DXY was hammered again last night as EUR blasted off:

The Australian dollar was soft against DMs:

But powered against EMs:

Gold is poised for higher:

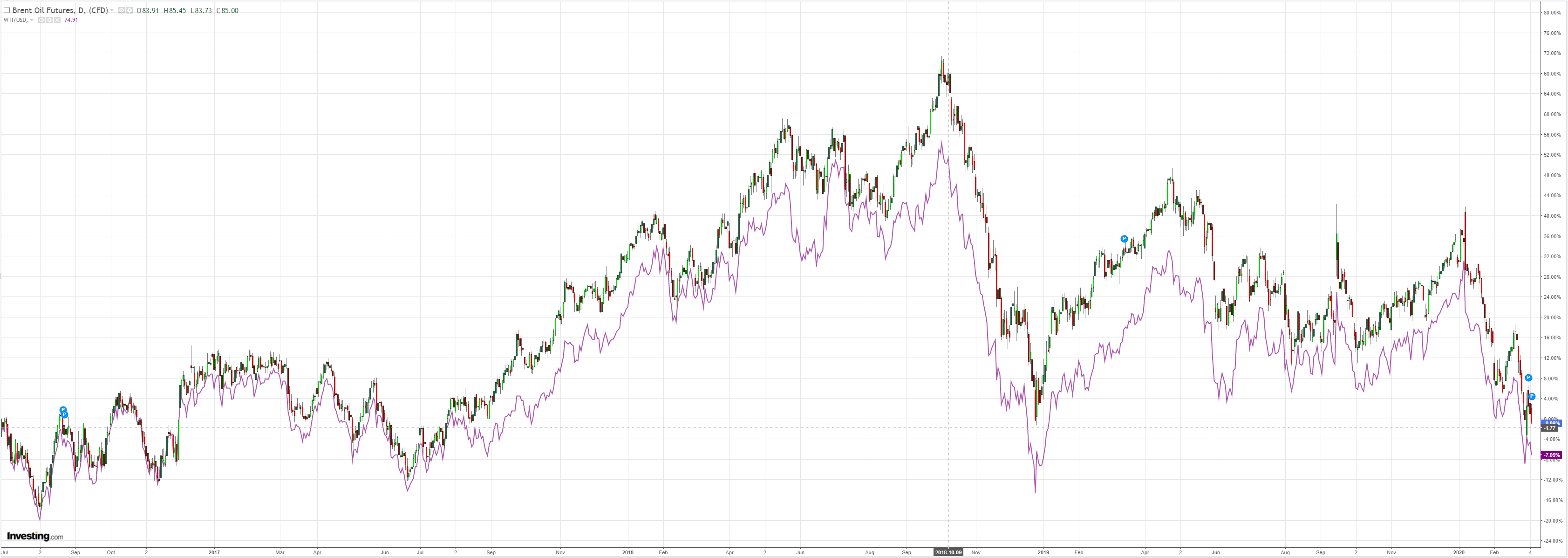

Oil was smashed despite OPEC cuts:

Metals did better:

