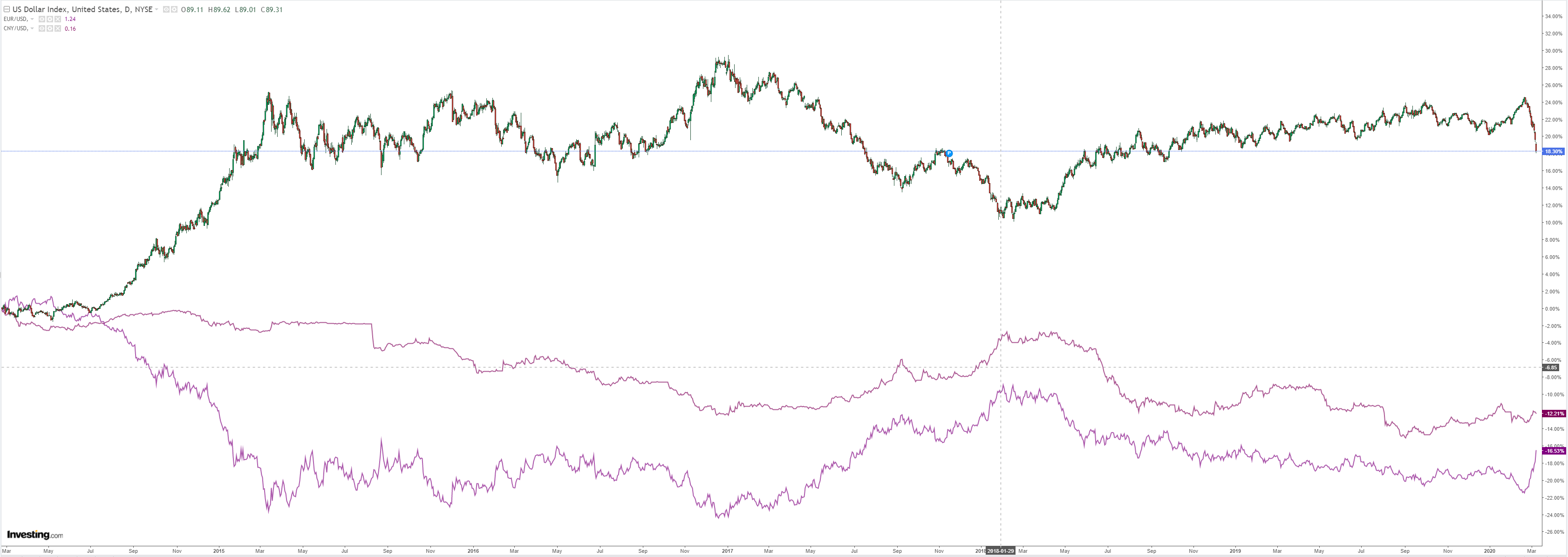

DXY is in free air and crashing as EUR, the new haven of the world (!?!?), tears the roof off:

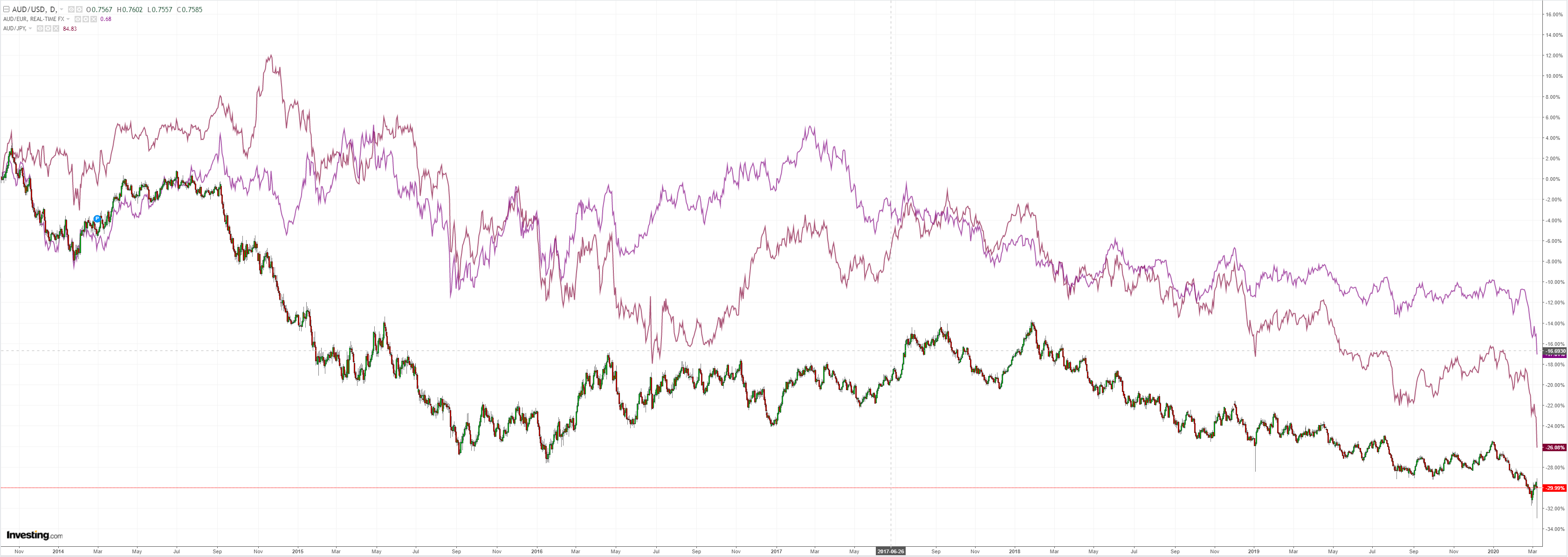

The Australian dollar ripped higher following yesterday’s fat finger:

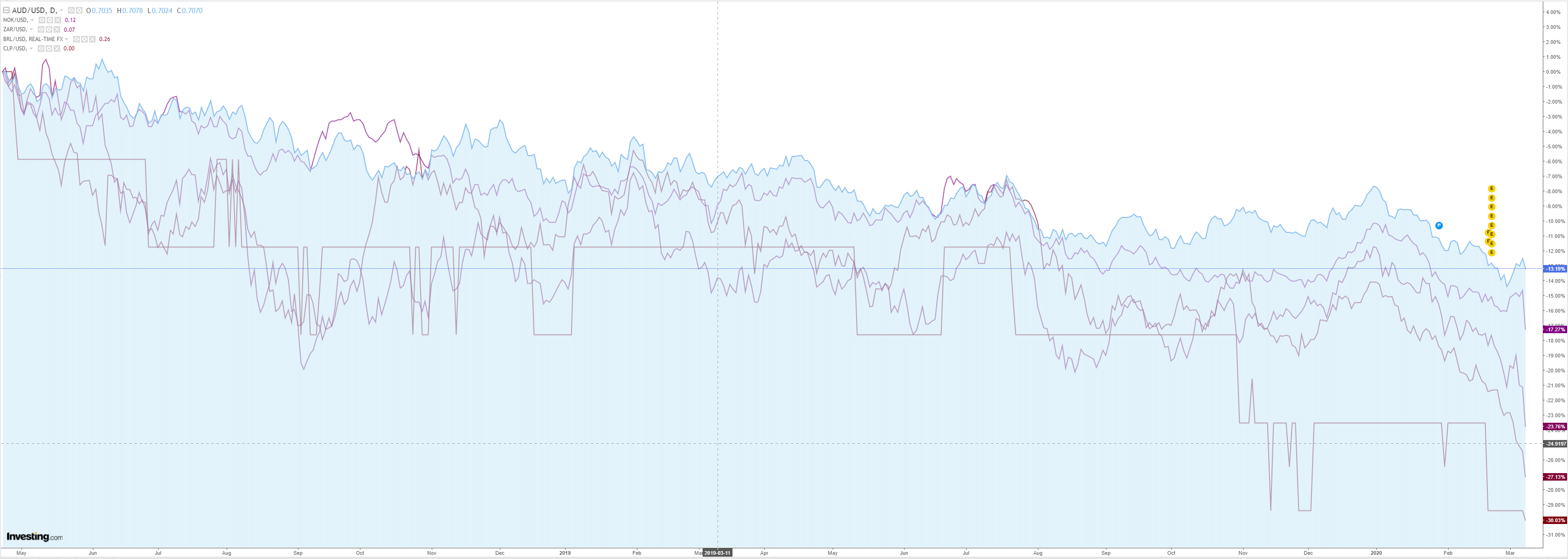

It is caning EMs:

Advertisement

And all other commodity currencies:

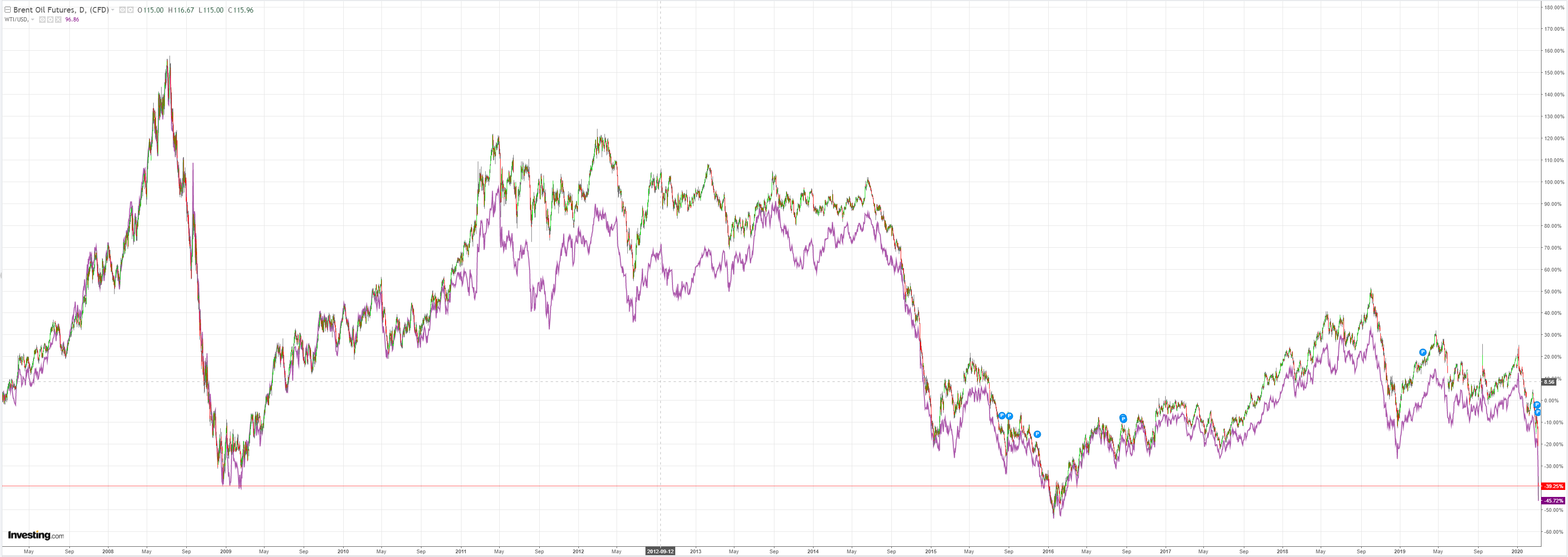

Oil will halve yet:

Gold has not pushed through:

Advertisement

Base metals broke:

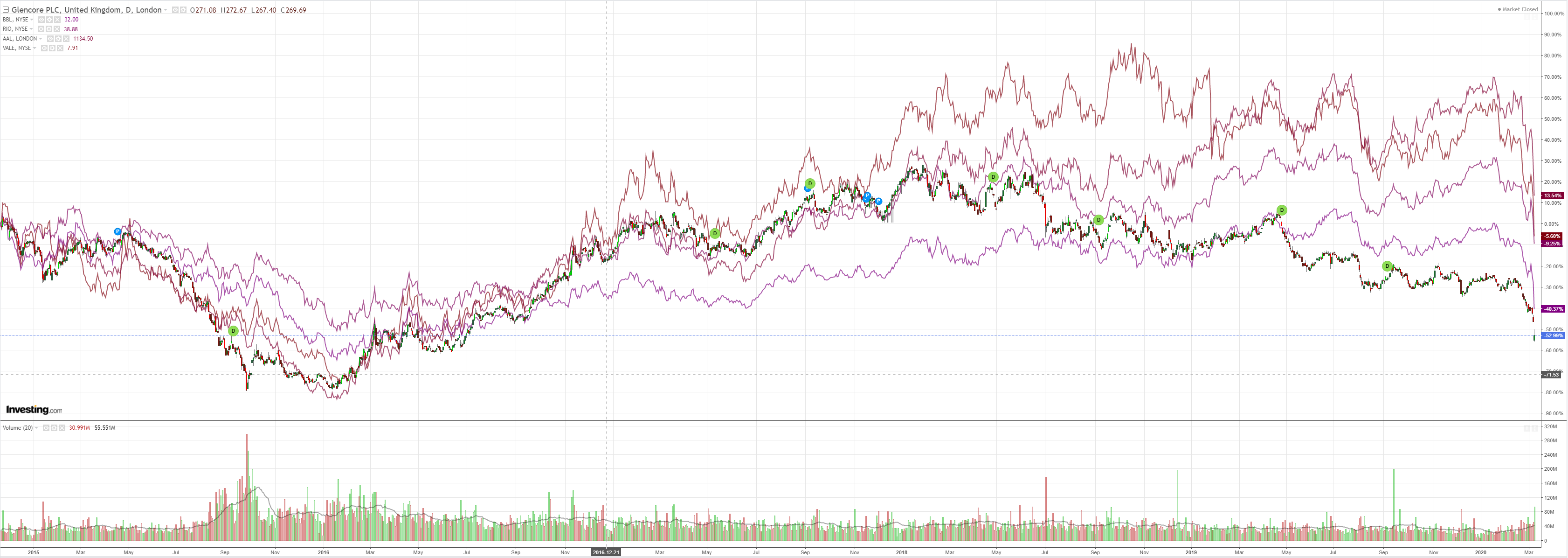

Miners flushed:

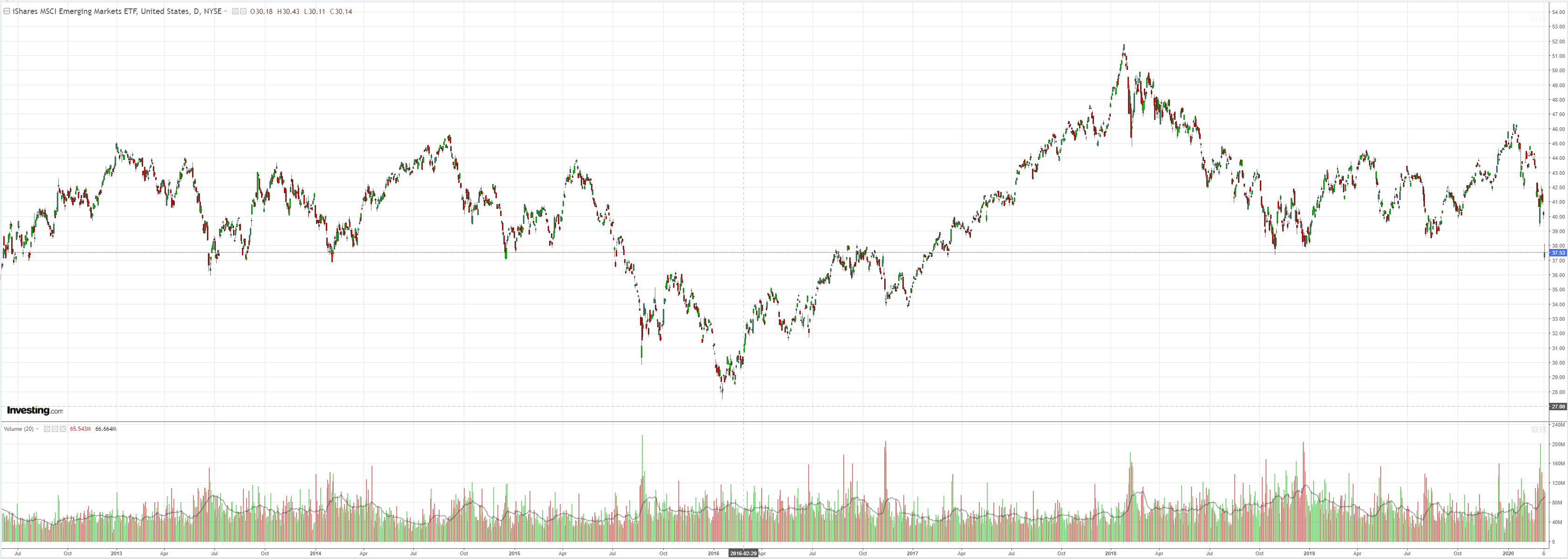

With EM stocks:

Advertisement

Junk committed suicide:

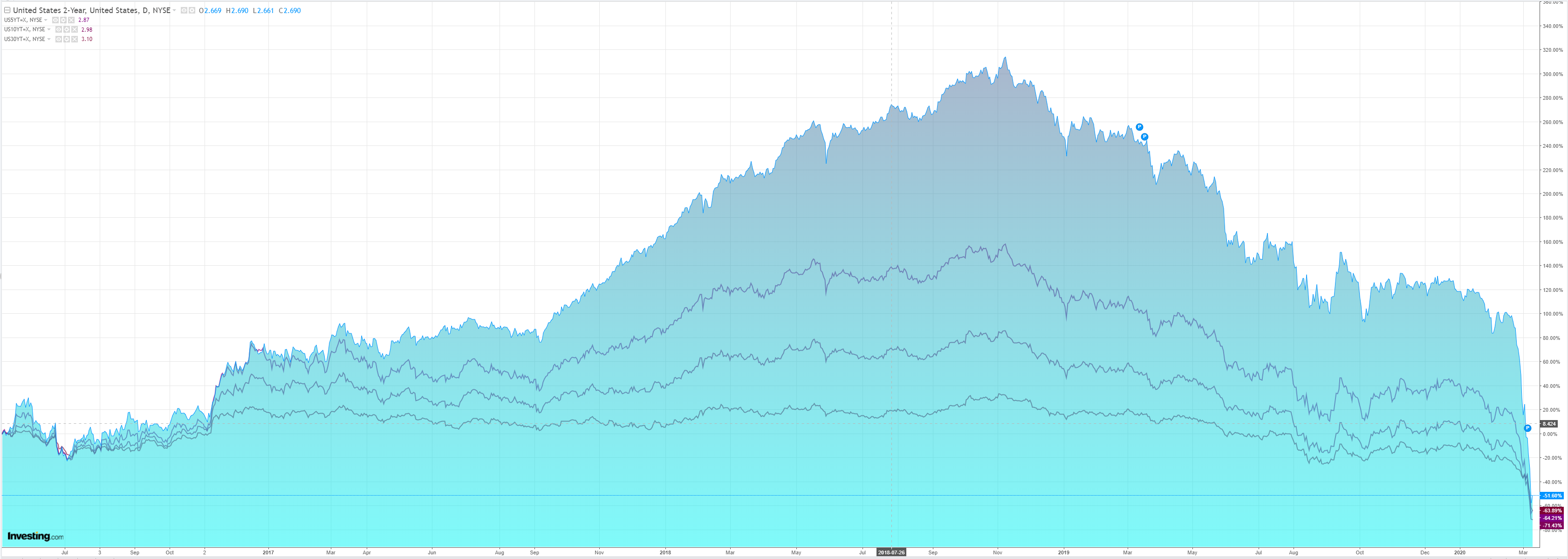

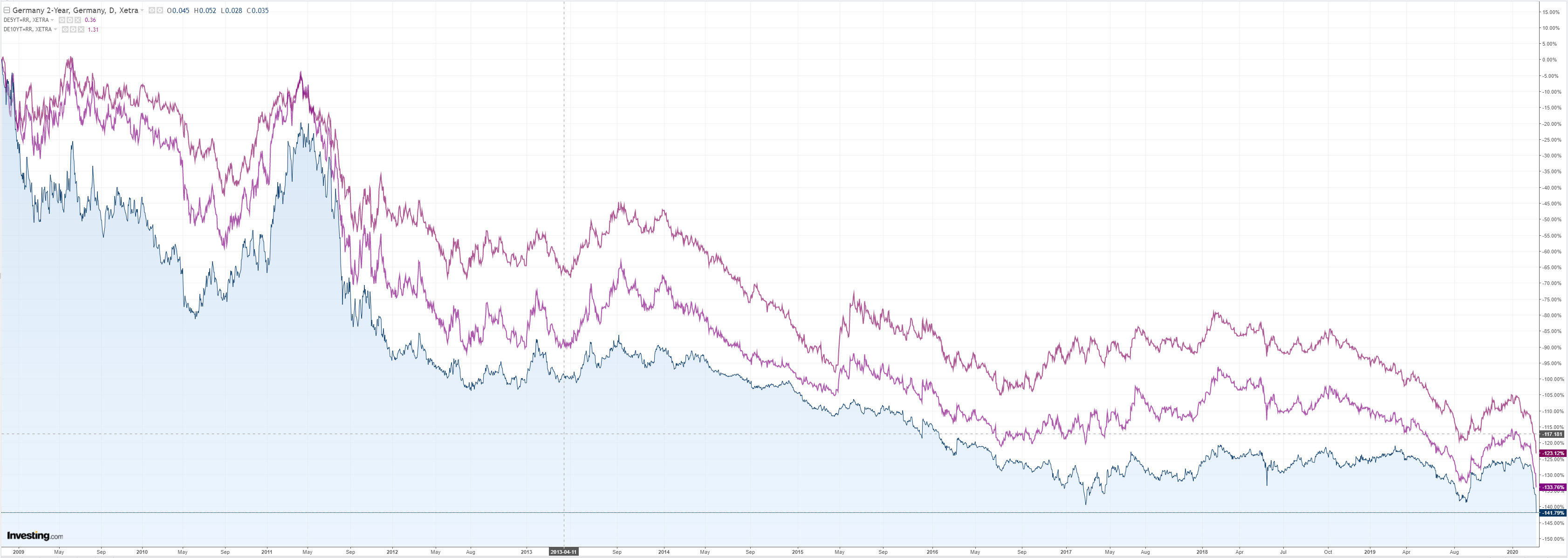

All bonds but Australian raged higher:

As stocks crashed. And they have still only blown the froth off:

Advertisement

The story for the Australian dollar now is how far the RBA has fallen behind the curve. Bond yields and the currency are stalled becasue the bank’s overly cautious cut has left it last in line for further easing. We don;t even know waht kind of QE it will do.

