NSW government considering abolishing stamp duty. Stamp duty is a transaction, or “Tobin” tax on property paid by buyers. It is the primary source of state government revenue. It is viewed by many commentators to be an inefficient tax, breeding incentives for state governments to prop up property prices to prop up revenues. Recently, NSW Treasurer Perrottet has raised the possibility of reforming property taxes, with a view to abolishing stamp duty. We think that discussion has been prompted by the sharp deterioration in the macro environment, and has also been enabled by RBA quantitative easing (QE) in the semi-government bond complex. After all, state governments are funding constrained, with natural biases towards austerity and status quo tax arrangements, until someone comes along to make funding risk free, like the RBA through QE. But QE is an emergency measure. States cannot presume upon the RBA being the buyer of last resort indefinitely, without wholesale changes to the plumbing of the system, such as a return to Exchange Settlement Account (ESA) privileges with the Bank. Therefore, long-term, the NSW government will need to replace stamp duty with something different, such as land tax.

Abolition of stamp duty would improve housing affordability. In NSW, the average rate of stamp duty is around 4% of a property’s value. Abolition of the tax would increase housing affordability by 4% or more, if we also account for leverage and increased borrowing capacity.

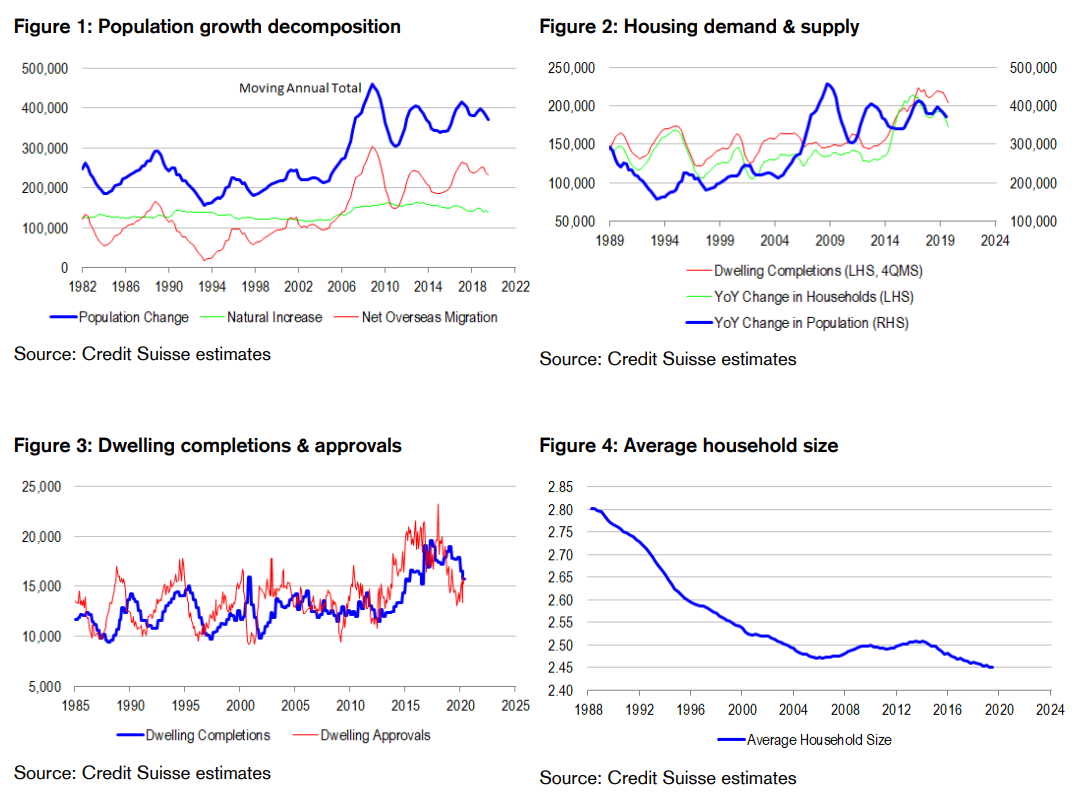

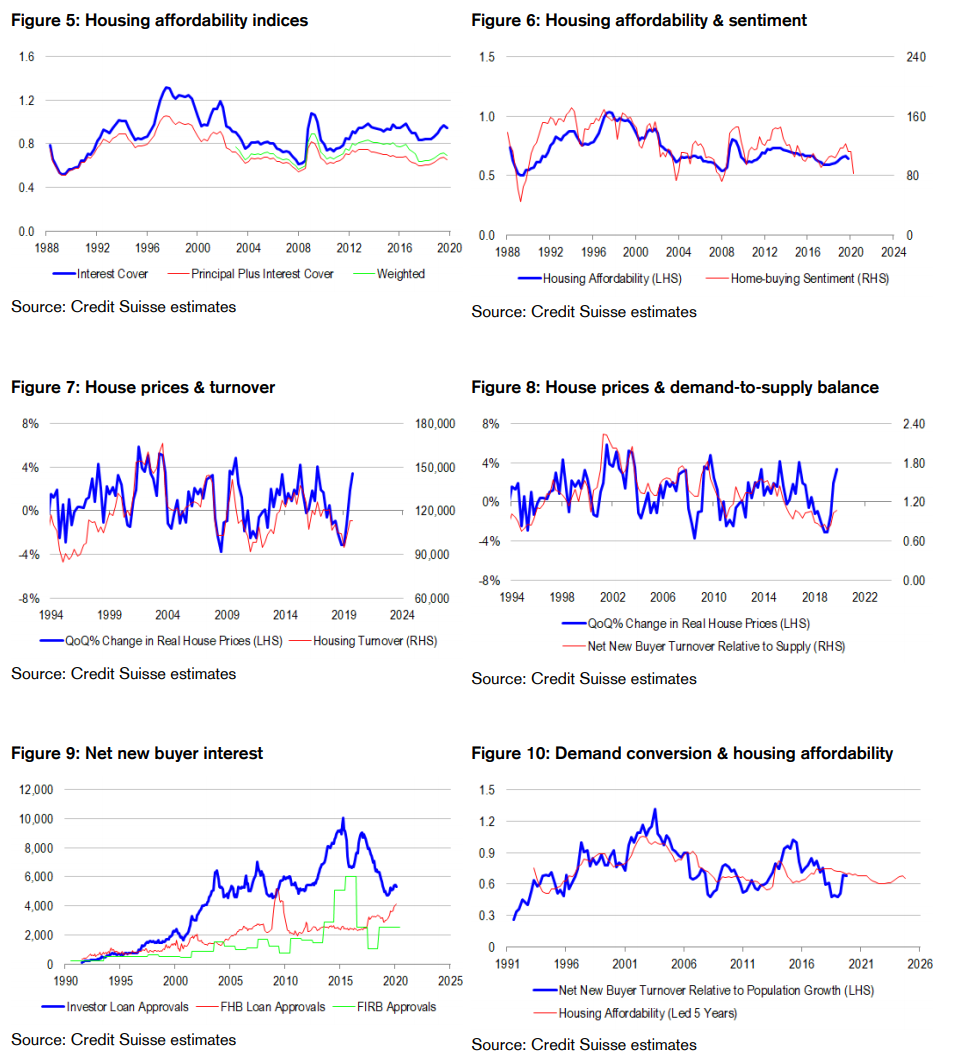

History says turnover key to price gains, making Tobin tax reduction attractive, but … Over the past few decades, we see an extremely strong and positive correlation between house price inflation and housing turnover. On the basis of this correlation alone, one could easily arrive at the conclusion that abolition of stamp duty would increase turnover and prices significantly by lowering the cost of transacting. However, historical correlations mask different moving parts to the house price equation. In the first place, supply matters as well as demand. We also need to account for new supply from dwelling completions as well as existing supply from foreclosures in any house price model. Secondly, not all buyers are created equal. Home movers do not influence the housing demand-to-supply balance in that they sell a home to buy a home. The real net new buyers are first home buyers, investors and foreigners. What should really matter for house prices is the turnover of net new buyers relative to new and existing supply. And the data support this fundamental view. Our demand-to-supply proxy is even more highly correlated with house price inflation than housing turnover alone, looking all the way back to the early 1990s. To be sure, abolition of stamp duty will likely increase participation in the market from first home buyers, investors and foreigners by altering housing affordability and incentives to “buy and hold” property. However, our point is that the transmission mechanism is more sophisticated than merely boosting turnover.

