US-China tensions escalate. According to Bloomberg reports, US President Trump has taken the view that COVID-19 originiated from a laboratory in Wuhan, and has threatened retaliation against China. His first threat was to block a large US fund from investing abroad according to global index weights, therefore putting a small dent in capital flows to China. So far, we have only seen a war of words, between US and Chinese officials, even before Trump’s recent statements. And Trump has stopped short of attributing blame to Chinese President Xi. Also, Chinese officials have not inflamed matters in their responses to Trump. But nonetheless, we have found recent developments quite troubling, as COVID-19 has taken on new geo-political dimensions.

Two sides to a trade war. The historical playbooks tell us that trade wars have both inflationary and deflationary aspects to them – but typically deflation occurs before inflation. On the deflationary side of things, we note that the US is a large net importer of goods and services from the rest of the world, meaning that on the flipside, it is also a large exporter of USDs to pay for them. To the extent that the rest of the world is dependent on USD funding, whether directly through USD foreign currency borrowing, or currency pegs, a US-led trade war causes a global USD funding squeeze, which in turn makes liquidity and funding conditions extremely challenging in the rest of the world, especially for emerging markets (EMs) dependent on USD funding. On the other hand, the longer term effects of trade wars can be potentially quite inflationary, as global supply chains are disrupted, and firms are incentivized to take back their production facilities from abroad at materially higher cost as competitive advantages from trade are either blocked or unwound. The balance between the deflationary and inflationary forces is a delicate one at any given point in time. But the longer trade wars go on, the more likely it is that the inflationary side will dominate.

