DXY was weak last night as EUR chases the fiscal package:

Australian dollar was weak anyway:

EMs were mixed:

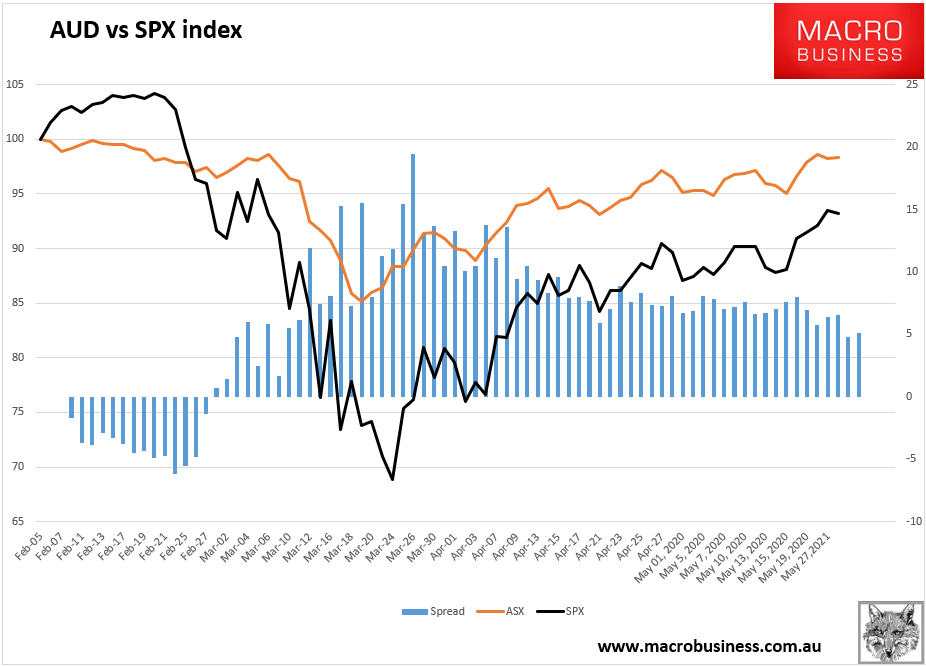

AUD/SPX correlation had an up day but is trending lower:

Gold was firm:

Oil too:

