Via Captial Economics:

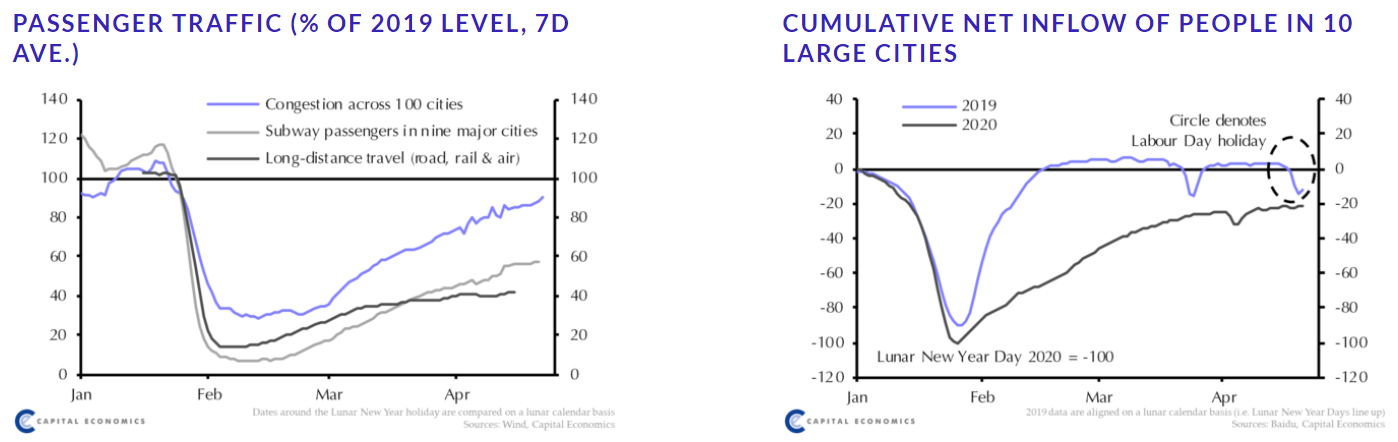

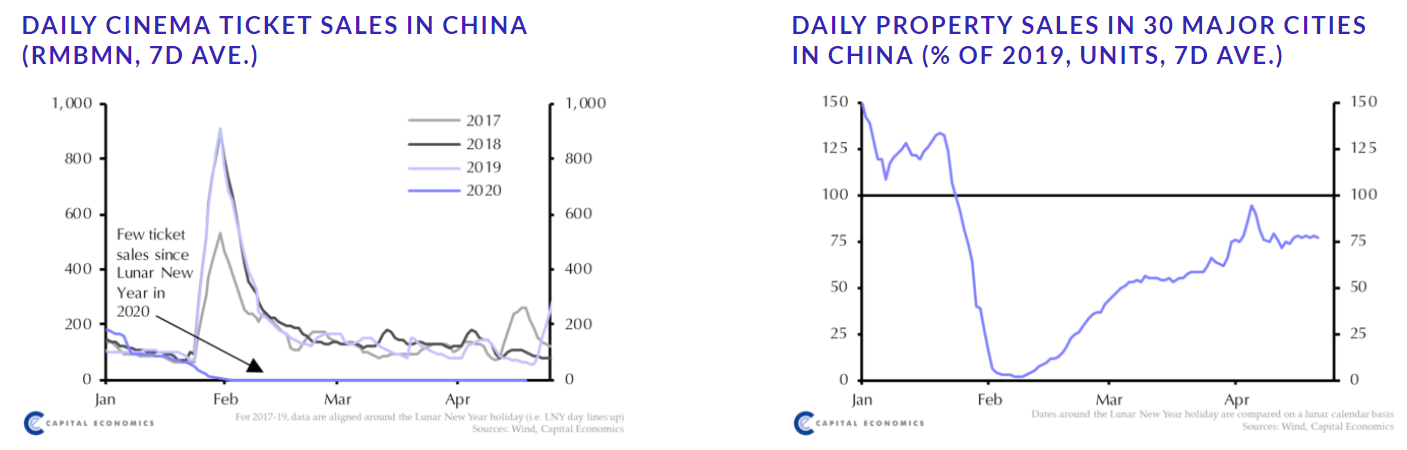

Most noteworthy for Australia is that stalled property sales recovery. Volumes down one quarter is worse than the 2015 bust that crushed bulks.

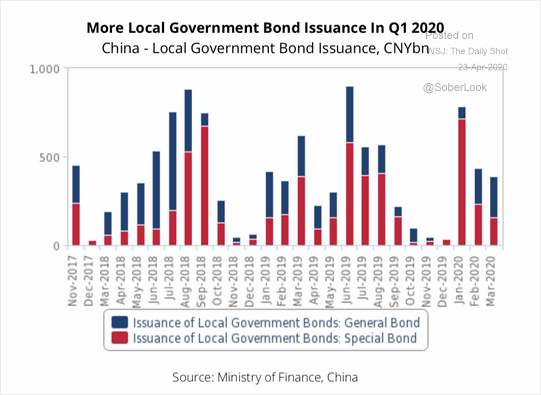

There are offsets in infrastructure with local governments on the move:

Advertisement