Robert Lechte, a welfare-state advocate living in Melbourne, believes that Australia’s superannuation system “enshrines inequality”:

Like other market-based schemes, superannuation has reinforced and accelerated existing inequalities. Because super is primarily funded by employer contributions, it is self-evidently terrible for the unemployed or those out of paid work due to disability, sickness, or caregiving. They earn a 9.5 percent contribution on zero — namely, zero. By contrast, professionals, managers and other high-income employees earn 9.5 percent super on six-figure salaries — earning increased interest.

Lower-income groups are also at a disadvantage…

It’s commonly asserted that a higher contribution percentage will simply fix things, but super contributions cannot fix income inequality because super balances are themselves nothing more than income, determined by the labor market, forcibly saved.

Similar sentiments were echoed by The Australia Institute’s (TAI) chief economist, Richard Denniss:

According to research from my Australia Institute colleague Matt Grudnoff, 60 per cent of superannuation tax concessions go to the top 20 per cent of households, with just 11 per cent going to the bottom half of all Australian households…

According to Treasury, when you compare the age pension and superannuation tax concessions, taxpayers spend at least twice as much supporting the retirement of someone in the top 1 per cent of income earners as they spend on someone receiving the age pension…

The people who invented our compulsory superannuation system, and the tax concessions that accompany it, didn’t set out to make a system that takes the disparities in working-life incomes and magnifies them in retirement.

Since the size of one’s superannuation nest egg is a function of how long one works and how much they earn, and because the 15% flat tax on superannuation contributions and earnings provides the most benefits to those on higher marginal tax rates, superannuation drives inequality.

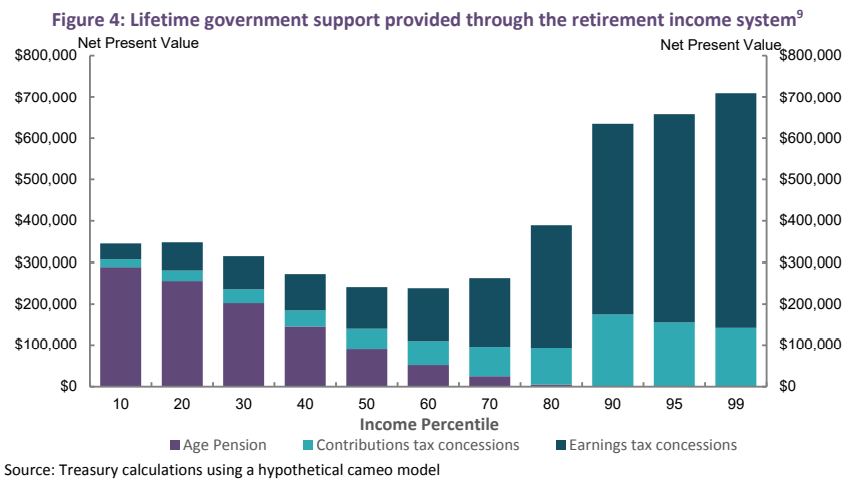

Anybody disputing these claims only needs to examine the below chart from the Australian Treasury, which shows the lifetime taxpayer support provided via the retirement system:

Clearly, higher income earners receive a disproportionate share of superannuation concessions.

For instance, the top 1% of earners are projected by the Treasury to receive more than $700,000 in superannuation concessions over their working lives, which dwarfs the $50,000 of concessions received by the bottom 10% of income earners.

Accordingly, Australia’s compulsory superannuation system is actually enshrining inequality by concentrating asset ownership among the wealthy.

For these reasons, Australia’s superannuation system is really more of a tax avoidance scheme for the rich than a genuine retirement pillar.

Therefore, the absolute last thing the federal government should do is go ahead with the legislated lift in the superannuation guarantee to 12%, given this would worsen inequality.