You’ve got to love equities. They are the true village idiot of markets. Convulsing one way or the other until they are finally right by random walk!

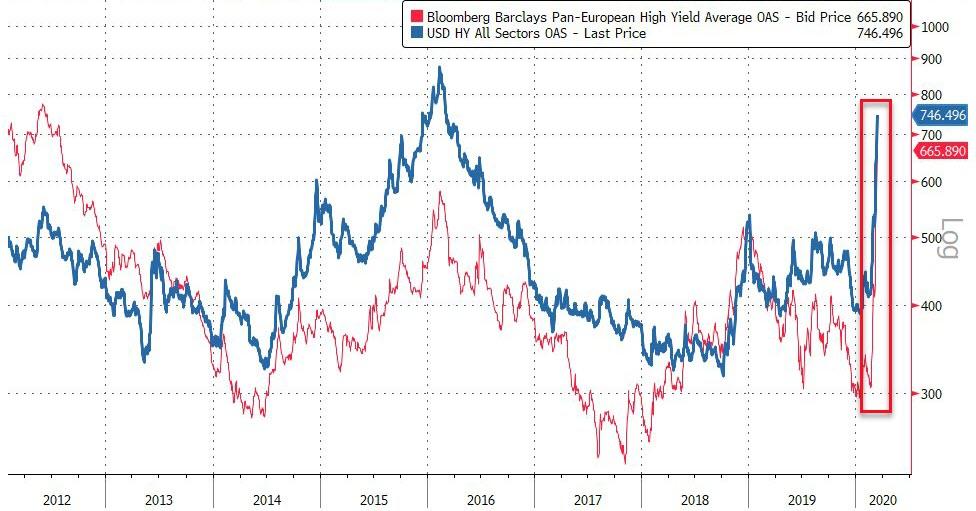

Meanwhile, credit has no choice but to reflect underlying reality. And what it is saying is not encouraging at all.

US junk apreads are on a tear with European trailing:

Advertisement