No reliable official Indian data for April or May. The Indian Ministry of Statistics & Programme Implementation (MSPI) has halted the official releases of industrial production (IP) and consumer price index (CPI) estimates, providing instead “quick” estimates of IP, and partial food CPI data. Specifically on the IP data, The MSPI has said that in light of shutdown measures to contain the spread of the COVID-19 pandemic, the majority of industrial sector establishments have not been operating since the end of March 2020. This has had an impact on the items being produced by the establishments during the month of April 2020, where a number of responding units have reported “nil” production. Consequently, officials have suggested that it has become “inappropriate” to compare IP estimates for April 2020 with earlier months, and users of the data have been guided to track IP growth from the “re-based” April reference point instead.

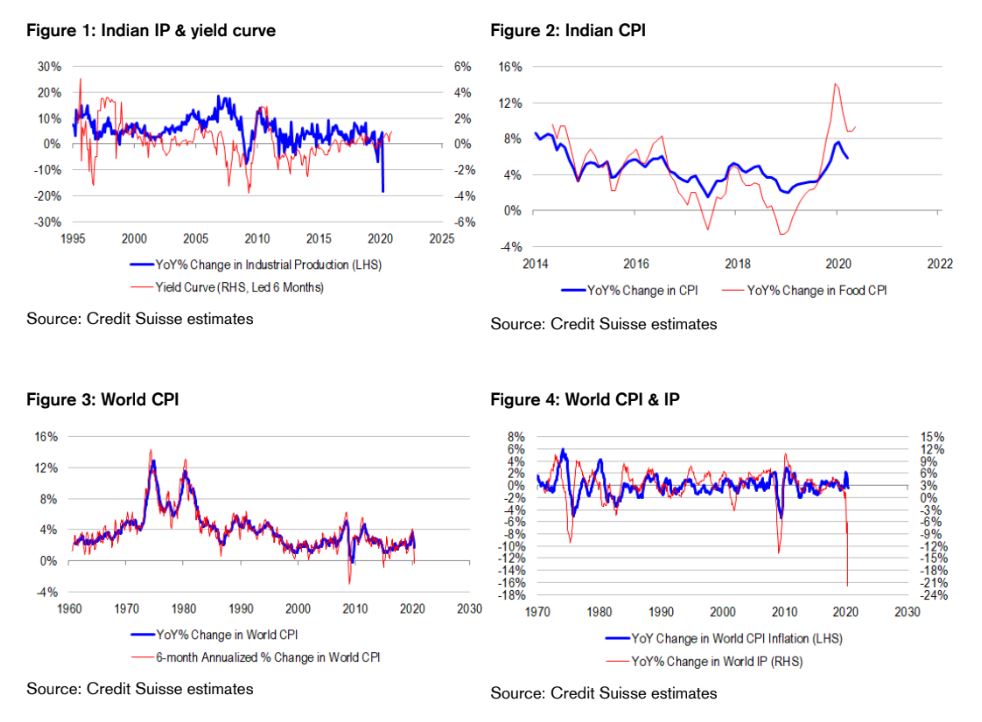

What little data are available for India point to stagflation. Although the MSPI is suggesting that recent IP estimates are unreliable or uncomparable to the past, it is nevertheless providing “quick” estimates of IP on the same indexed basis as previous data. And if the raw data are anything to go by, Indian IP is down a staggering 57% in the year-to-April. If accurate, this would be the fastest pace of contraction in all of the major economies to date. Effectively, India is experiencing a depression, and the world ought to take note because the economy represents almost 15% of world gross domestic product (GDP) on a purchasing power parity (PPP) basis. One would think that with the economy shrinking so rapidly, that deflation would be inevitable. But the data suggest otherwise. The latest available official CPI data for March point to year-ended headline inflation of 5.8%. Since March, we only have food CPI numbers – but these are significant because food represents roughly 40% of the Indian consumption basket. And in the April-May period, we note accelerating food CPI inflation to 9.3% from 8.8% in March. In other words, it is highly unlikely that India is in deflation, despite the sharpest decline in IP on record.

