Former Labor Prime Minister, Kevin Rudd, claims“Scott Morrison’s crusade on super is the biggest attack on working Australians since WorkChoices”:

Scott Morrison’s crusade against compulsory superannuation marks the greatest assault on the living standards of working Australians since John Howard’s WorkChoices industrial laws took the meat axe to wages and conditions…

If Morrison succeeds, it may boost his popularity among neoliberal zealots. But it will entrench stark inequalities between rich and poor. With the levy frozen at its current rate, a 30-year-old worker earning $40,000 a year will have the equivalent of $10,000 less each year in retirement…

First, they claim, it will boost wages. Yet if this were true, wages would have rocketed during Abbott’s freeze. Instead, wages flatlined while company profits soared. This was a direct transfer of wealth from working people to corporate executives…

Our super system has become the envy of finance ministers, treasurers and the financial world. It protects national budgets by reducing radically the future call on the age pension.

What complete and utter tosh.

First, compulsory superannuation is unambiguously paid for by lower take home wages. Think about it from an employer’s perspective. They are only concerned about their total wages bill, not what proportion of wages is paid to employees versus paid into a superannuation account.

Therefore, lifting the superannuation guarantee (SG) to 12% from 9.5% currently will necessarily lower workers’ disposable incomes (other things equal).

Advertisement

If you don’t believe, here’s the findings of the Henry Tax Review, which was commissioned by Kevin Rudd:

Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

RBA assistant governor Luci Ellis said it had “shaved” its worker pay forecasts to reflect that higher compulsory super will dampen future wage growth for private sector workers…

“Historically about 80 percent of the increase in the non-cash benefit tends to show up as somewhat slower wages growth than what you would have otherwise seen.”

Even slower wage growth will be the result of increasing compulsory superannuation contributions from 9.5 per cent to 12 per cent…

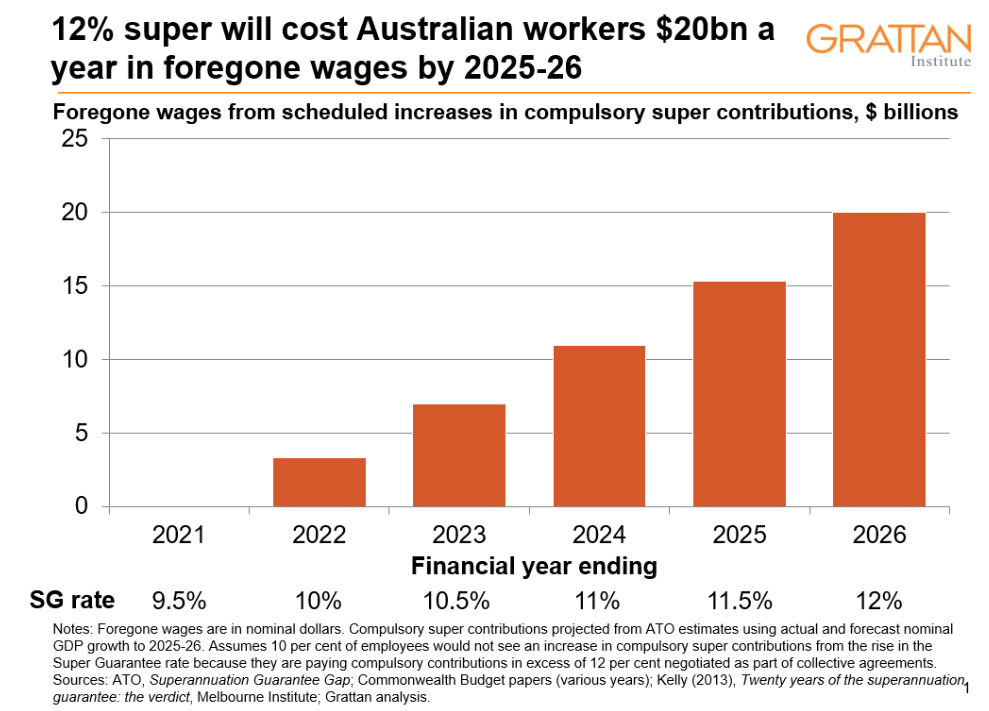

If compulsory super contributions go up, wages will be lower than they otherwise. And the cut to wages from raising compulsory super is big. Really big. By the time it’s fully implemented in 2025-26, a 12 per cent Super Guarantee will strip up to $20 billion from workers’ wages each year, or nearly 1 per cent of GDP…

Advertisement

Heck, even Bill Shorten as assistant treasurer in the former Labor Government admitted in 2010 that SG increases were paid for by workers through lower wage rises:

“Because it’s wages, not profits, that will fund super increases in the next few years. Wages are the seedbed of the whole operation. An increase in super is not, absolutely not, a tax on business. Essentially, both employers and employees would consider the Superannuation Guarantee increases to be a different way of receiving a wage increase.”

As did compulsory superannuation’s founder, Paul Keating:

Advertisement

The cost of superannuation was never borne by employers. It was absorbed into the overall wage cost… In other words, had employers not paid nine percentage points of wages as superannuation contributions to employee superannuation accounts, they would have paid it in cash as wages.