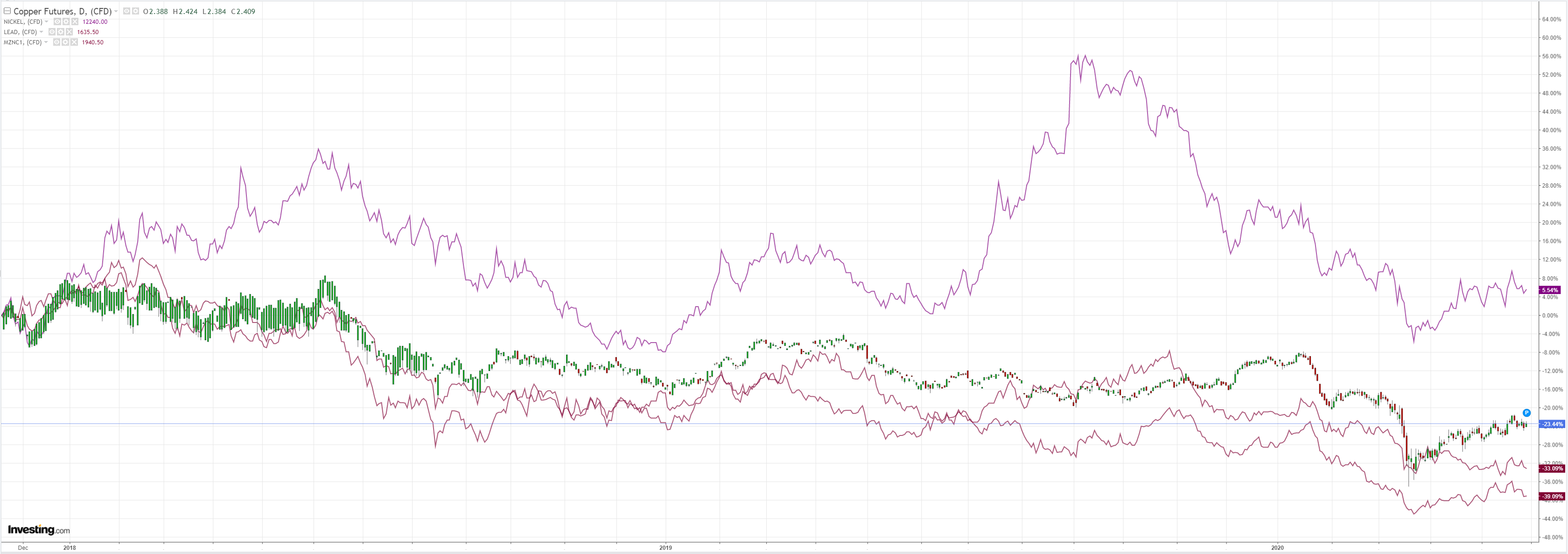

Dirt is crushed:

Except the red magic dirt. Anyone with that is flying:

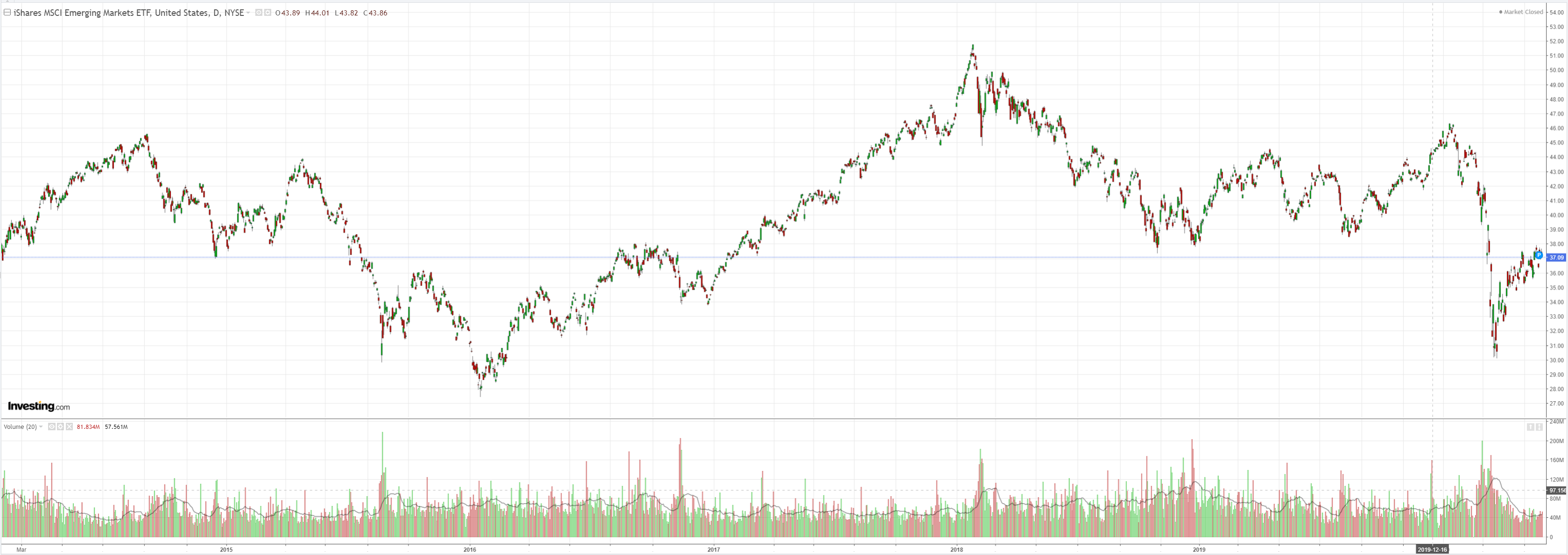

EM stocks are stalled:

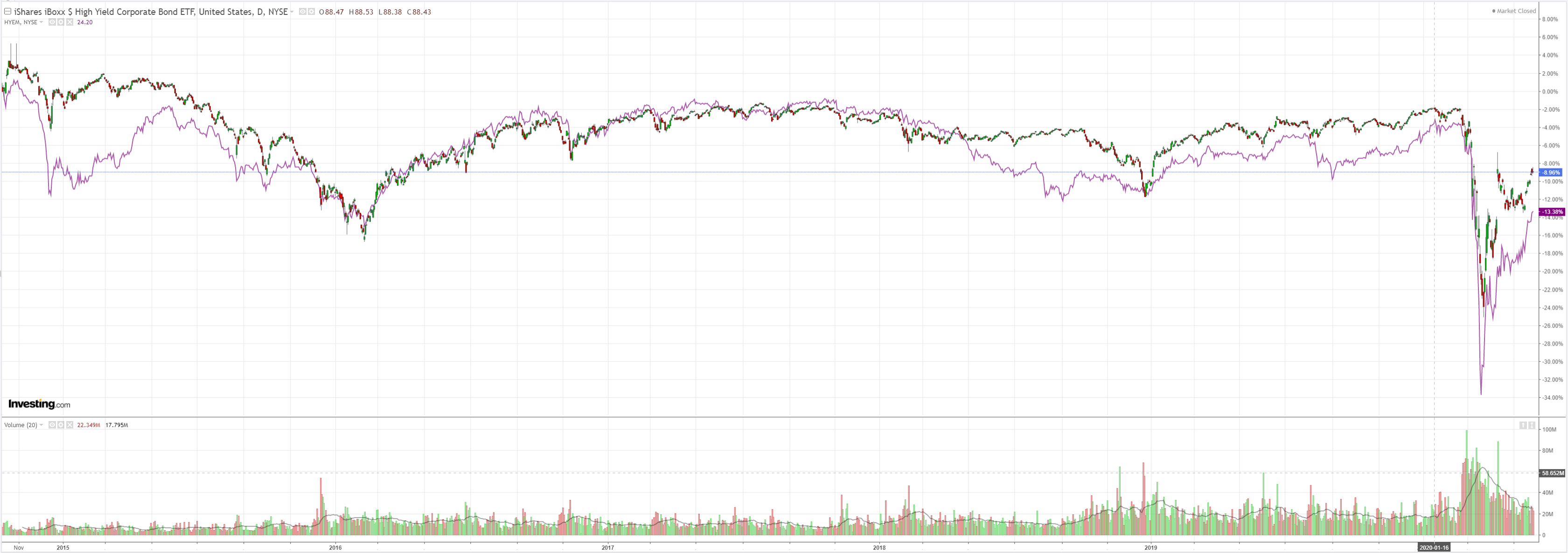

Junk is euphoric:

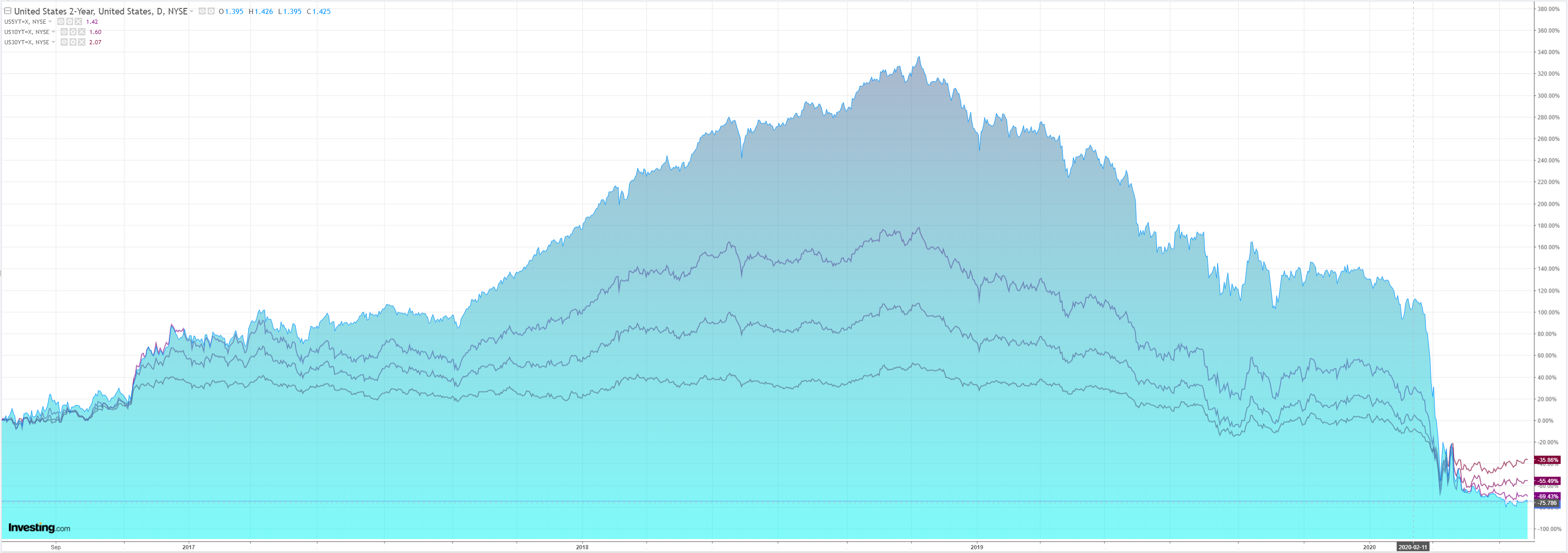

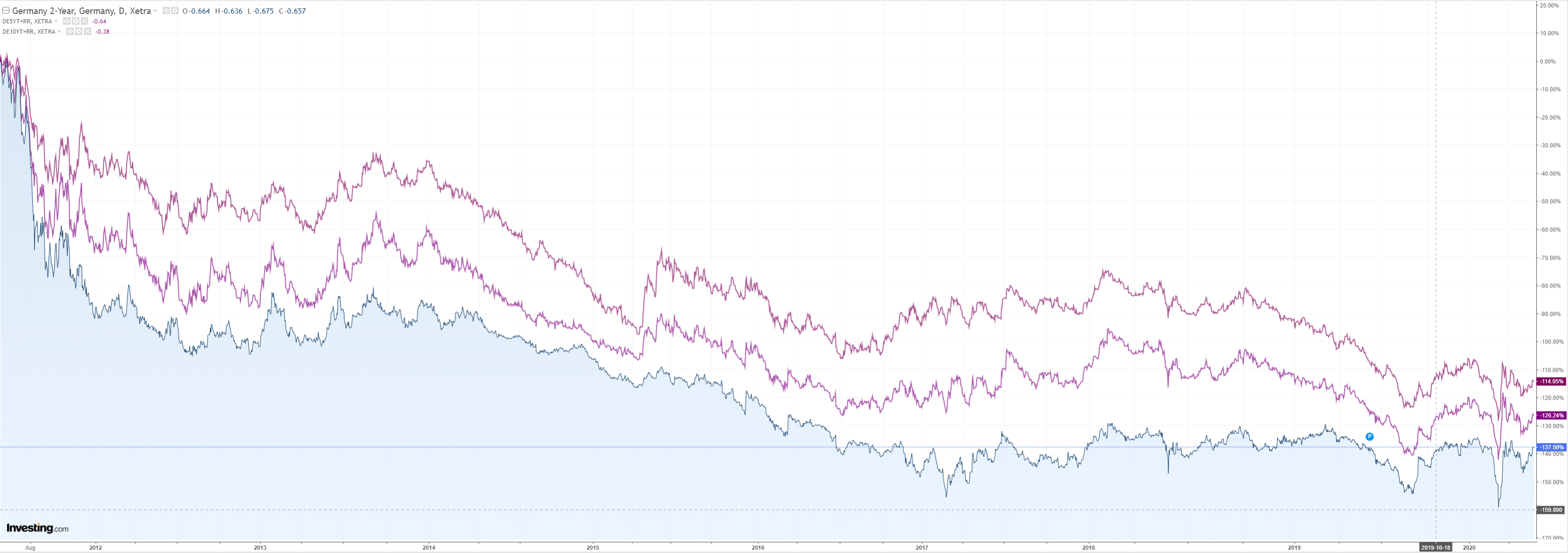

Bonds were bid:

Stocks stalled:

Westpac has the wrap:

Event Wrap

US weekly jobless claims rose in line with expectations at 2.1m. However, continuing claims fell to 21m from 25m (estimates were close to 26m), indicating the worst in the labour market may have passed. April durable goods orders did not fall as much as expected, the headline measure down 17.2%m/m (vs est. -19.0%m/m), and the ex-transport measure down 7.4%m/m (vs est. -15%m/m). The second take on Q1 GDP was slightly weaker (annualised -5.0%, vs est. -4.8%), although personal consumption fell 6.8% annualised (vs the expected -7.5%). Pending home sales fell 21.8%m/m in April (vs est. -17%m/m).