The Indian outlook is very uncertain. The Indian yield curve, measured as the spread between 10-year government bond yields and 3-month interbank rates, is upward sloping. Investors expect rates to rise medium term, which can only make sense if they also expect recovery. And historically, the yield curve is a useful leading indicator of Indian IP growth momentum. From deeply negative growth rates, the yield curve is now pointing to recovery. But the trouble is that the yield curve is not proving very useful in this cycle as a leading indicator. It is failing to tell us much about the depth of the COVID-19 shock to the economy, let alone potential recovery dynamics, because monetary policy is not the binding constraint on the economy. Instead, the virus curve is proving to be the better signal. Worryingly, India is exhibiting one of the steepest virus curves in the world – one of the worst infection growth rates in the world, alongside Brazil. Even more concerning is the fact that attempts to shutdown the economy are not working very well to flatten the virus curve, unlike the experiences of other major economies. In most developed economies, shutdown restrictions have become more stringent, slowing the spread of the pandemic with a delay, and enabling more recent relaxation of restrictions. But in India and Brazil, infection counts have shown very little responsiveness to more stringent conditions. Indeed in India, infection counts have risen sharply and shutdown restrictions have been relaxed despite the absence of evidence that there had been much progress in fighting the pandemic to begin with. Indian policy makers have shown some reticence to shut down more of the economy to deal with the pandemic – but the private sector might have done the job for them with confidence clearly undermined.

The virus is still out there. The Indian and Brazilian experiences are reminding us about the ongoing risks from COVID-19 in the absence of an effective cure, vaccine or treatment. Never mind a second wave of the outbreak – India and Brazil are still dealing with the first wave. And for what it is worth, there is emerging evidence of a second wave of infections in some developed economies now that many of them are starting to ramp up again. From a domestic cyclical perspective, we see risks that soft border closures could remain in place for longer given that the first wave of the virus is still thriving in major parts of the world and that mutations are quite possible. Indeed, of the 240K net overseas migration into Australian in 2018-19, migrants from India alone make up roughly 70K, or 29% of the annual flow. And if border restrictions remain in place, the risk is that housing and related sectors suffer from reduced population growth and household formation rates. The policy outlook is becoming especially interesting now that New Zealand is claiming victory over the pandemic after implementing extreme shutdown measures, creating pressure on Australian policy makers to achieve and hold similar outcomes. After all, New Zealand might not have economic outcomes to boast about – but at least policy makers can say that they have eliminated chains of community transmission for almost a month and are in a position to effectively prevent or contain any future imported cases from overseas. But in Australia, policy makers can neither point to strong economic outcomes nor technical elimination of the virus just yet. To be sure, policy makers are taking the view that the spread of the virus is broadly under control, that reopening needs to happen quickly and that the economy is on the road to recovery. They are even thinking about ways to enable foreign students to return to Australia to support the education and residential property sectors. However, the decision to open borders to support the economy is a weighty and risky one, while technical elimination of the virus is a very achievable and substantial win provided that border restrictions remain in place.

India is cyclically and structurally significant from a global perspective. Beyond the immediate implications of the Indian outlook for Australia, we think that India typifies the stagflation problem facing the world. Inflation is not coming down materially despite a deep and negative shock to output. Therefore, one can only imagine how much inflation could accelerate in a recovery scenario (which incidentally, we cannot completely rule out for India, if the Western world recovers strongly, supporting exports). Structurally, we are concerned that India is such a large part of the world to be offline for an extended period of time. We think that companies are actively looking to secure their supply chains, regardless of competitive advantages or disadvantages. And in this context, ongoing problems in India are likely to harden their stance on reclaiming their production facilities from abroad. De-globalization is becoming very hard to reverse in the circumstances.

Still overweight resources. In previous cycles, we would look at deep contraction in Indian and emerging market (EM) economies as reasons to sell commodity exposures. Indeed, we are still tempted to think along these lines. However, the issues are that the financial demand for commodities matters as much as physical, and that physical commodity supply is being disrupted too by COVID-19 (notably Brazilian iron ore production). While it is difficult to say how long the supply side disruptions will go on for, what we can say is that in the interim, investors could focus on the reflationary impulses from de-globalization, loss of productive capacity and overwhelming money creation (stimulus), and therefore seek out inflation hedges like commodity exposures. Historical relationships suggest that when world CPI inflation momentum is resilient to a downturn in world IP, that resources stocks tend do much better than EM equities, because they are more than just EM plays – they are inflation plays too. Also, our proprietary pipeline inflation indicator based on timely business survey data points such as order backlogs, supplier delivery times and input prices, is pointing to considerably higher inflation pressure in the period ahead than what bond market investors are pricing in. In our view, there is room for a re-rating of inflation expectations, supporting all inflation hedges. Gold stands out to us, as it is less dependant on usage value than other industrial commodities. Having said this, many commodities look cheap in gold terms, and could easily experience inflation with gold. From an Australian equity market perspective, we are also comforted by the fact that larger capitalization names in the resources space have strong balance sheets and good cashflow, an therefore rank well on quality metrics. In contrast, we are concerned about the health of housing-related stocks, in the building, consumer and financial sectors, because of the risks that migration will remain lower for longer for as long as COVID-19 is out there without a cure, vaccine or treatment.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.