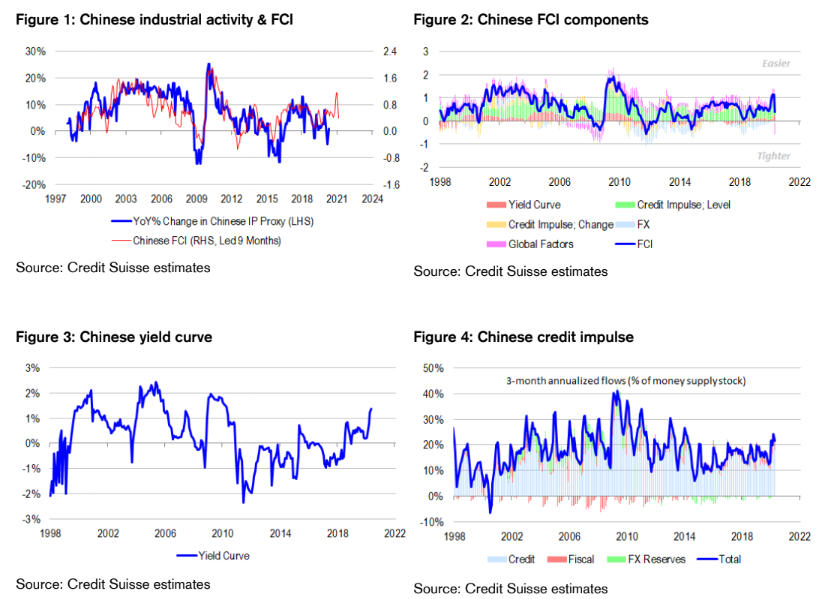

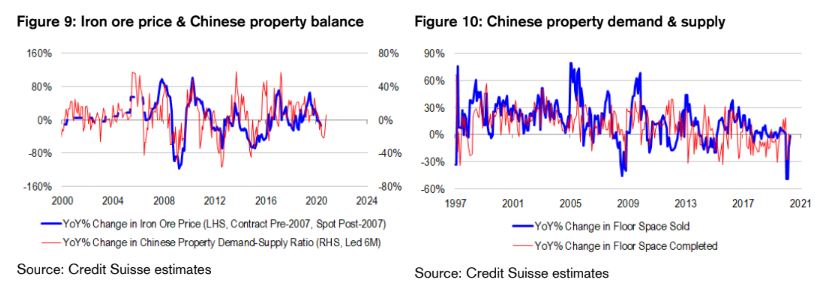

“Hard” indicators in China improving. Official headline data for China were mixed in April. Industrial production surprised to the upside, while retail sales and fixed asset investment surprised to the downside. But there was general improvement in the “hard” indicators we track for the sake of the Australian commodities outlook. Year-ended growth in electricity output picked up to 1.9% from -3%, while growth in exports picked up to 3.5% from -6.6%. Our unofficial industrial activity indicator, based on these indicators, as well as railway freight, has risen off the canvass. It is also noteworthy that property indicators have started to look healthier, with growth rates in floor space sold and floor space completed both turning less negative, and the balance of demand-to-supply growth tipping into positive territory. Credit easing measures have started to work.

Chinese yield curve steep, while credit impulse strong. Yield curves, defined as the spread between long-term bond yields and short-term interest rates, are powerful leading indicators of growth. In a world plagued with concerns about ineffective monetary policy at the zero bound and very flat or inverted real yield curves, it is interesting to note that China has one of the steepest yield curves in the world. Importantly, steepness is there despite concerns about capital outflows undermining the ability of the PBoC to control money market rates and liquidity in a pegged exchange rate regime. Transitioning from prices to quantities, we also note that the credit impulse in China—the growth rate of money supply defined from its sources—is very strong. Aggregate financing flows have increased sharply in recent months, overshadowing volatility in forex reserves, and developments on the fiscal front. The steep yield curve combined with strong credit impulse represent powerful easing contributions in our assessment of financial conditions.

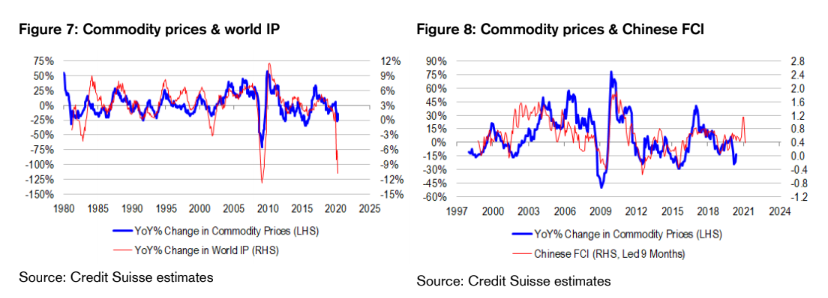

Global factors weighing on Chinese outlook. Domestic liquidity conditions for China are easy. But global factors are challenging. We note that the plunge in US real retail sales to roughly -20% in the year-to-April will weigh on export demand going forward. Moreover, renewal of trade tensions between the US and China threatens to dampen export prospects even more, and exacerbate capital flight from China to the detriment of liquidity in the system. However, we are encouraged by recent statements from Chinese authorities that they are willing to do more fiscal spending. Also, the Fed is doing its part to support USD funding for Chinese entities. The Fed is not launching a foreign exchange (FX) swap line with the PBoC, because the CNY is not considered a convertible currency. However, it is doing the next best thing via its Foreign and International Monetary Authority (FIMA) repo facility, which allows foreign central banks like the PBoC to swap their USDs held in the form of Treasuries for USD liquidity with the Fed, rather than go through the potentially disorderly markets. China has USDs—but in the form of Treasuries rather than cash. So the FIMA repo facility is an extremely useful option for the PBoC. That said, the facility does not completely alleviate all funding pressures for China from capital flight.

Chinese growth “hanging in”. Our proprietary Chinese financial conditions index (FCI) takes into account domestic factors like the yield curve and credit impulse. It also takes into account FX and global factors such as USD funding conditions and US retail sales. It is historically a powerful leading indicator of Chinese industrial activity growth as we prefer to measure it. And right now, it points to slightly easy conditions and better growth prospects from a relatively low base. To be sure, recent shocks from US developments are driving the FCI lower, and do threaten to derail recovery longer-term, especially if trade war escalation gets out of hand. However, for now, the FCI is “hanging in” there. There are upside risks to consider too, if shutdown restrictions globally are relaxed, and the US consumer resumes more normal spending activity. Indeed, high frequency indicators such as credit card spending suggest that the worst for US retail sales may have just passed behind us.

Still overweight resources. Resources stocks are outperforming the ASX 200 since the onset of the crisis. We are very tempted to neutralise our overweight on the sector because of strong outperformance. But we think there is more outperformance to come, notwithstanding deterioration in the US economy and US-China relations. The outlook is clearly fluid, but we think there is enough easiness in Chinese financial conditions and upside to the global cycle from shutdown relaxations to weather minor storms for a bit longer, especially in a relative sense for resources companies. Interestingly, commodity prices are materially overshooting world industrial production (IP) growth consistent with past episodes of deep contraction…Commodity price dynamics clearly become a bit non-linear around the most volatile times in the cycle. We think these non-linearities are related to supply side destruction, scarcity and inflation uncertainties therein. And in our view, they afford us some protection against some of the growth shocks that could occur going forward.

A few points:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.