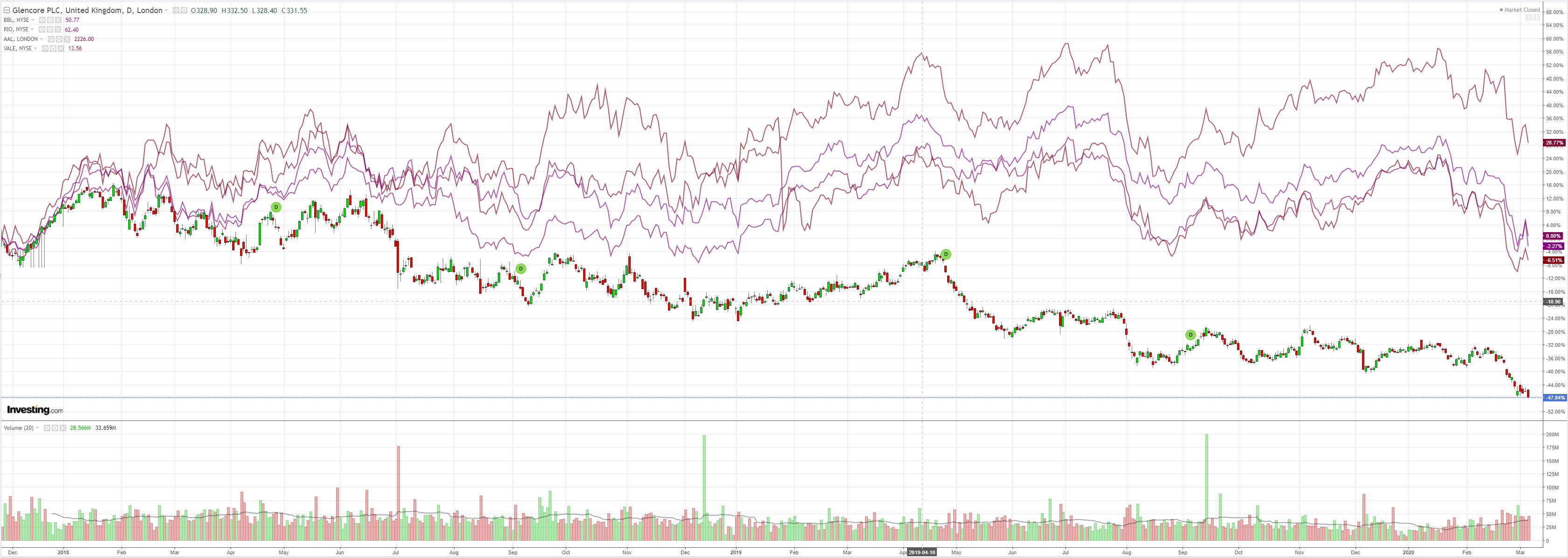

But not miners:

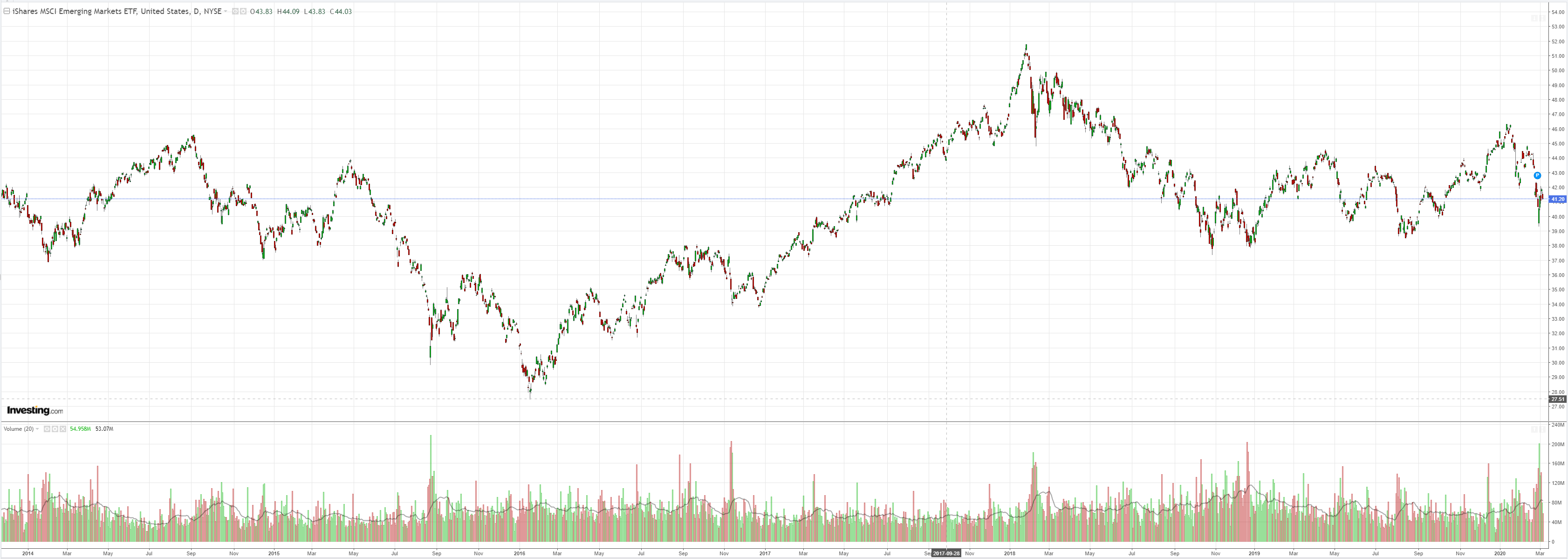

EM stocks fell:

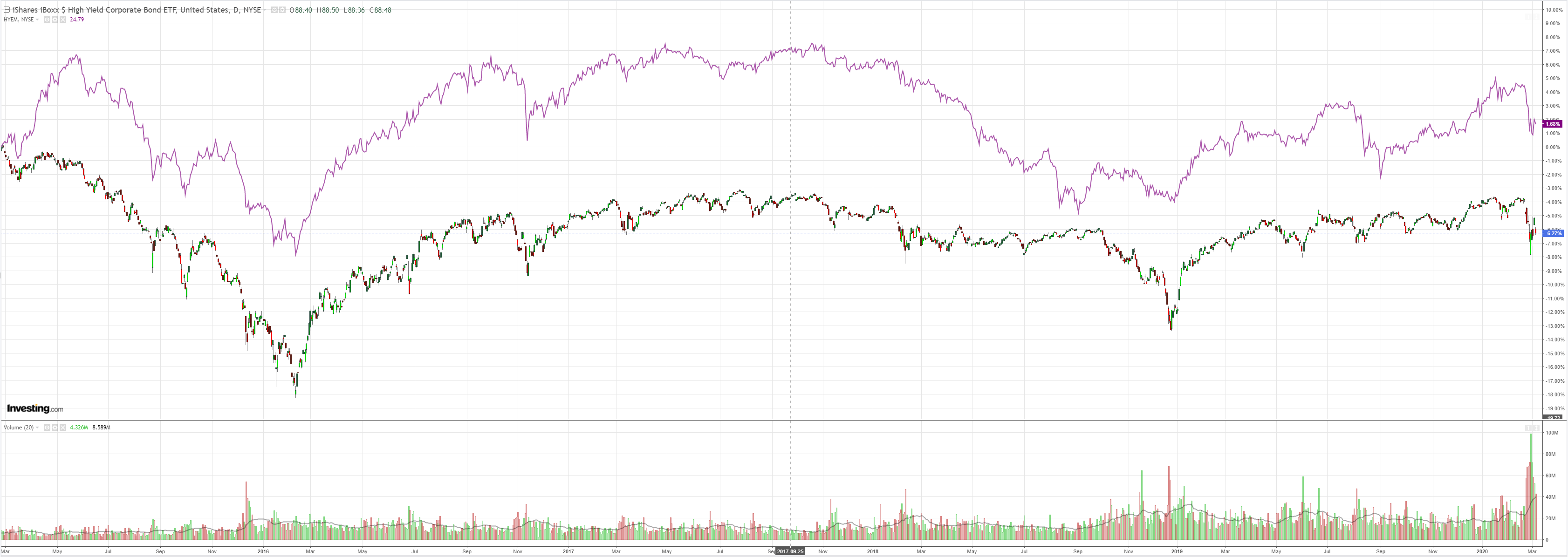

And junk:

Bonds boomed:

Stocks swooned:

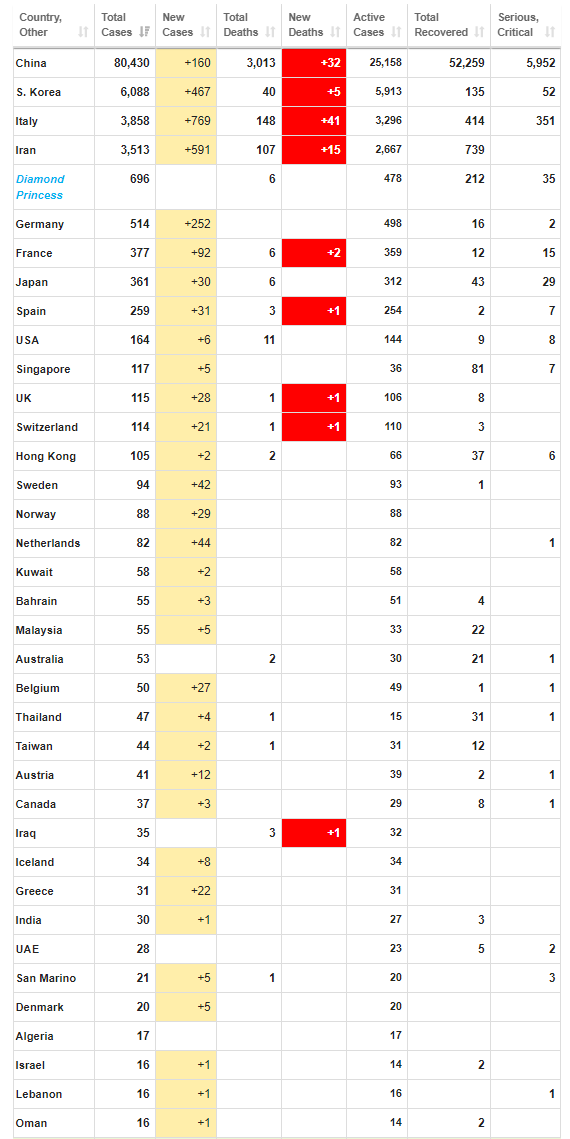

China’s virus has spread everywhere now and is exploding in Europe:

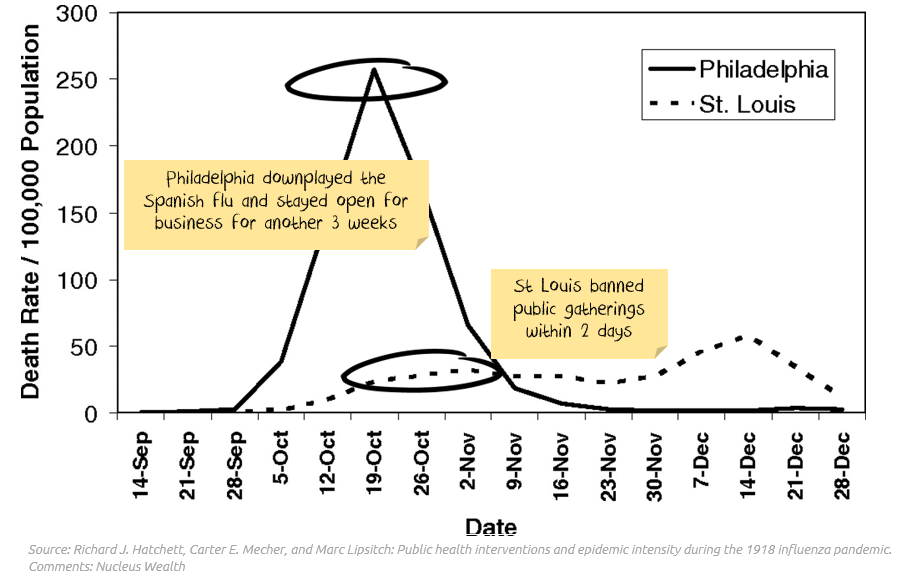

It looks to me like Europe has taken the path of Philadelphia instead of St Louis:

It’s far too late to close borders. This was a conscious choice to share in Italy’s pain to support the Eurozone project. I hope it doesn’t backfire.

Anyway, what lies ahead is some combination of mass casualties and localised shutdowns that will smash the EZ into deep recession over the next quarter. I hope its dodgy banks are ready.

What is most interesting is the bid for the EUR which is now looking quite persistent amid the crisis. The answer is the unwinding carry trade, previously from the FT:

The euro has entered a new phase, according to Deutsche Bank, rivalling Japan’s yen as the currency everyone wants to borrow — but no one wants to own.

In a research note published this week, London-based strategist George Saravelos said the European single currency could be expected to be trading at around $1.40 now, as investment flows have “swung to a huge surplus”. Instead, it is pinned around $1.10 due to what he describes as a large set of other outflows.

Crucially, he said, Europe has become a big lender to the rest of the world, marking “an important regime break” for the currency. Loans by eurozone banks to non-residents have climbed to levels not seen since 2008, while euro-denominated liabilities of non-EU banks have picked up sharply.

On Deutsche’s estimates, about two-thirds of the eurozone’s €455bn surplus in its balance of payments over the past 12 months can be attributed to such activity.

…“The euro is likely to exhibit increasing ‘carry trade’ behaviour where depreciation is gradual but appreciation pressures sharp as positions are unwound,” Mr Saravelos said.

And so it is. It does not appear that thre market is onto it. It keeps moving EUR shorter:

So the bid might turn even more violent as the risk unwind continues.

For the Australian dollar this is a very unwelcomed development. I still expect it to fall versus all major developed economy forex but a tumbling DXY will make it much harder.

This might have been offset by an aggressive central bank but we have the pansy RBA obsessing over a 25bps pop gun when it should be loading up the QE howitzer.

The good news is it is very gold bullish as DXY succumbs.

We have rebalanced our forex holdings across the USD and EUR because we simply don’t know how sustained this break with tradition will be. A strong EUR might reverse as the virus shock turns financial shock, or intensify.

Even so, I expect material new lows for the AUD against both because Australia’s economy is by far the worst positioned with six months of winter, virus and shut down ahead versus only a few for the northern hemisphere.

David Llewellyn-Smith is Chief Strategist at the MB Fund which is very conservatively positioned for coronavirus risks including a falling Australian dollar.