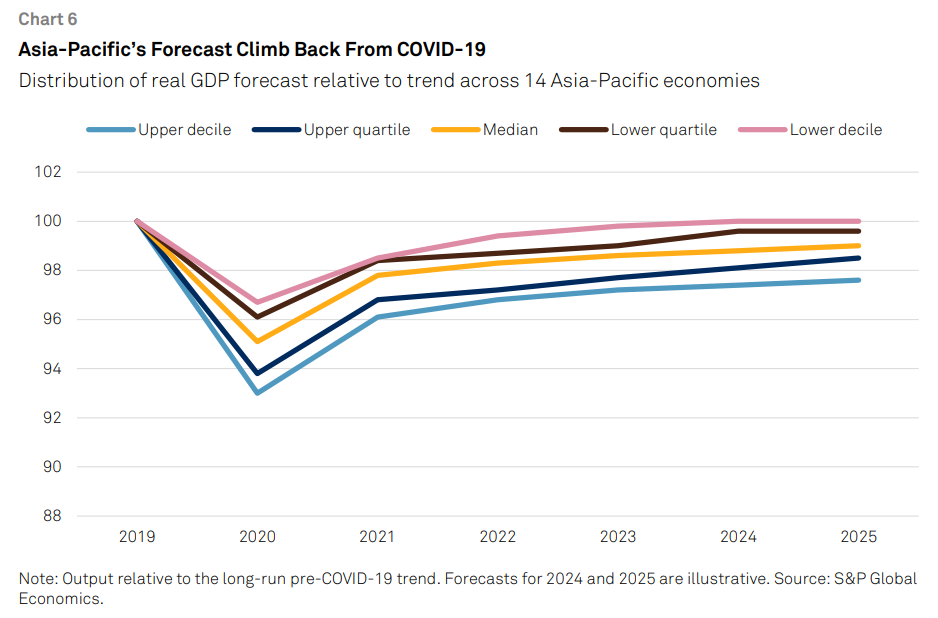

– Overall. We expect GDP growth for Asia-Pacific to fall to 0.3% in 2020 before a gradual recovery, implying a two-year income loss of over US$2 trillion. In 2020, corporates could see on average 10% to 15% less revenue, and banks may incur over US$400 billion in extra credit costs because of the outbreak.

– Risks. Our top risks are stricter and longer COVID-19 measures, higher debt leverage, tighter financing conditions for lower-grade issuers–particularly in U.S. dollars–and that the U.S.- China dispute will reignite.

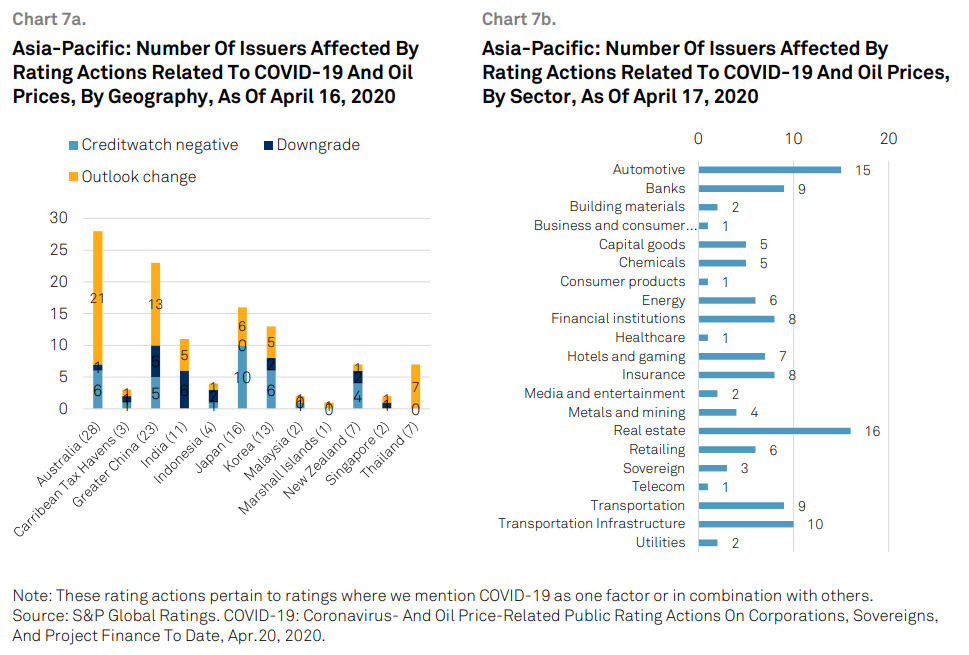

– Credit. While government monetary and fiscal actions provide some buffer, the slump in consumer and business demand will strain borrower credit quality, resulting in an escalation in missed or deferred payments and, for banks, higher nonperforming loans.

Credit conditions in Asia-Pacific going into the second half 2020 will be very tough. Containment measures to stem the spread of COVID-19 have escalated regionally (outside China) with global confirmed cases doubling to more than 2 million. These measures, together with business and consumer behavioral changes, are having a wider effect on credit conditions in Asia-Pacific beyond what we estimated in late March (see “Credit Conditions Asia-Pacific: As Bad As 1997, ” published March 30, 2020). Based on the experience of China, we believe the COVID-19 recovery period will take much longer than many had earlier expected.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.