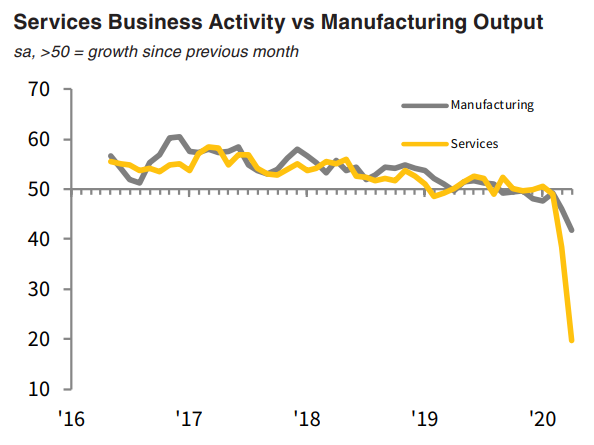

The latest Commonwealth Bank Flash Composite PMI® pointed to a much stronger contraction of the Australian private sector during April, with the decline particularly severe at service providers. The coronavirus disease 2019 (COVID-19) led new orders to fall at a steep pace, with employment scaled back markedly as a result. Both input costs and output prices decreased, but this was reflective of trends in the service sector as manufacturing inflation trends accelerated.

Manufacturing is seeing a garden variety recession. But services are seeing Armageddon.

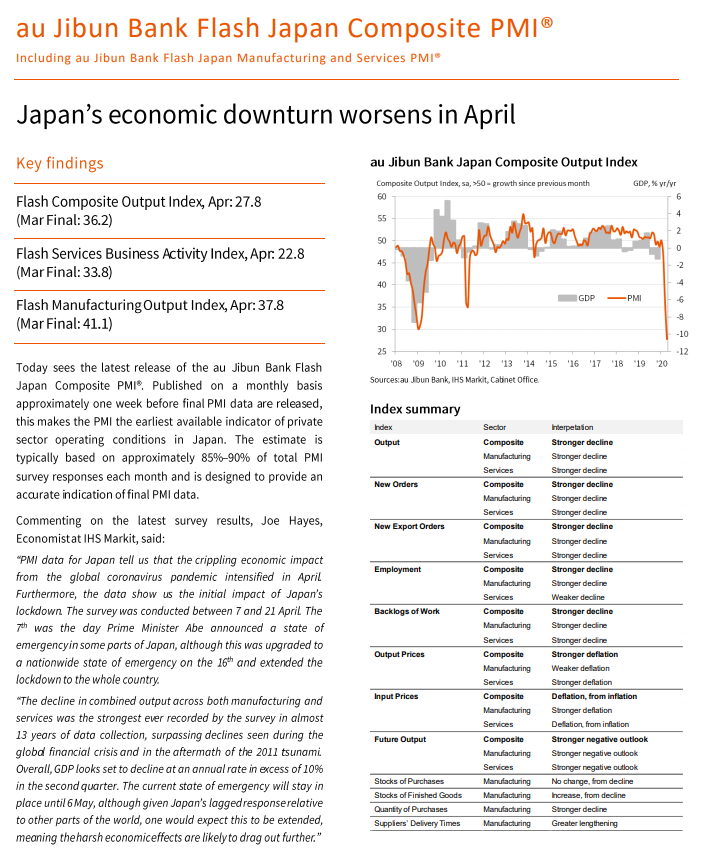

The same pattern is apparent in Japan today with services much worse hit:

Advertisement

We will see this pattern repeated worldwide.

The difference between Australia and just about everywhere else is this:

Advertisement

Our manufacturing output is so small at 5% of value-added that it offers no protection against a people-to-people shock. That could have been an illness, sudden degloblisation, war, commodity crisis, or something else.

COVID-19 has exposed the much-celebrated Australian services economy – that sells nothing but houses and cappuccinos to one another – as little more than an imbalance that will now violently adjust.

An entire generation of economists should be hung out to dry.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.