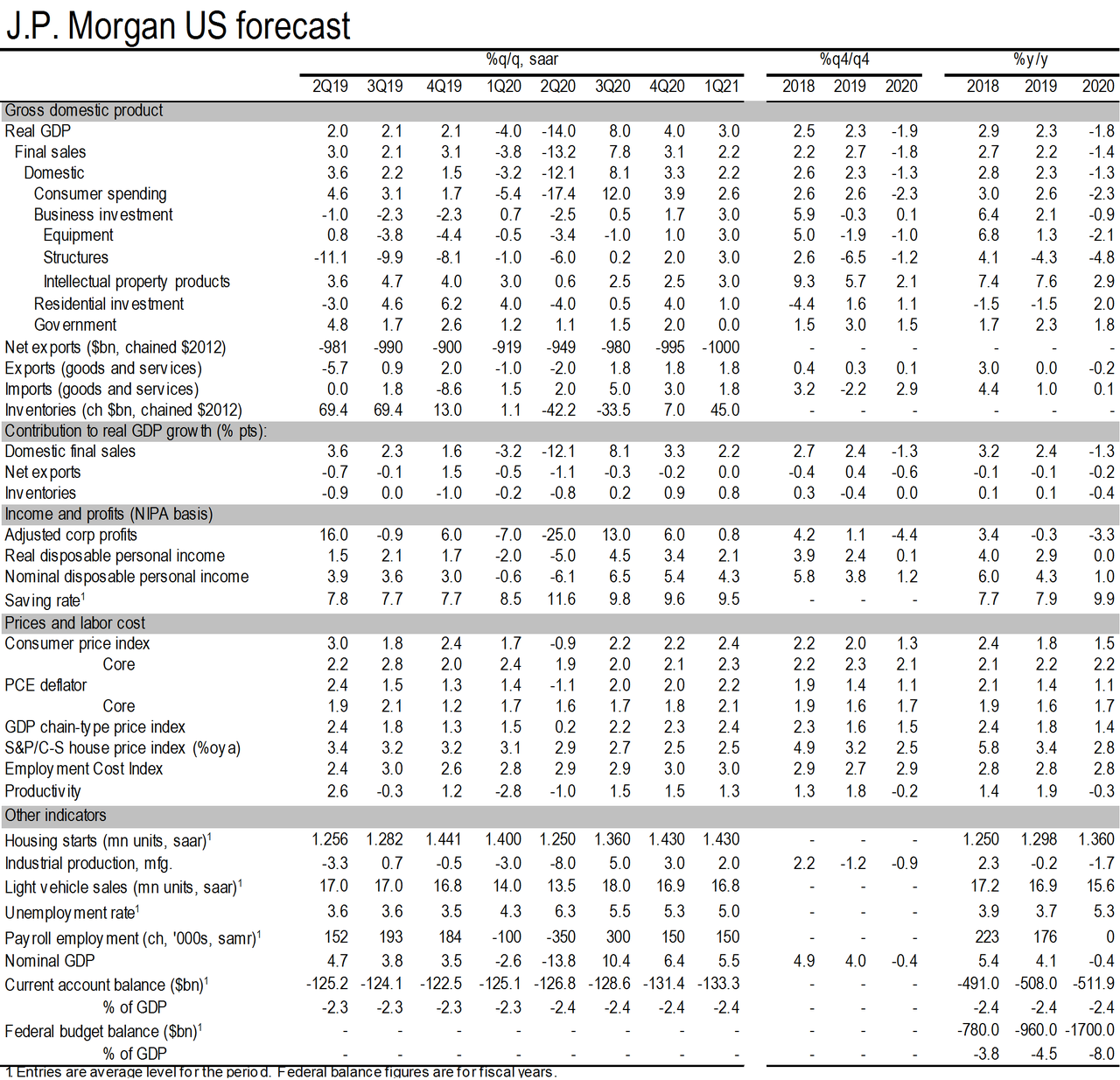

As before, we continue to assume that ground zero of the economic weakness is those consumer services with inadequate social distancing: air travel, movies, sporting events, etc. In our reckoning of where to draw the lines, this group represents around 7% of GDP. We assume activity in this group falls to 63% of normal activity in March, followed by 25% in April, 63% in May, and fully recovers to 100% of normal activity in June. We do not assume a reoccurrence of the virus in the fall. With these assumptions alone, this group would subtract 4%-points from Q1 growth and almost 11%-points from Q2 growth before adding 7%-points to Q3 growth. On top of this we assume spillover to other categories of spending, particularly in Q2 as the weakening environment depresses sentiment, destroys jobs and weakens business and household balance sheets. We expect these spillover effects to last in Q3, counteracting the support to growth from activity coming back on line. Crucially, we expect a vigorous policy response to partially offset these negative feedback loops. The Fed has already done a lot, and will remain creative in trying to do more. Additionally we are now expecting $1 trillion in federal fiscal support to the economy. We expect this to come through (i) direct cash payments to households, (ii) support for state and local government finances, and (iii) liquidity support to struggling businesses. While we expect rapid passage of this support, the deployment of funds in the economy should take a few months and is expected to peak in Q3. As before, we continue to see the inflation outlook driven more by demand weakness than supply weakness.

Prices of toilet paper and hand sanitizer will not rise enough to get inflation back to the Fed’s 2 percent objective any time in our forecast. Consequently, we have the Fed on hold this year and next.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.