MacroBusiness has gone to great lengths over many years to explain why Australia’s compulsory superannuation system is not a genuine retirement pillar and is ripe for reform. This comes despite us offering a superannuation fund via our partners at Nucleus Wealth. Thus, we are effectively talking against our own book.

We see five fundamental problems with Australia’s compulsory superannuation system.

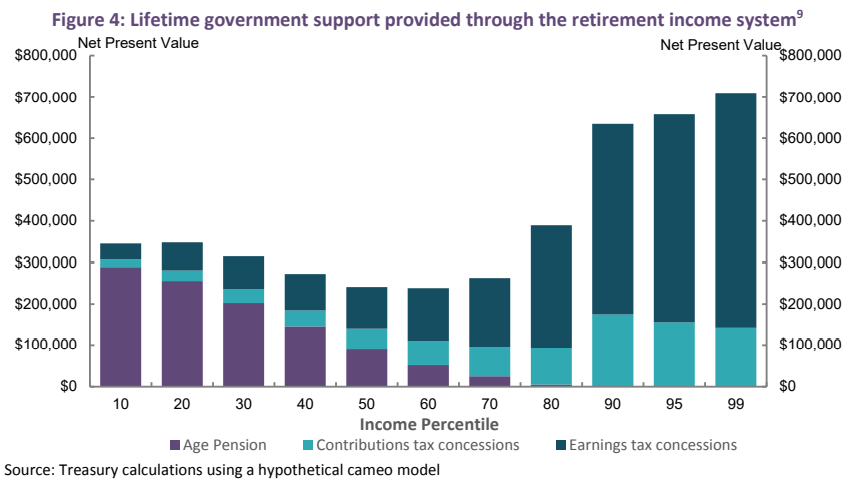

First, the overwhelming majority of superannuation concessions go to those that need them least (high income earners) and misses those that need them the most (lower income earners).

This is highlighted most clearly by the below Australian Treasury chart, which shows that the top 1% of income earners will receive roughly 14-times the superannuation tax concessions over their working lives ($700,000) than the bottom 10% of income earners ($50,000):

Second, because superannuation concessions flow mostly to those that do not need them and were unlikely to ever utilise the Aged Pension anyway, the cost of superannuation concessions to the federal budget far outweighs their savings from lower Aged Pension expenditure.

Third, Australia’s superannuation system is highly inefficient. Australia’s management fees are among the highest in the world with Australian households spending twice as much each year on superannuation fees as they do on electricity.

The number of people employed in the superannuation industry is also astronomical, dwarfing Australia’s entire welfare system and on par with our entire defence force and its bureaucracy.

Fourth, superannuation is voluntary for the self-employed. Therefore, it misses millions of Australian workers.

Finally, superannuation can be withdrawn in full and spent from 60 years of age – way before the official retirement age of 66 (rising to 67). This means that many will quickly exhaust their superannuation funds before retirement and then fall back on the Aged Pension.

In contrast to superannuation, the Aged Pension system suffers from none of the above pitfalls and is Australia’s true retirement pillar.

The Aged Pension is available universally as soon as one reaches retirement age, provided they are not already wealthy.

Because it is means tested, the Aged pension is targeted towards those that need it most – low income earners – rather than being used for tax minimisation by the wealthy.

The Aged Pension is not based on how long one works or how much they earned during their working lives.

And finally, the Aged Pension is far more efficient, with Australia’s entire welfare system costing only $6 billion per year and employing only 33,000 people, while providing $45 billion in pension benefits.

Given the above, the first best policy response would be to disband the compulsory superannuation system and redeploy the budget savings into the Aged Pension system.

However, given how embedded the superannuation system is, this will never happen. Therefore, policy makers should instead focus on limiting the damage by making the compulsory superannuation system more efficient and equitable.

Two low-hanging fruit options immediately come to mind:

- Abandon the legislated increase in the superannuation guarantee to 12%, since this will merely accentuate the above problems.

- Change the superannuation concession structure from a 15% flat tax on superannuation contributions/earnings to a flat 15% concession (i.e. marginal tax rate less 15%). This will give more benefits to lower income earners and less to higher income earners.

While the above measures won’t fix the myriad of underlying problems in superannuation, they are simple and will at least stop the system from getting worse.

Policy makers should use the COVID-19 pandemic to drive superannuation reform.