing that even higher modest payments to super will lead to slower wages growth…

That in a period of static wage growth, an increase in the legislated Superannuation Guarantee is the only way ordinary working Australians will have returned to them, but a sliver of the labour productivity that they have provided – productivity that companies have been banking over the past seven years…

Commentators like Chris Richardson and David Murray, whether they realise it or not, are pawns in a wider game to sprag the Superannuation Guarantee, emanating deep from within the Liberal party…

The key message is this: in a period of flat to negative real wage growth, the only likely avenue to any real, though modest, increase in compensation is via the prospective increase in the Superannuation Guarantee Charge.

The cost of superannuation was never borne by employers. It was absorbed into the overall wage cost. Indeed, in each year of the SGC growth between 1992 and 2002, the profit share in the economy rose…

In other words, had employers not paid nine percentage points of wages as superannuation contributions to employee superannuation accounts, they would have paid it in cash as wages…

When you hear conservatives these days speak of superannuation as a tax on employers they are either ill-informed or they are lying…

Advertisement

Does Paul Keating suffer from amnesia? How is it that in 2007, compulsory superannuation was unambiguously paid for by workers through lower wage growth. But in 2020, it no longer is?

The RBA recently admitted that the SG is primarily paid for by workers via lower take-home wages:

RBA assistant governor Luci Ellis said it had “shaved” its worker pay forecasts to reflect that higher compulsory super will dampen future wage growth for private sector workers, offsetting wage increase pressures from a tightening labour market.

Wage growth would have got “a little bit of a pick-up from here” if not for the legislated requirement for business to boost their superannuation contributions, Dr Ellis said.

“Historically about 80 percent of the increase in the non-cash benefit tends to show up as somewhat slower wages growth than what you would have otherwise seen.”

Though compulsory SG contributions are paid by employees, wage setting generally takes into account all labour costs. It is widely accepted that employees bear the cost of higher SG in the form of lower take-home pay. This means there will be a trade-off between people’s income during their working lives and their income during their retirement.

Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

The increase in the superannuation guarantee to 12 per cent will likely lead to lower wage increases, shifting a greater proportion of earnings into the superannuation system.

A major challenge for retirement incomes policy is the need for current consumption to be deferred in favour of future income in retirement…

No loss of remuneration is involved in meeting this national challenge. What is involved, rather, is forgoing a faster increase in real take‑home pay in return for a higher standard of living in retirement.

