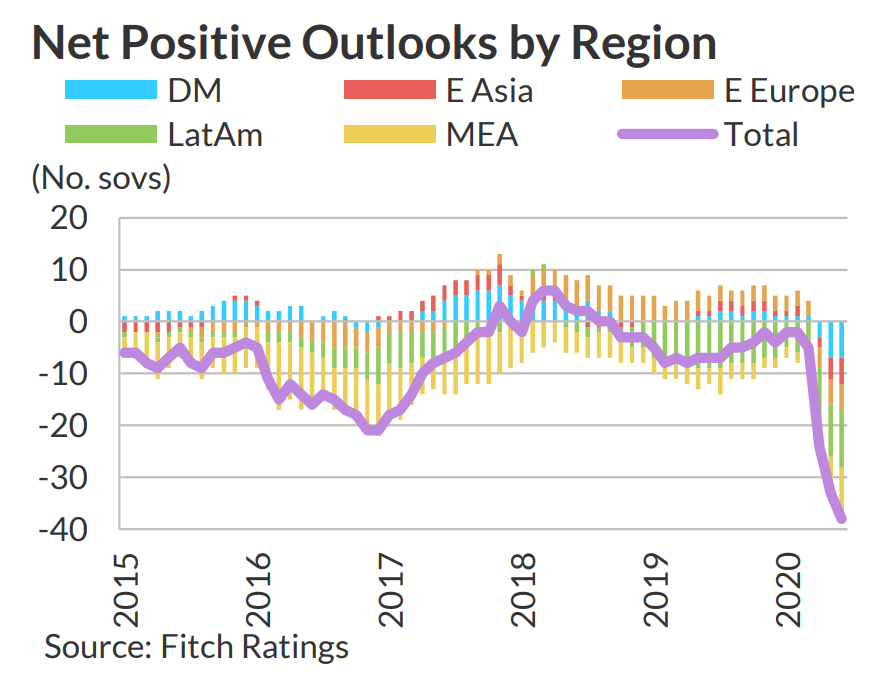

There were more sovereign downgrades in 1H20 than any full year prior, and 40 sovereigns are on Negative Outlook, a record high in absolute terms and as a share of the rated portfolio, Fitch Ratings says.

The coronavirus pandemic is exerting considerable pressure on sovereign creditworthiness across all regions and rating categories, as governments bear the costs of severe recessions combined with health crises. Emerging-market sovereigns are additionally confronted with external financing strains associated with commodity price fluctuations, currency swings and changes in investor risk appetite. Global policy responses have been sizeable and swift, but leave governments with higher debt burdens while still facing uncertainties around the economic outlook and the future path of the virus.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.