Iron ore price charts for April 27, 2020:

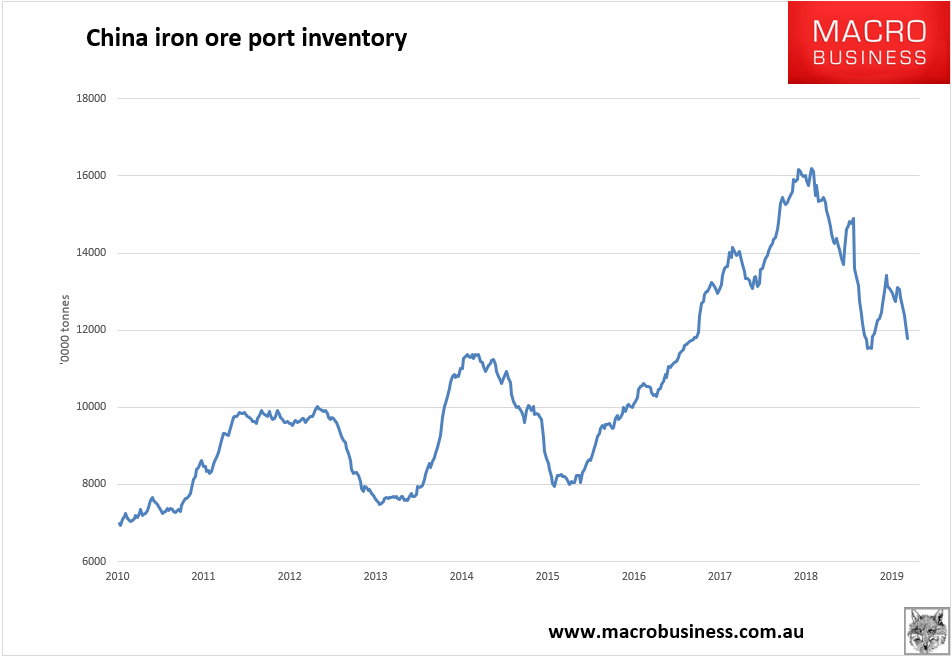

Spot down but everything was supported a little by falling port inventories:

Some argue that these can’t fall much more. History suggests otherwise.

Advertisement

Iron ore price charts for April 27, 2020:

Spot down but everything was supported a little by falling port inventories:

Some argue that these can’t fall much more. History suggests otherwise.

The full text of this article is available to MacroBusiness subscribers