Mixed April NAB business survey: The NAB survey for April revealed an even sharper decline in business conditions, with the component sum index falling to -34 from a downwardly revised -22. However, the more forward looking, “pure” confidence measure, improved to -46 from an upwardly revised -65, as companies adjusted to the shutdown period and started to see some daylight. The confidence-conditions spread, a pure sentiment indicator, and a powerful leading indicator of the slope of the real yield curve, turned less negative, consistent with steepening of the curve from deep inversion territory.

Business spending intentions plunge. There are many interesting elements to the NAB business survey which we use in our modelling. Among them are firms’ capex and hiring intentions – effectively two sides of the same coin of business spending. Capex intentions deteriorated at an even sharper pace in April to -33 from -24, while hiring intentions plunged to -35 from -20. Both indices have fallen to all time historical lows, consistent with other available data points such as ANZ and SEEK job advertisements.

Core domestic demand still in the gutter. Taking into account capex intentions in the NAB business survey, as well as other available partials such as credit, retail sales, building approvals, consumer sentiment and the depth of the infrastructure spending pipeline, we “now-cast” ongoing contraction in domestic demand. Indeed, the only data points holding up our activity tracker are retail sales and credit growth, which are heavily distorted by hoarding behaviour and credit line drawdowns during the early stages of the shutdown. Ultimately, these distortions are likely to wash out, consistent with an even sharper pace of decline in domestic demand than our tracker is suggesting currently.

Employment plunging. Our proprietary core domestic demand tracker is a key component of our leading labour market indicator, as well as NAB business survey hiring intentions and ANZ job advertisements. The weighted average of these leading indicators is now pointing to contraction in aggregate hours worked of 7-8%, consistent with what ABS weekly payrolls data are suggesting.

