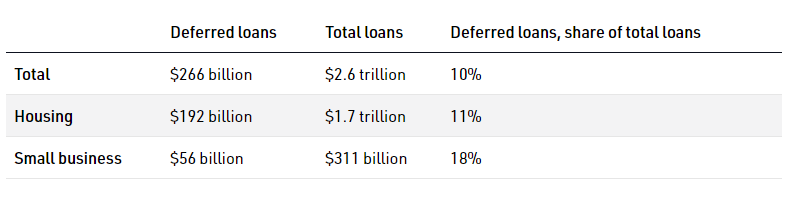

The Australian Prudential Regulatory Authority (APRA) released some alarming data late last week on mortgage deferrals.

According to APRA, $192 billion of mortgages have been deferred by authorised deposit-taking institutions (ADIs), comprising 11% of all housing loans:

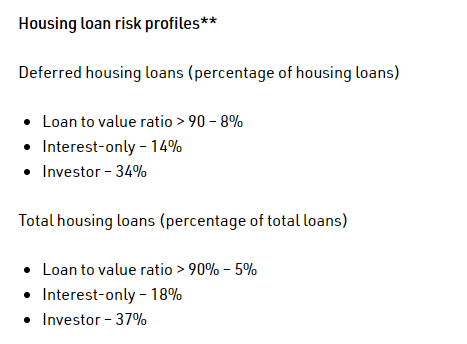

Worse, more than one-third of investor mortgages have been deferred, a large proportion of which are interest-only:

Advertisement

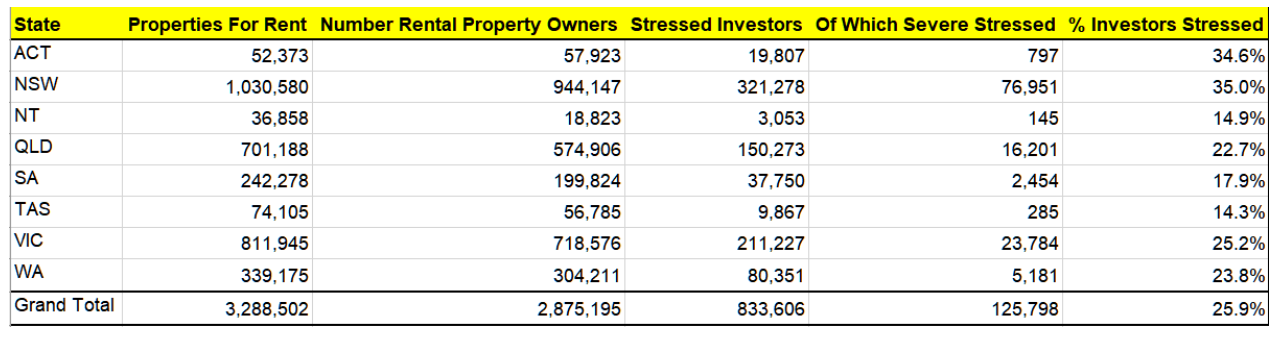

As reported earlier this month by Martin North, one quarter of property investors (more than half with a mortgage) are suffering negative cash flow on their investment. That is, their holding costs are greater than their investment property income:

Of these 2.8 million entities, around 830,000 on a cash-flow basis, are not making sufficient to recover the costs of owning and letting their properties (stressed investors) of which 126,000 are severely stressed, most often because of low occupancy, or high repair costs. This is around 25.9% of all investment property, and 51.3% of mortgaged properties…

“The growth that you might have anticipated might not come, so at some stage you’re going to have to say: ‘If I can’t afford this mortgage, am I better off to rent, put my capital aside and wait until I’m in a better position to buy back into the market?’”…

“Some of those customers, I think, will say ‘I just can’t see how I can trade my way out of this,’ and will be wise enough to cut their losses”…

That is wise advice. But it also increases the rise of a feedback loop, where falling prices causes more investors to sell, which causes further price falls, etc.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.