Despite Australian workers facing massive income declines, Labor continues to lobby hard for the superannuation guarantee (SG) to be lifted to 12%:

Senior Labor figures said compulsory super, which originated under the Hawke government’s accord process in the 1980s, should be protected as the Morrison government forged a new compact with unions and business to negotiate workplace reforms…

Labor leader Anthony Albanese, who has been excluded from negotiations, said the party held dear the 12 per cent guarantee.

“The accord and enterprise bargaining was successful because it incorporated a social wage including boosting retirement incomes through compulsory superannuation,” he said.

“Coalition governments have used every opportunity to undermine super, including the current process that has seen more than $13 billion taken from accounts.”

When will Labor admit that the SG is paid for via salary sacrifice from workers? This means that workers take home lower wages today in exchange for bigger superannuation balances at retirement. It also means that lifting the SG to 12% from 9.5% currently will necessarily lower workers’ disposable incomes (other things equal).

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

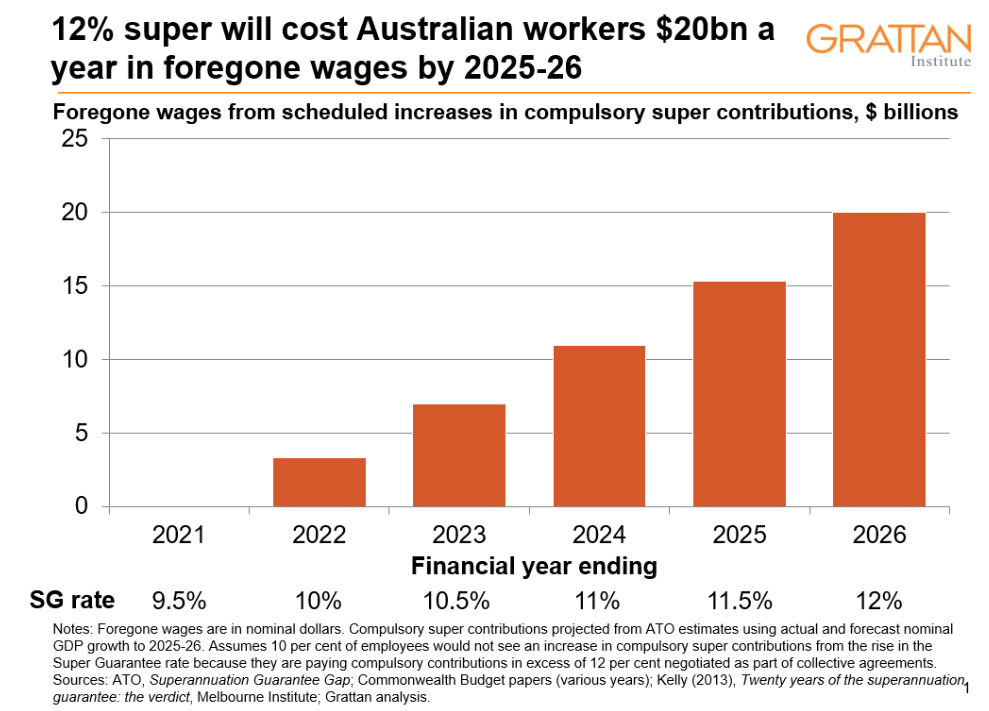

If compulsory super contributions go up, wages will be lower than they otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP…

RBA assistant governor Luci Ellis said it had “shaved” its worker pay forecasts to reflect that higher compulsory super will dampen future wage growth for private sector workers…

“Historically about 80 percent of the increase in the non-cash benefit tends to show up as somewhat slower wages growth than what you would have otherwise seen.”

Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

Because it’s wages, not profits, that will fund super increases in the next few years. Wages are the seedbed of the whole operation. An increase in super is not, absolutely not, a tax on business. Essentially, both employers and employees would consider the Superannuation Guarantee increases to be a different way of receiving a wage increase.

And here’s former Labor Prime Minister and Treasurer, Paul Keating:

The cost of superannuation was never borne by employers. It was absorbed into the overall wage cost… In other words, had employers not paid nine percentage points of wages as superannuation contributions to employee superannuation accounts, they would have paid it in cash as wages.

Advertisement

How much more evidence does Labor need before it admits that its 12% superannuation fetish will rob workers of much needed disposable income?

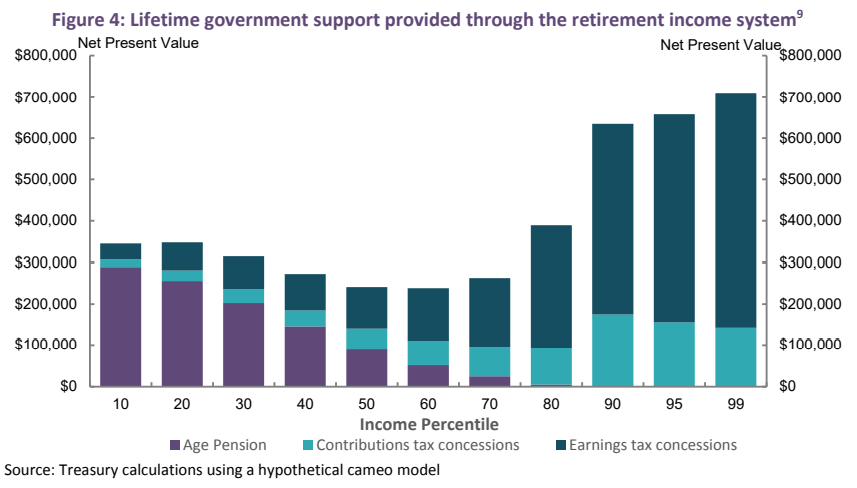

Perhaps even worse, 12% superannuation will also worsen inequality, since the lion’s share of concessions flow to high income earners, according to the Australian Treasury:

Advertisement

Moreover, because it gives higher income earners the lion’s share of concessions, compulsory superannuation costs the federal budget more than it saves in Aged Pension costs. The Grattan Institute, the Henry Tax Review, and actuarial firm Rice Warner are explicit on this point.

Indeed, the Grattan Institute estimates that lifting the SG to 12% would cost the federal budget an additional $2 billion a year in lost income:

In both the short and long term, though, superannuation costs the budget more than it saves, because the tax breaks cost the government more than the pension savings…

Advertisement

Any objective analysis would conclude that raising the SG to 12% is poor policy, given it would: 1) lower workers’ disposable income; 2) increase inequality; and 3) worsen the long-term sustainability of the federal budget.

The only real winners from this policy are Labor’s industry superannuation mates, which will get to ‘clip the ticket’ on bigger funds under management.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.