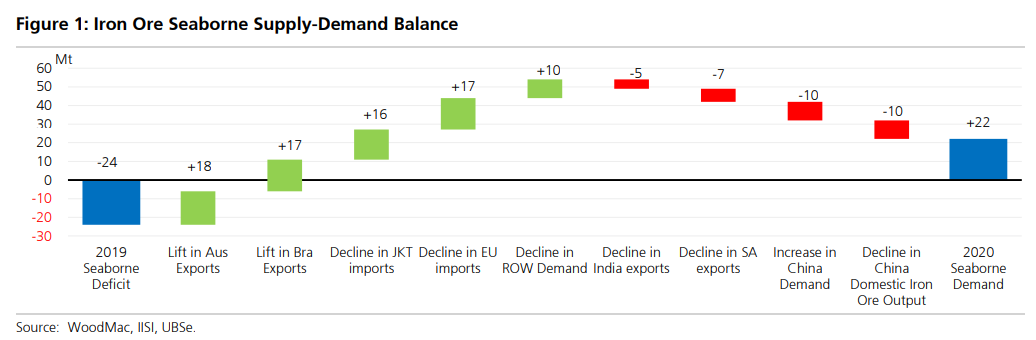

Iron ore appears well-supported by current tightness

The iron ore price (62% CFR China) has averaged US$89/t YTD with spot now over US$100/t and above our CY 20e forecast of US$86/t. We are comfortable with our forecast based on 1) a strong recovery in Vale iron ore production which will require a 70-90Mt lift in 2H 20 to meet guidance (UBSe: 1H: ~120Mt, 2H: ~200Mt) & 2) mobility

restrictions easing in S. Africa & India, bringing supply into the market to alleviate current tightness. Uncertainty remains elevated due to COVID-19 so we’ve developed an interactive model of the steel & iron ore market to help model a range of scenarios through flexing assumptions on steel demand growth & iron ore supply.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.