Around 3.5 million workers are receiving JobKeeker payments and 1.6 million are relying on JobSeeker. This means approximately 42% of Australia’s 12.1 million-person workforce is being supported via these government schemes.

Mozo’s data showed the vast majority of these people (92%) require this support to remain financially stable. In addition to the worrying housing situation, a third of surveyed income support recipients said they would not be able to afford to pay their bills if the payments stopped, with a fifth also unable to cover the cost of groceries…

This amounts to approximately 1.3 million Australians potentially unable to keep a roof over their heads…

“With the jobs market on life support, JobKeeper and JobSeeker payments are critical in ensuring people can remain in their homes and have enough money to cover necessary expenses,” Mozo Director Kirsty Lamont said.

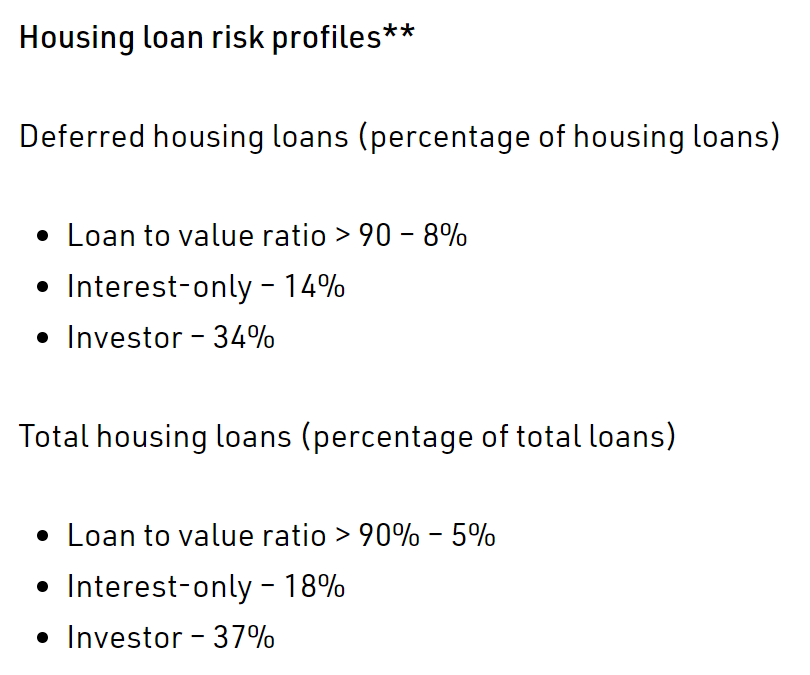

According to APRA research earlier this month, just under half a million Australian households had deferred a total of $192 billion worth of mortgages (11% of total mortgages) as at 31 May. Property investors are under particular pressure, with around one-third of investor mortgages deferred, according to APRA:

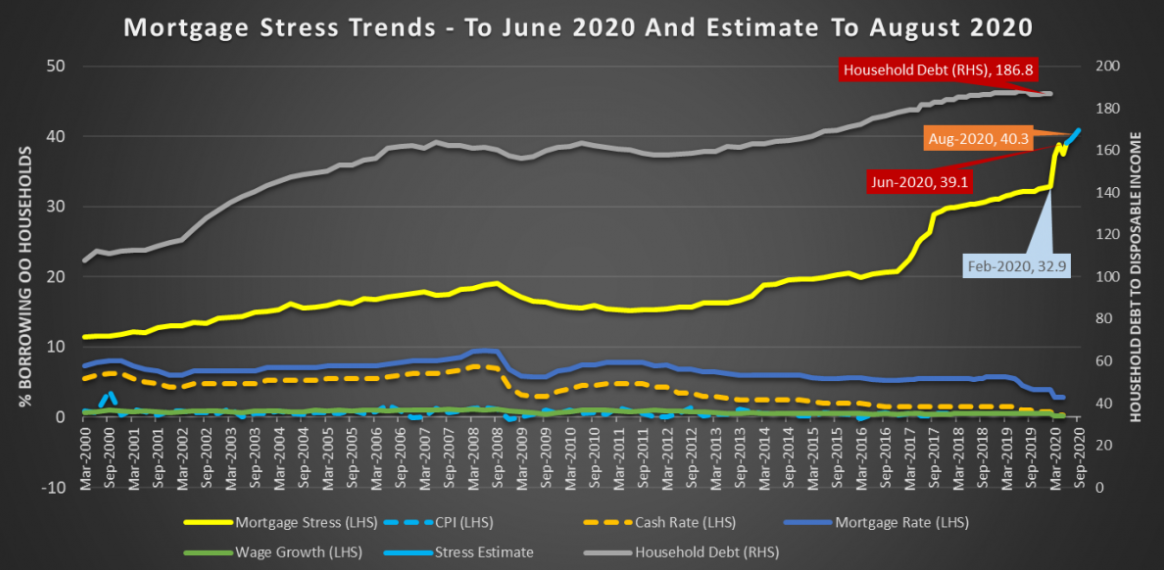

Separate data from Digital Finance Analytics (DFA) also revealed that the percentage of borrowing households experiencing mortgage stress was a record high 39.1% in June, equating to 1.47 million owner occupied mortgage holders experiencing financial pressure:

Investors are most exposed, with DFA noting that “a larger number of property investors with a mortgage (51.3%) are underwater from a cash-flow perspective… which suggests investors are caught in the financial crisis headlights”.

The rise in investor stress is especially pertinent given both rents and prices are now falling.

How long will speculators hold on to these loss-making properties when prospects for capital growth are slim and the labour market is so fragile?

While announced extensions to JobKeeper, JobSeeker and mortgage deferrals will help, struggling households are still facing reduced levels of support from October.

Thus, there is the clear risk that loss-making investors, in particular, could sell in large numbers, causing a feedback loop of further property price falls and forced sales.