From Christopher Metli, head of Quantitative and Derivatives Strategy at Morgan Stanley:

The stresses in many areas of the financial markets are spreading. The market is increasingly pricing in a seizing of the real economy as the market awaits more details on the timing and scope of response. Compounding these problems is growing financial stresses as cash becomes dear, which threatens to create a negative feedback loop between markets and the economy. Poor liquidity, a breakdown in correlations, physical exchanges closing (CME for now), and many working from home compound the problem. While a 2008 style financial system meltdown may not be in the cards, the market is increasingly demanding greater liquidity backstops and greater fiscal action. QDS noted on Monday financial markets had Crossed the Rubicon, and the decline now may not stop until the market gets what it is demanding from policymakers.

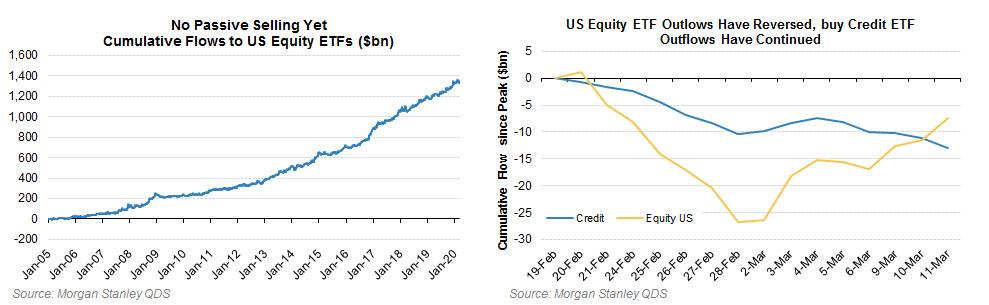

Systematic strategies have been the leading sellers so far, and asset managers have likely contributed as well. But bottoms up hedge funds have not derisked to the same extent, and retail / passive has not yet sold materially either. Only when those groups sell (and investors get clarity on the policy response) can markets find a durable bottom.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.