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

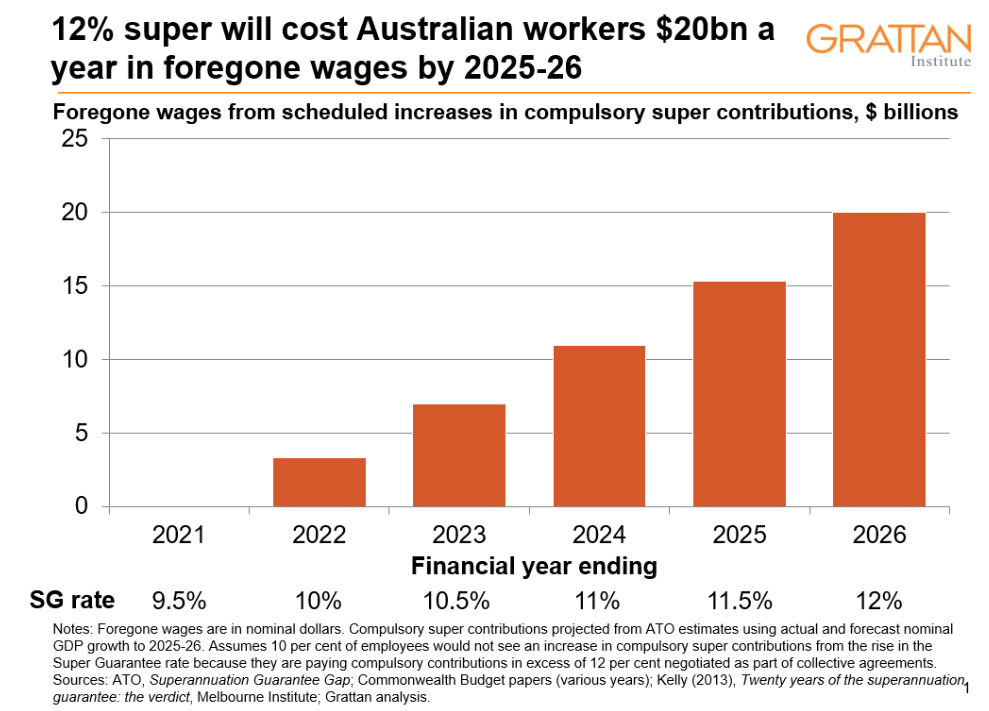

If compulsory super contributions go up, wages will be lower than they would otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP..

Are these organisations “pawns in a wider game to sprag the Superannuation Guarantee, emanating deep from within the Liberal party”. Obviously not.

Nor does Keating’s claim that “in a period of static wage growth, an increase in the legislated Superannuation Guarantee is the only way ordinary working Australians will have returned to them” make any sense.

Advertisement

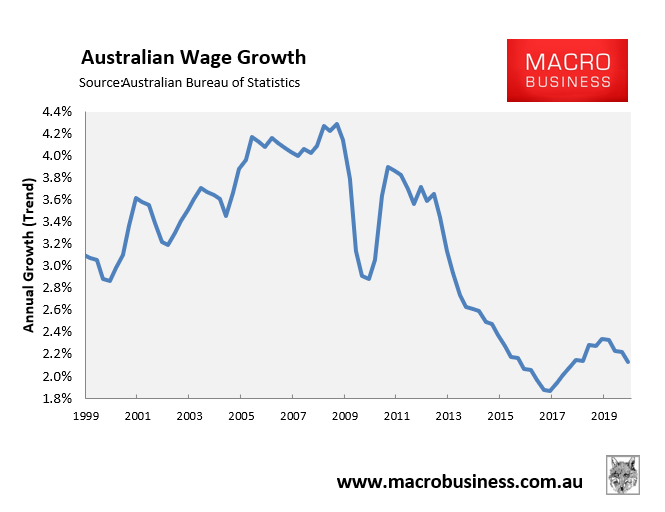

While real inflation-adjusted wages have stagnated, nominal wages have grown at an average of 2.1% over the past five years:

This gives employers plenty of scope to cut take home wages if the compulsory SG is increased.

Advertisement

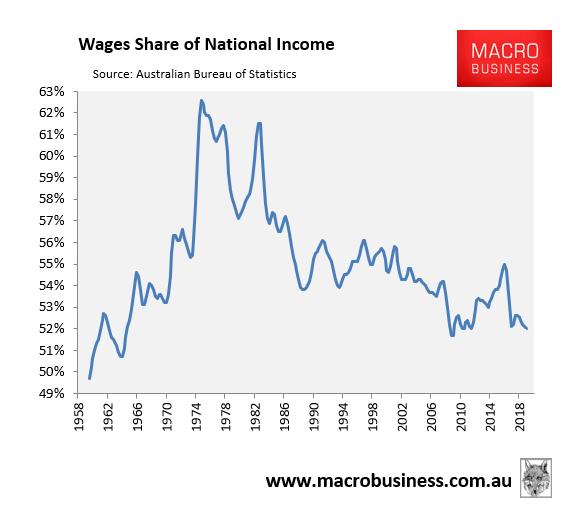

Seriously, why would employers voluntarily absorb the hit from increasing the SG when workers’ bargaining power and share of national income is at 50-year lows?

If bosses currently don’t feel pressured to give real wage rises, then why would they feel pressed to absorb further increases in the compulsory SG?

Advertisement

Moreover, the massive fall in the labour income share in Australia over the period when the SG was increasing is inconsistent with Keating’s new found suggestion that employers absorbed the cost of super.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.