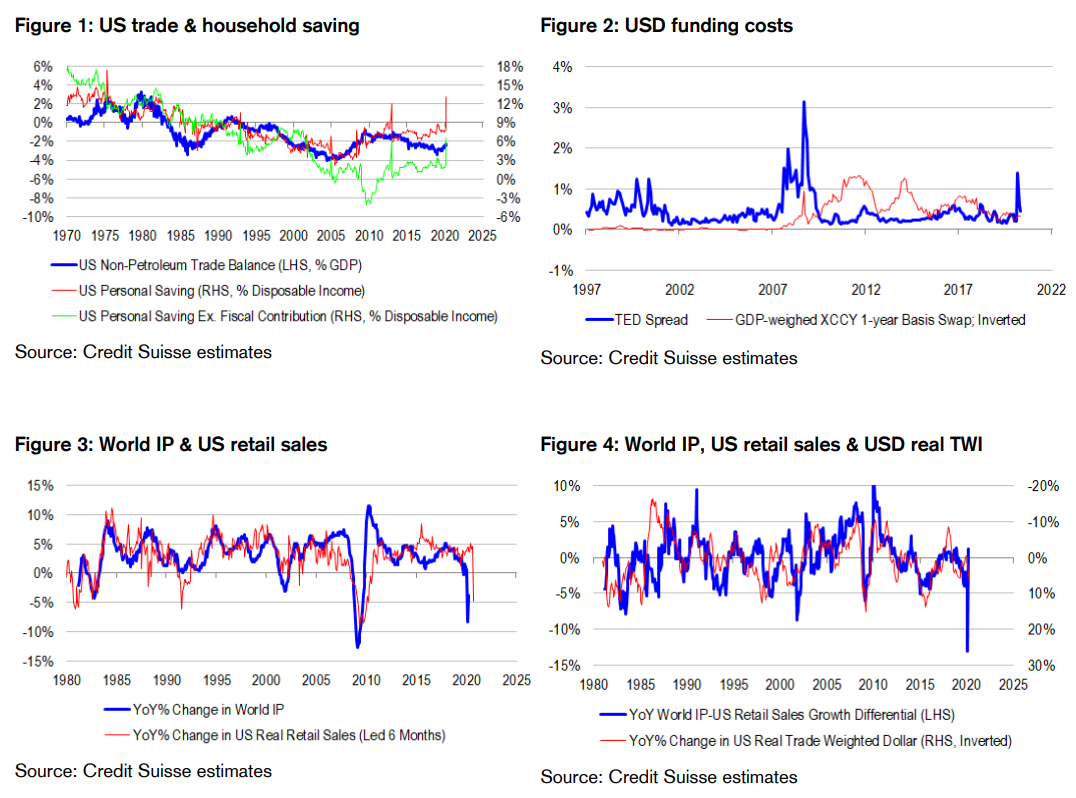

USD shortage comes back, especially for China. We see a global USD shortage re-emerging because a potential re-escalation of the trade war would exacerbate the effects of US consumer deleveraging on trade. From a flow of funds perspective, the US trade balance must equal the sum of US domestic public and private saving. The public sector is materially dis-saving at present as the government runs large scale fiscal stimulus. But the private sector is saving even faster than the government can dis-save, as evidenced by a sharp rise in the US household saving rate to 13.1% in April from 8%. Therefore, the trade deficit is becoming smaller, and the US is supplying less USDs to the broader world via trade. To be sure, the Fed is doing a lot to increase USD supply to the broader world and weaken the USD via foreign exchange (FX) swap lines and easy monetary policy. USD supply is caught in between conflicting trade and portfolio forces. But interestingly, the Fed has not set up any FX swap lines with China, which incidentally runs the biggest trade balance with the US of all the major economies and EMs. Therefore, the net balance of forces results in a material USD funding squeeze for China. Indeed, there are many commentators now talking about material CNY/USD devaluation to come.

COVID-19 already doing the disruption work of a trade war. COVID-19 is achieving what several years of trade wars could not. Perhaps more accurately, it is proving to be the straw that breaks the camel’s back. Surveys clearly tell us that world trade and industrial production (IP) are collapsing in response to shutdowns. New orders, order backlogs and commodity prices are falling sharply. The US consumer is weak, weighing on global demand and the USD is threatening to rise, consistent with tighter USD funding conditions abroad, reduced access to trade financing and shortening of global supply chains. In the circumstances, world IP could undershoot for a while, weighing on commodity prices from a physical demand-to-supply perspective. But surveys also clearly tell us that supplier deliver times are rising extremely sharply. Our proprietary pipeline inflation indicator, based on supplier deliver times, order backlogs and prices paid, is very close to neutral levels – a remarkable development all things considered. The pipeline indicator is a powerful anchor for inflation pricing in bonds. And currently neutral levels point to 10-year breakevens rising to around 1.8%, from roughly 1.1%. Should this materialize, the financial demand for inflation hedges like commodities should increase, notwithstanding what happens to physical demand.

An additional layer of uncertainty to deal with in asset allocation. At an asset allocation level, US-China escalation makes waves. It contributes to higher-than-normal equity market volatility (VIX), which in turn could cut short the breath-taking rally from late March. It has ambiguous effects on bonds, depending on the balance of inflationary and deflationary forces, and what the Fed chooses to do – but we dare say that at currently stretched valuations, the upside to bonds is very limited. Indeed, inflation uncertainty alone could prove a problem for the asset class. Uncertainty also makes commodity investing very complicated, as a potential return of USD strength is counterbalanced by the inflationary effects of supply chain disruption. In our view, gold is a clear winner, as it can rise with the USD, if uncertainty is high enough. Also, the Fed could always do more to weaken the USD.

But the fate of industrial commodities is clearly debatable. Finally we have concerns that uncertainty and foreign capital flight from China will either cause authorities to tighten capital controls, or shrink the pool of liquidity for Chinese residents to export abroad, weighing on their ability and appetite to purchase property abroad.

Factor investing signals unmoved, but stocks within buckets change a little. We remain short momentum (-38%), short value (-38%) and long quality (+24%). Dynamic factor weightings are little changed over the past month. But within each factor bucket, stock preferences are different, because of the fluid environment. Within the ASX 100, our factor preferences currently place large and uncrowded resources stocks, capex stocks and unloved quality exposures ahead of property exposures. Our long basket is slightly less resources heavy than it was before, and rightly so, because resources have outperformed eating into their alpha potential, and investors are already well aware of the recovery in China from a very low base.

Our short basket is less dominated by bank, healthcare and staple names, reflecting their underperformance in April. Heightened uncertainty is a negative for equities as an asset class, and could therefore be marginally supportive of defensive and quality exposures over cyclicals within the universe. However, from a factor investing perspective, high uncertainty undermines faith in trends, and the efficacy of momentum factors, which just so happen to be favouring defensives over cyclicals at present. High uncertainty is also a problem for value investing, because credit spreads are linked to uncertainty pricing. We worry that investors will start to lose faith in the omnipotence of the Fed, because fiscal policy is inflaming risks that the Fed cannot directly or easily control with its balance sheet management. Indeed, we are not just talking about US-China trade conflict, but also premature relaxation of shutdown restrictions and the potential for COVID-19 to mutate and spread again. Should uncertainty rise despite Fed quantitative easing, credit spreads could remain elevated or even rise, signalling de-leveraging risk. And de-leveraging undermines the efficacy of value factors, because asset prices drive fundamentals, rather than the other way around. Clearly Australian builders, property developers, banks and consumer stocks are subject to de-leveraging and housing risks. And interestingly, large cap resources stocks have very strong balance sheets, helping them to weather whatever storm comes from US-China tensions in a relative sense.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.