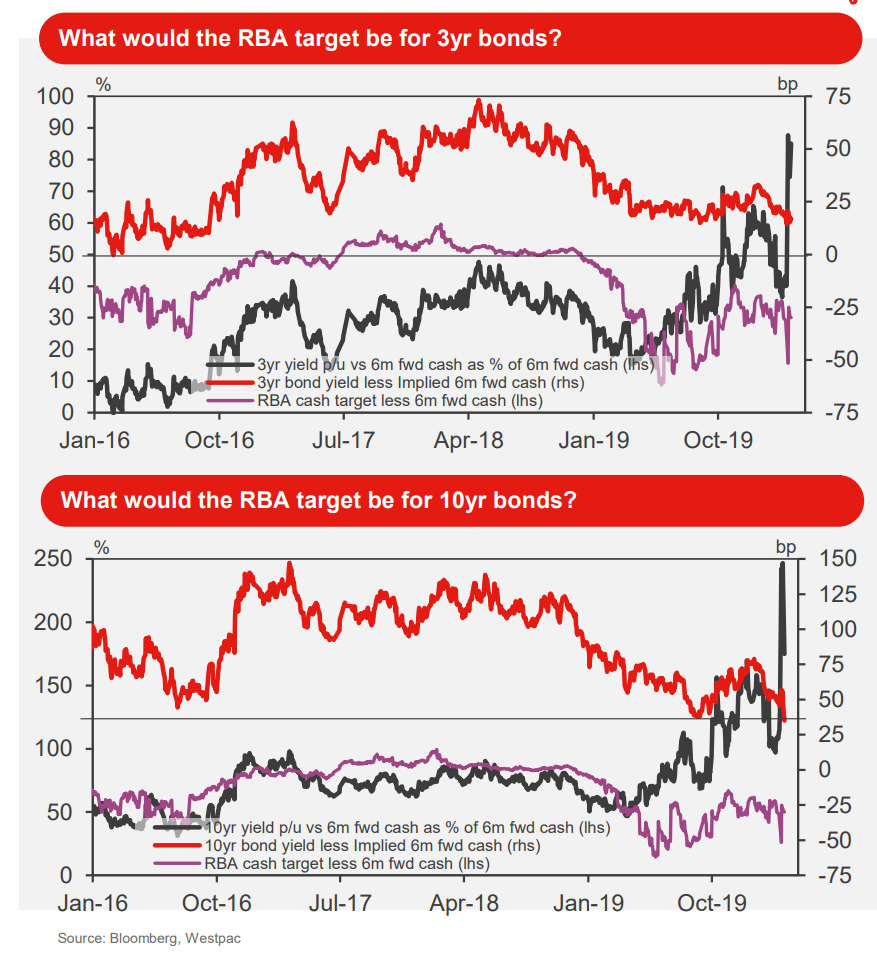

Westpac takes a shot at it:

Advertisement

• In the week or so since the RBA delivered its 25bp rate cut last Tuesday, the market has pushed the odds of a follow-up in April to 100% and even pushed the terminal rate to around 5bps or so below the 0.25% level that we regard as the lowest cash target that the RBA would adopt using “conventional” monetary policy tools.

• Beyond that, we have long advocated an “unconventional” programme of asset purchases, which we saw as the RBA buying ACGBs and semi-government bonds across the curve. We re-highlighted that in our last weekly essay. So it is of interest to us that the dialogue around the RBA’s QE potentials has shifted such that not only are we discussing the likely timing of the RBA’s introduction of QE, but, more importantly, its construction.

• That is, there is a growing view that the RBA might undertake similar unconventional policy as the Bank of Japan which has implemented a “yield curve control (YCC)” policy. YCC involves setting a numerical target for government bond yields, rather than the RBA announcing the dollar amount of bonds that they intended purchasing. In the BoJ’s case, in Sept. 2016, they committed to peg 10yr JGB yields around 0%. They have held to that target ever since.

