When it comes to self-entitlement, you would be hard pressed beating Australia’s superannuation industry.

Industry superannuation funds were first to attack the Morrison Government’s decision to allow financially strapped Australians to access $20,000 of their own superannuation savings early, which continues to this day:

“If it’s seen as a regular opportunity to dip into [super] every time there’s a major national problem, that would really ruin the entire, great superannuation system that we have in Australia,” said Gerard Noonan, the chairman of industry fund Media Super.

Non industry funds like Future Super have also attacked the early release scheme:

Since applications opened last week, almost half a million Australians have been approved to withdraw a total of $3.8 billion from their superannuation savings, in lieu of other avenues for support.

The decision many people are being forced to make is this: choose between you, now, or you in the future. It’s not a real choice. When you need to put food on the table, there’s no getting past the fact that you can’t eat compound interest.

The risk of this policy is that we create a second class of citizens in Australia. A group of people who will retire with collectively billions of dollars less than their peers, because we didn’t protect their futures in this time of need… the early access super policy is treating the superannuation of those individuals suffering from COVID-19 as a national relief fund.

Let’s put some facts on the table.

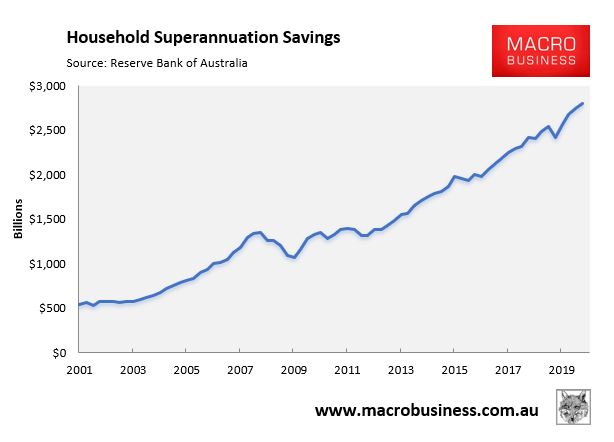

First, the Australian Treasury forecasts that up to $27 billion would be withdrawn from superannuation balances. This is tiny when viewed against the $2.8 trillion of total superannuation savings as at December 2019 (latest available data):

This money belongs to members and they should be allowed to access it in this time of need.

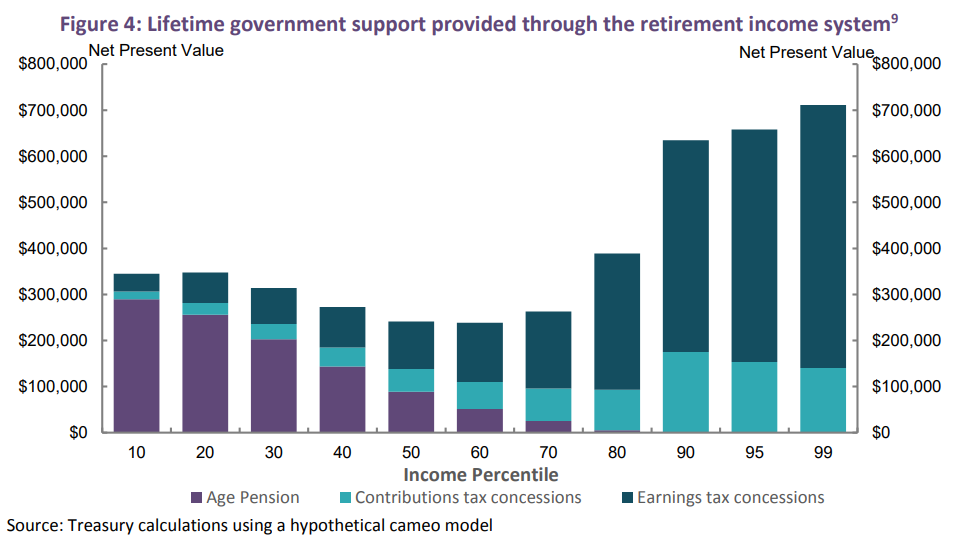

Second, the claim that the early release scheme would “create a second class of citizens in Australia” that “will retire with collectively billions of dollars less than their peers” is laughable when one considers how superannuation tax concessions are distributed.

Superannuation concessions cost the Federal Budget an obscene $43 billion a year. They are also very poorly targeted, with high income earners receiving the overwhelming majority of concessions, as illustrated by the below chart from the Australian Treasury:

Clearly, the compulsory superannuation system is already worsening income inequality. Moreover, the poor targeting of concessions towards high income earners means that superannuation costs the Federal Budget far more than it saves in Aged Pension costs, as confirmed by the Henry Tax Review, the Grattan Institute and actuaries Rice Warner.

The motivations of the superannuation industry are obvious. They want to protect the compulsory system at a minimum and preferably succeed in having the superannuation guarantee lifted from the current 9.5% to 12%.

This would ensure an ever-growing base of funds under management to which superannuation funds could skim management fees from. It has absolutely nothing to do with efficiency or equity, both of which is damaged by the compulsory superannuation system.

This gross inefficiency is evidenced by the fact that the typical Australian spends twice as much each year on superannuation management fees than they do on electricity. However, because these fees are hidden from view, few people realise they are being robbed blind.

The superannuation industry wants to fatten this gravy train, which explains why it continually deflects attention away from the truth that superannuation is a net drain on taxpayers, robs workers of disposable income, and worsens inequality.