That it will be a depression is yesterday’s news. What kind then? Greg Jericho kicks us off with some useful musing:

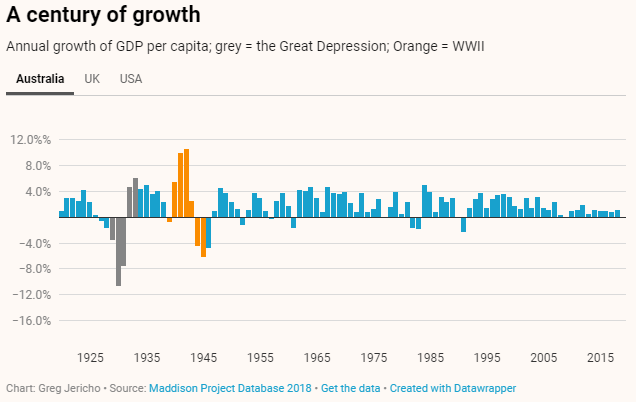

Through my lifetime there have been three “worst since the Great Depression” times for the economy – the early 1980s, the early 90s and the global financial crisis. In each case we never really got close to experiencing dramatic declines in production and income that happened during the 30s.

Out of those three cases the worst our GDP per capita ever fell in a year was 2.2%. By contrast, during the Depression, there were three consecutive years where it fell by more than 3.5% and one where it fell by more than 10%.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.