Kansas Fed’s manufacturing survey was less weak than expected at -19 (est. -22, prior -20), the outlook rising to -2 (prior -8).German May (provisional) CPI was as expected at -0.1%m/m and +0.6% y/y, with harmonised slightly less weak at 0.0% m/m and +0.5%y/y (est. -0.1%m/m, +0.4%y/y).

Eurozone May economic confidence was slightly below estimates at 67.5 (est. 70.6, prior revised to 64.9 from 67.0), with services notably softer at -43.6 (est.-27.9), though industrial confidence at -27.5 (est. -26.5) was close to expectations.Event Outlook

Australia: April private sector credit rose by 1.1% in March as firms drew down on existing lines of credit to boost liquidity ahead of the looming cash flow squeeze. This dynamic should extend into April, and Westpac is looking for a print of 0.6%. The ABS will also release the “Household Impacts of COVID-19 Survey” for 12-15 May.

New Zealand: May ANZ consumer confidence will be supported by the easing of COVID-19 restrictions.

Euro Area: M3 money supply should continue to accelerate as easing takes effect (market f/c 8.2%yr). The May CPI is expected to slip into deflation with a print of -0.1%, dragging annual price growth to 0.1%yr.

US: April wholesale inventories will continue to wind down as businesses brace for the demand shock. Personal income (market f/c -6.0%) and personal spending (market f/c -12.8%) will be hit hard in April, with further weakness ahead as job losses dampen activity. Having slipped into negative territory in March, the core PCE deflator is set for another weak print of -0.3%. To round out the day, the May Chicago PMI is poised for a marginal recovery (market f/c 40.0), and Fed Chair Powell will take part in a moderated virtual discussion (01:00 AEST).

In this bizarrely accelerated new normal, we’ve now had the boom, the bust, the stimulus, the recovery, the rotation and, if it remains true to form, next will be the bond back-up as recovery takes hold. That’s three years’ worth of market action in three months.

But is it real? Of course not. It is the great fakeflation, an entity of suspended animation in which capitalism has been bundled into a cryogenic chamber, so that markets can pretend there is a cycle. We all fear the moment that the door is opened and the stink of putrid reality gushes into our noses.

But my thoughts today wander over to the possibility that that will never happen. I have not been convinced by arguments that the Government can hold asset prices up just by choosing to. But there is another way to look at this which is perhaps more credible. Phil Lowe gave us a hint about it yesterday. Via News:

Australia’s Reserve Bank Governor Phil Lowe has warned ending the $1500 JobKeeper’s wage subsidy too early would be a “mistake” and it may need to be extended beyond September.

Breaking with the Prime Minister’s rhetoric that the scheme needs to be phased out as soon as possible, the RBA chief has warned the premature withdrawal of stimulus could damage the economy.

But he’s proposed that any extension would likely to be more targeted, for example for the tourism industry hit by international border closures, an option the Prime Minister has previously flagged.

What an absurd notion. Exactly how long are these jobs that the Government is paying people not to do still jobs? Judging by Captain Lowe, forever!

And that may be the rub. I have long argued against crashnics that see the end of fiat currency that, rather, the next evolution in our economic system is to principles and policies associated with Modern Monetary Theory (MMT). Emergency stimulus measures are almost never withdrawn so what we may instead have upon us now is the MMT era. Like most of these things, it’s not been born clean, with forethought and planning, but in crisis, mutilated by panic and interests. Yet it may still be the new normal.

What will be the outcome of this be for currencies? Traditionally it was a mix of internal, external and relative measures that determined value. In the MMT environment, if that is what it is, the answer will probably be determined by inflation. Those nations that “stimulate”, that is pay the most people to do nothing, will find themselves with greater aggregate demand, inflation and higher currencies. Those that don’t pay everyone to do nothing, with inhibited “stimulus”, higher unemployment and deflation will see lower currencies.

That means those with solid external accounts will be rewarded most with lower currencies, intensifying their imbalances. While the fiscally and monetarily profligate will be punished with higher, chasing inflation, intensifying theirs as well.

It’s the opposite of what should happen in theory but, hey, this is suspended capitalism now.