Housing affordability a powerful driver of demand conversion, but … Most economists model house prices by using a fundamental estimate of household formation based on demographics, and subsequently comparing this to supply. There are merits to this approach, provided we can accurately model average household size without resorting to supply side variables and circular reasoning therein. Suffice to say, we are not so confident. But the good news is that if we can find a reliable way of converting population growth into housing turnover via a known and predictable conversion ratio, we can construct independent demand and supply indicators, which will be able to explain and predict house price inflation. As it turns out, there is a one-for-one relationship between the conversion ratio of net new buyer housing turnover to population growth, and housing affordability. We use housing finance and Foreign Investment Review Board (FIRB) data to quantify net new buying interest. And we use a principal plus interest cover measure of housing affordability assuming the standard variable mortgage rate at any given point in time as well as a 25 year loan life. On this basis, a 4%+ increase in housing affordability should increase the conversion ratio by 4% or more. But there is a catch—history says that it takes a very long time for affordability changes to feed through permanently into conversion rates. Indeed, the lead time could by up to 5 years. And in the interim, there are some challenging affordability dynamics to navigate.

Population growth slowing sharply and housing oversupply ratcheting up. In 2019, the population grew by roughly 1.5%. Of this growth, 0.6% was in the form of natural increase, while 0.9% came from net migration. With COVID-19 border restrictions in place, the risk is that population growth slows sharply towards the rate of natural increase. The longer borders remain closed the greater the skew of population growth towards 0.6%. While we have no particular insight into when shutdown restrictions will be relaxed, we do suspect that even when domestic restrictions are unwound, that border closures will remain in place for a considerable period of time longer so as to minimize risks from reinfection and virus mutation from abroad. Prime Minister Morrison has suggested that migration could fall by 85% in FY21, consistent with annualized population growth halving to 0.75%. Household formation—that is, housing demand before accounting for demolitions—could easily halve. Assuming the current average household size of 2.45 (circular, yes we know), a slowing in population growth to 175K per annum from roughly 370K in 2019, would cause household formation to drop to 71K from 151K. Accounting for 20-25K per annum worth of replacement demand, this would imply underlying housing demand of 91-96K, well short of the current level of dwelling completions of around 190K as well as the annualized level of building approvals of 180K.

Boost to affordability from stamp duty abolition small compared with halving of population growth. Using our preferred framework for modelling house prices based on net new buyer turnover relative to supply, we arrive at a very similar oversupply scenario to the “fundamental” picture. If the best that stamp duty abolition can achieve is a 4%+ increase in housing affordability, with delayed effectiveness, this stimulus would pale in comparison with the halving of population growth being projected by officials. Because the relationship between conversion and housing affordability is neatly one-for-one, with a long delay, net new buyer turnover would still decline to the tune of 46%. Our demand-to-supply measure would fall to its lowest level since the early 1990s recession, consistent with sharp declines in real house prices.

To make stamp duty abolition work, regime change would be required to re-shape expectations. All of our analysis assumes that historical relationships hold up. Policy makers could always throw a spanner in the works by dramatically changing the rules of the game. And at first glance, abolition of stamp duty looks like a dramatic rule change with potentially non-linear consequences. But credibility is an issue if the RBA does not commit to being the buyer of last resort of semi-government debt in the long term. In this scenario, state government funding constraints would inevitably return, forcing officials to substitute stamp duty for a regime based on land taxes. In turn, this would create a “Ricardian equivalence” problem for potential borrowers today that would feed back into their present behaviour. In other words, without a blanket promise to permanently and drastically cut the sum total of property taxes, whatever their form, households will merely look though announcements today and not change their behaviour. The 5-year lead time from housing affordability to demand conversion would continue to hold, and the halving of population growth from COVID-19 restrictions would drag net new buyer demand significantly lower.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.