Chief economist of The Australia Institute, Richard Denniss, is the latest commentator to expose the gross inequity of Australia’s compulsory superannuation system:

This year, the government will spend more than $41 billion on tax concessions for superannuation with the stated purpose of helping people save for their retirement. But the way the rules are designed give the vast majority of that money to people who will already retire comfortably, while providing next to nothing to those with the lowest incomes and the lowest super balances.

According to research from my Australia Institute colleague Matt Grudnoff, 60 per cent of superannuation tax concessions go to the top 20 per cent of households, with just 11 per cent going to the bottom half of all Australian households…

According to Treasury, when you compare the age pension and superannuation tax concessions, taxpayers spend at least twice as much supporting the retirement of someone in the top 1 per cent of income earners as they spend on someone receiving the age pension…

Superannuation tax concessions aren’t just enormous and unfair, though: they are also growing – at about 8.5 per cent a year, twice the rate of growth for the age pension. And while you often hear conservative politicians and business leaders bemoaning the “unsustainable” growth in welfare spending, it’s rare to hear them expressing concern about the rapidly growing cost of the tax benefits we give to the wealthiest Australians…

The people who invented our compulsory superannuation system, and the tax concessions that accompany it, didn’t set out to make a system that takes the disparities in working-life incomes and magnifies them in retirement. Regardless of their intentions, however, that is precisely what they have made. And there are clearly no regrets…

But while successive governments have assured us we “can’t afford” to increase unemployment benefits or the age pension, we currently spend more than $24 billion a year boosting the retirement incomes of the wealthiest 20 per cent of the population…

It gets worse.

One of the biggest justifications for putting 9.5 per cent of our wage into superannuation, and for spending $41 billion a year on tax concessions for that super, is that it “takes pressure off the age pension system”. The only problem with this argument is that it’s not true. Not even close.

The people who get the most taxpayer support for their retirement savings are those who are already so wealthy that they were never going to be eligible for the age pension – because the pension is “asset-tested”…

Even though we spend a combined $90 billion a year on the age pension and tax concessions, and a further $30 billion a year on superannuation fees, poverty among older Australians is more common in Australia, particularly among women, than in most OECD countries.

…the superannuation industry is so relaxed and confident that rather than wasting time defending the obscenity of the existing inequities, it is running ads demanding we all put more money into their broken system.

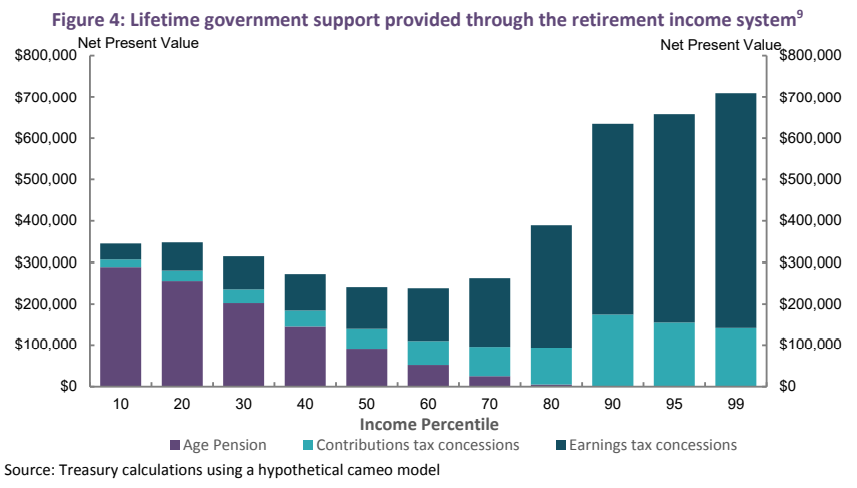

Well said. Anybody disputing Richard Denniss’ claims only need to examine the below chart from the Australian Treasury showing the lifetime taxpayer support provided through Australia’s retirement system:

As you can see, superannuation concessions are massively skewed towards high income earners. For example, the top 1% of income earners will receive over $700,000 in taxpayer contributions to their personal superannuation account over their working lives, whereas those in the bottom 10% of income earners will receive less than $50,000.

Therefore, Australia’s compulsory superannuation system is helping to concentrate asset ownership among the wealthy and exacerbating inequality.

Instead of lifting the superannuation guarantee from 9.5% to 12%, in turn exacerbating these inequalities and increasing the net cost to the federal budget, superannuation concessions should be made progressive so that they go to where they are needed (i.e. lower and middle income earners) and genuinely relieve pressure on the Aged Pension.