An interesting debate emerged at The AFR yesterday with regards to Australia’s compulsory superannuation system.

Pitcher Partners director, Brad Twentyman, proposed allowing workers to cash out half of their superannuation contributions over the next 18 months in order to lift disposable income and save the federal budget around $10 billion:

[It] would be “one of the most effective ways” to support households and the economy without increasing government debt…

“With the super guarantee halved, this would equate to a $10 billion boost to the federal budget, assuming all Australians who currently contribute to super participated,” Mr Twentyman said.

By contrast, Mercer senior partner, David Knox, argued that the COVID-19 economic meltdown reinforces the need to lift the superannuation guarantee (SG) from the current 9.5% to 12%:

Advertisement

[Knox] said with long-term investment returns set to fall from inflation plus 4 or 5 per cent, down to 2 or 3 per cent, the government should forge ahead with the scheduled increase, which was set to lift the SG by 0.5 per cent next year.

“In the post COVID-19 environment things are going to be different,” Dr Knox said.

“If we’re earning 5 per cent then money doubles in 14 years. But if we’re earning 3 per cent money doubles in 22 or 24 years.”

Compulsory superannuation is paid for by workers via reducing their take-home pay. Therefore, reducing the SG would lift disposable income, whereas raising the SG would lower it (other things equal).

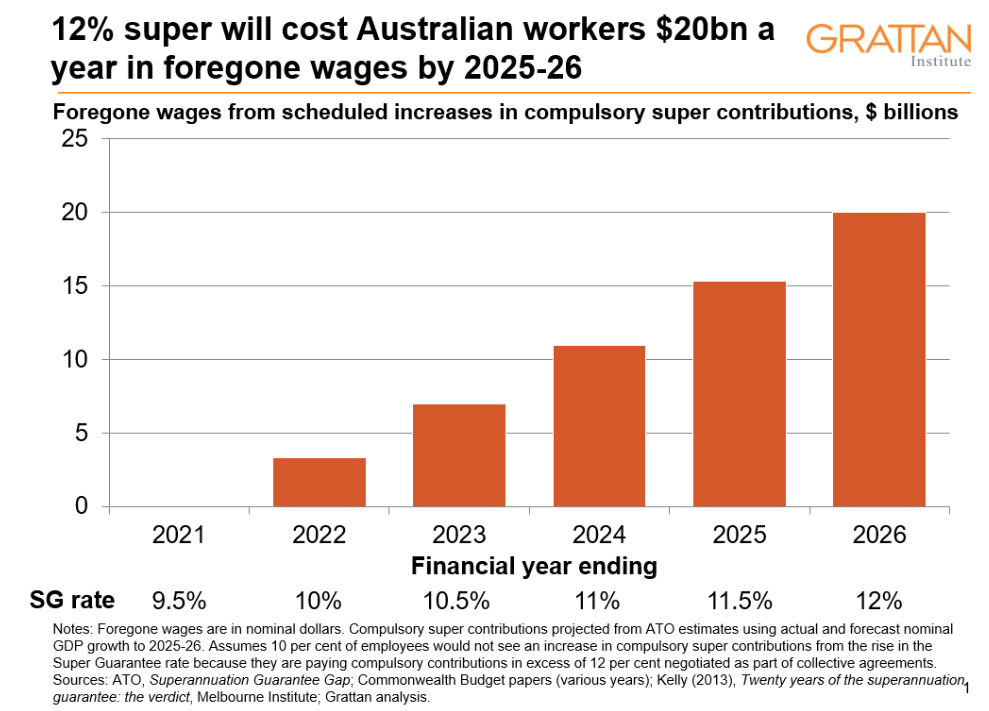

For example, the Grattan Institute forecast that raising to SG to 12% would cost Australian workers $20 billion a year in foregone take-home wages once fully implemented in 2025-26:

Advertisement

The Henry Tax review and the Reserve Bank of Australia have also concluded that raising the SG would lower wages (other things equal).

Lifting the SG would also have a detrimental impact on low income earners struggling to make ends meet and living paycheck to paycheck. This is why the Henry Tax Review explicitly recommended against it:

Advertisement

“Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners”.

There is also the huge cost to the federal budget.

As noted in The AFR article:

Advertisement

About $30 billion flows into the $3 trillion super system each quarter, or about $120 billion a year. Compulsory superannuation contributions are taxed at concessional rates, resulting in foregone budget revenue worth $19 billion a year.

An additional 15 per cent concessional rate on investment earnings results in the system costing $43 billion in tax concessions each year.

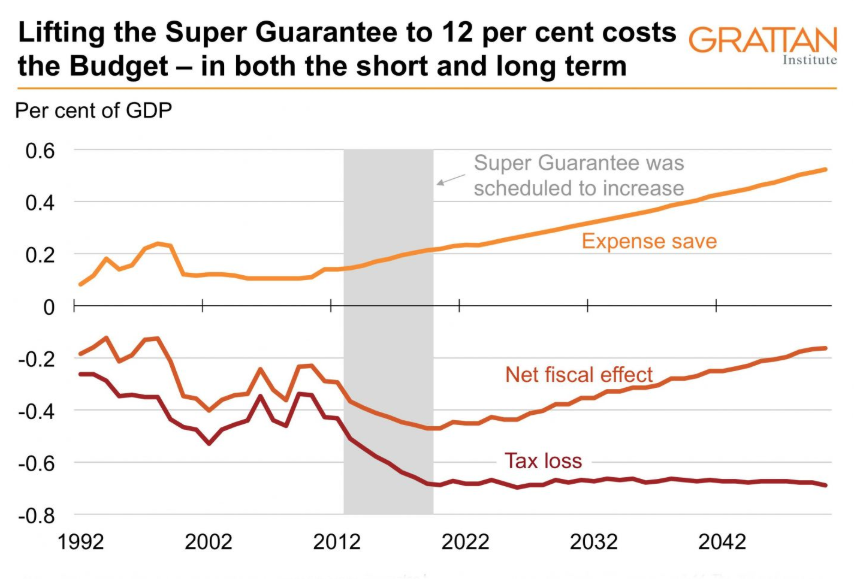

The Grattan Institute forecasts that lifting the SG to 12% would cost the federal budget an additional $2 billion a year in additional tax breaks and would also cost the budget more than it saves in Aged Pension costs over the long-run:

The purpose of superannuation is to save for the future and reduce future age-pension payments. In both the short and long term, though, superannuation costs the budget more than it saves, because the tax breaks cost the government more than the pension savings.

Actuarial firm Rice Warner said that lifting compulsory super contributions to 12% would not have much impact on the age pension for many years, and would save the budget only about 0.1% in lower age pension spending in the second half of this century.

In contrast, extra super tax breaks from higher compulsory super would cost an average of 0.22% of GDP “through this century”…

An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).

Advertisement

Clearly then, lifting the SG to 12% is unambiguously bad policy given it would: 1) lower take-home wages; and 2) worsen the long-tern sustainability of the federal budget.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.