• The RBA has yet to make any mention of this as a possible policy approach. Rather, in November 2019, Governor Lowe did suggest that negative rates were out of the question and that QE would likely be in a form of government bond purchases. Perhaps YCC is consistent with the latter suggestion, so it is worthwhile discussing some of the potentialities arising out of the policy. We do so below and on the next page.

• A number of questions quickly arise, some of which are relevant to the “traditional” QE approach of asset purchases. They include:

– What maturity or maturities might the RBA target? Shorter maturities would have more immediate impact given the greater importance of short end rates to most private borrowers. That would also assist lower wholesale rates at the maturities often related to the currency, a lower level of which the RBA has explicitly noted as a target for the policy stance. We do question what might happen if the RBA is left defending their policy target(s) in a period of rising rates – presumably some time in the future. Given that under YCC the central bank is defending a price, not undertaking a pre-determined amount of purchases, this could create a situation in which there a MORE purchases undertaken than under more traditional approach.

− Would the RBA change its yield targets? The previous comments imply that the RBA kept targeting the same yields regardless of market conditions. That could provide some sense that AU bonds were a “safe haven” in times of a major market correction.

− However, there might be some scope for the RBA to alter its target(s) over time. In this way the monthly Board meeting would garner considerable interest as the Bank contemplates adjusting their wholesale term structure targets rather than only focussing on the cash target.

− How many targets would the RBA have? In Japan, they have targeted long end yields. While we have already speculated that the RBA might target shorter yields, there is a case for longer maturities to be targeted as well. The argument is largely predicated on the amount of ACGBs and semis available in the “free float” of bonds on issue. On the assumption that the RBA would not wish to create too much market “dislocation” they might wish to target yields across the curve. While it is true that buying shorter maturities could steepen the curve, which would benefit financial intermediaries such as banks, and in addition it could make the AOFMs refinancing task easier (perhaps substituting for the current buyback tenders), it would be competing at the short end with ADI’s LCR portfolios. Targeting longer maturities would also assist in the financing of infrastructure projects which is the focus of a lot of long end issuance at present, especially from the states. So it is not absolutely obvious that short rates will be the only focus of YCC.

− What will yield levels will the RBA target? Presumably Of interest relationship between, say, a three year bond and the overnight. With 3yr bond yields at 0.36% and 10yr bonds at 0.60%, there is not a lot of room to spare. In order to keep pressure on the currency, presumably the yield targets would initially be set below where we are today. So, with both rates above the implied terminal cash rate, there is little reason to bet against the current rally being sustained.

− Of interest is the market’s assessment of the equilibrium between, say a 3yr bond and the cash rate in an environment where the cash rate was expected to be stable for, say, two years.

− We have monitored this relationship over time (refer chart at top of previous page). In more usual markets, in a “no change, or potentially lower, cash rate” regime 3yr bond yields have averaged a spread to implied forward cash of around +25bp. Alternatively, in a “no change to potentially higher cash rate” regime, the average spread has been around +50bp. However, the relationship appears to be breaking down at these current low outright yield levels, as highlighted by the black line on the chart which plots the relationship between this spread and outright levels. It is a similar case with the 10yr yield (refer chart at bottom of previous page).

− For now, our assumption would be that the RBA targets a 3yr bond yield around the cash rate, or perhaps a handful of basis points above that. We would also expect any targeting of the 10yr maturity to keep the curve relatively flat at around 15-20bps,so any outright target of around 0.40-45%.

And what if everyone else’s bond turn negative? Will the RBA’s target yield prevent further falls? Why are we even having this debate mid-crisis? Why wasn’t this clarified by the bank years ago? Why don’t we know exactly what the RBA;s reaction function is and what it will do when it is reached?

Because the joint is fast asleep. The AUD is now delivering an enhanced shock to Australia because of it.

I hate to tell you, RBA, but you’re cooked on interest rates. They go no lower. All you have left is the currency to stimulate. QE is also the best (only) way to force Recessionberg to spend.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.