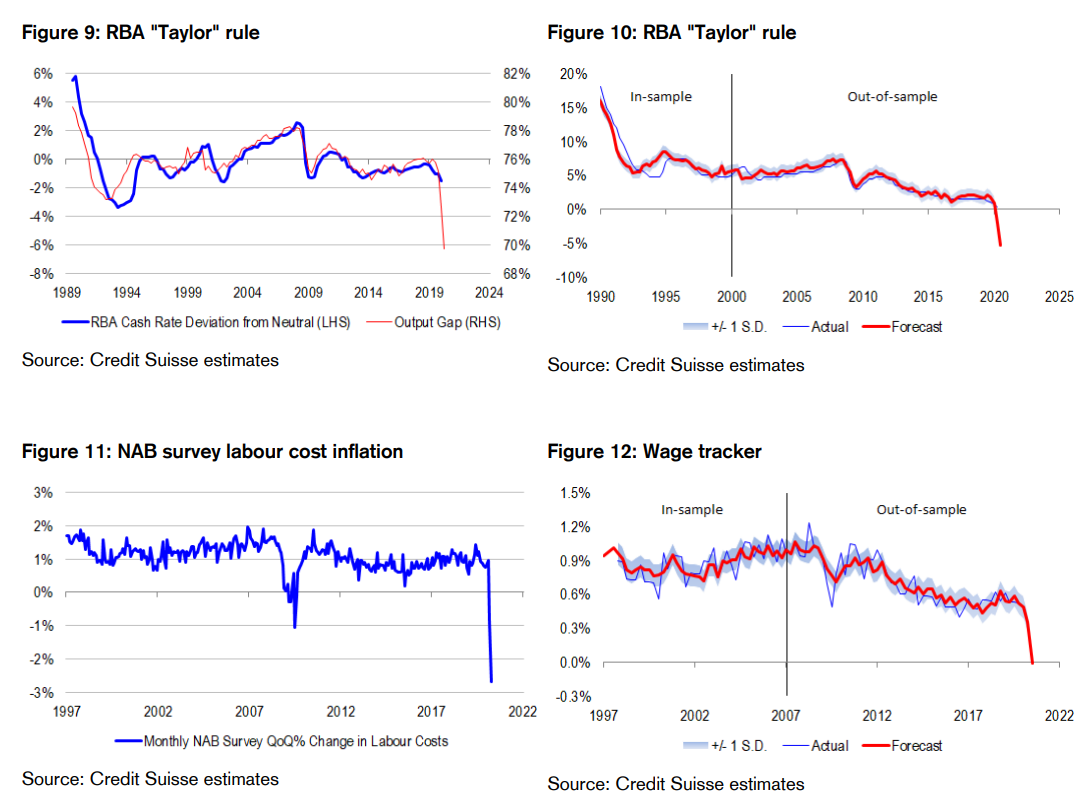

Historically wide output gap. Our proprietary real-time output gap is based on NAB business survey capacity utilization and male full-time employment as a share of the “active” labour force. The NAB survey reveals a decline in capacity utilization to a new historical low of 72% in April from 75% in March, and 81% in February. We do not yet have April labour market data, but if Consensus forecasts and our leading indicators are anything to go by, we will likely see sharp deterioration on this front too. Our real-time output gap will likely reach new wide levels. This matters for the RBA, because historically, the Bank sets the cash rate in accordance with the long-term neutral rate, with adjustments for the size of the output gap. We estimate that the equilibrium cash rate is now below -5% – an impossible level for the Bank to reach. Moreover, we doubt that extraordinary stimulus from elsewhere in the system (i.e. fiscal deficit spending and quantitative easing) is achieving a commensurate reduction in the “shadow” cash rate. Therefore, the RBA will likely struggle to behave in a sufficiently predictable way to keep risk premia in bonds down as it has in the past. To be sure, it has forward guidance at its disposal, but uncertainty is not just in rates now, but in the fundamental drivers of activity and CPI …

Labour costs falling? In the US, labour market conditions are deteriorating to the point that we might expect to see wage cuts. However, the US data reveal that the average American is not taking pay cuts, at least not just yet. We suspect the same is true of the average Australian too. With this in mind, it is interesting to note that the NAB business survey points to a quarterly decline in labour costs of 2.7%. The NAB labour cost inflation measure, combined with Enterprise Bargaining Agreement (EBA) wage claims, and our preferred measure of labour market slack, form the backbone of our proprietary wage tracker, which leads actual wage inflation outcomes by several months. Generously extrapolating EBA wage inflation at its 3Q 2019 pace because of the Fair Work Commission deferral decision, assuming Consensus numbers for the April labour market report, and applying the latest NAB survey data, we arrive at a slightly negative “now-cast” for the wage cost index. The question is whether or not Australians will indeed take pay cuts to preserve their jobs, or get new jobs in such a weak macro environment. And if the US experience is any guide, we suspect not. Therefore, inflation dynamics are about to become a whole lot more unstable relative to historical norms.

Bond yields could decouple from deteriorating macro data. We have longer-term concerns about supply side destruction from permanent business closures causing inflation risk. But clearly, we are not at this stage yet, given the plunge in capacity utilisation to new historically low levels. Clearly, small businesses struggling with their “will to live” are still holding on, aided by government stimulus. But how long they will hang in for is debatable, especially if we enter rolling shutdowns. And in the meantime, we are concerned about policy unpredictability and unusual wage inflation dynamics feeding into risk premia in bonds. Indeed, should the yield curve steepen because of these factors, investors may become concerned that higher bond yields are not necessarily a sign of good or bad growth, but merely risk. But for investors following a more conventional playbook, there seems to be enough optimism among businesses that we will not enter rolling shutdowns to also position for curve steepening. However, we have our doubts that the curve will steepen to the point of meaningfully escaping inversion territory, because the NAB business confidence-conditions spread is not improving dramatically, there are renewed concerns about USD liquidity tightening from trade wars, and we are at the effective zero bound for rates.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.