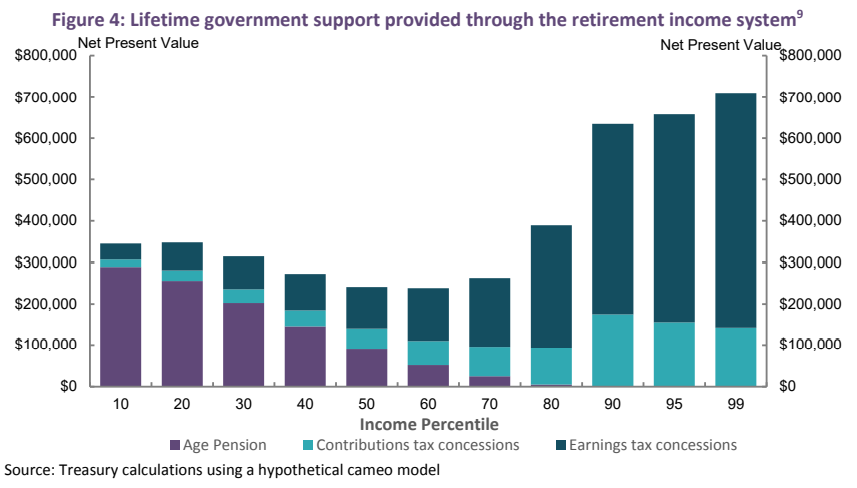

Second, lifting the SG to 12% will unambiguously increase inequality, given the lion’s share of concessions flow to high income earners, according to the Australian Treasury:

Advertisement

As shown above, higher income earners receive a disproportionate share of superannuation concessions.

For example, the top 1% of earners will receive more than $700,000 in superannuation concessions over their working lives, dwarfing the $50,000 of concessions received by the bottom 10% of income earners.

Therefore, Australia’s compulsory superannuation system enshrines inequality by concentrating asset ownership among the wealthy. And lifting the SG to 12% will only make the situation worse.

Advertisement

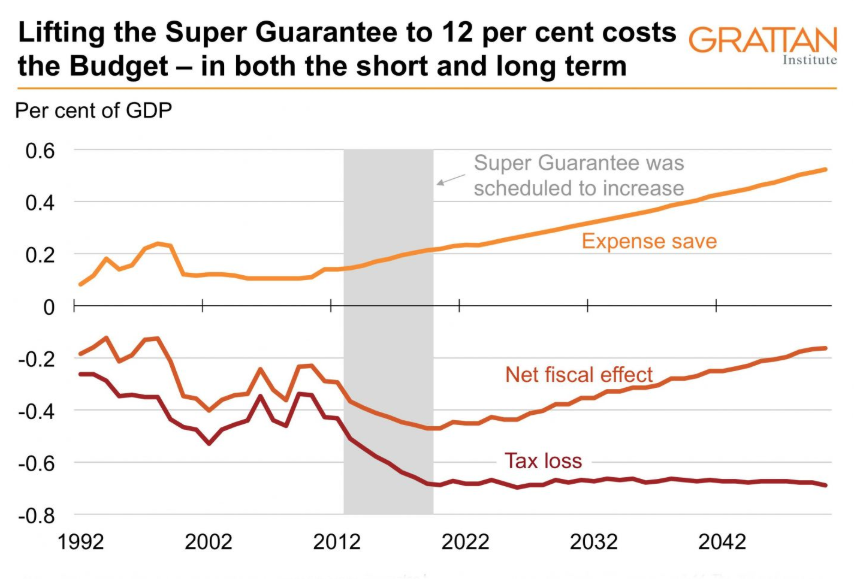

Third, and related directly to the above, lifting the SG to 12% will wreck the long-term sustainability of the Budget.

Because the lion’s share of concessions go to those that do not need them – i.e. high income earners – the budgetary cost of concessions outweighs any gains from lower expenditure on the Aged Pension.

Indeed, the Grattan Institute forecasted that lifting the SG to 12% would cost the federal budget an additional $2 billion a year in additional tax breaks, creating a net drain on the Budget over the long-run:

Advertisement

The purpose of superannuation is to save for the future and reduce future age-pension payments. In both the short and long term, though, superannuation costs the budget more than it saves, because the tax breaks cost the government more than the pension savings.

Actuarial firm Rice Warner said that lifting compulsory super contributions to 12% would not have much impact on the age pension for many years, and would save the budget only about 0.1% in lower age pension spending in the second half of this century.

In contrast, extra super tax breaks from higher compulsory super would cost an average of 0.22% of GDP “through this century”…

An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).

What part of the story does Kevin Rudd not understand? The Henry Tax Review explicitly recommended that his government not lift the SG, and yet he did so anyway. And here he is continuing to press the case based on lies.

Advertisement

Australia’s superannuation system is really more of a tax avoidance scheme for the rich than a genuine retirement pillar.

The only real winners from this policy are Labor’s industry superannuation mates, which get to ‘clip the ticket’ on bigger funds under management at the expense of working Australians and taxpayers.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.