DXY is an untouchable rocket ship. Judging by past episodes of US dollar shortage this has weeks to run:

The Australian dollar is now in outright free fall versus DMs:

Though it had a better day versus EMs:

Gold is still liquidating:

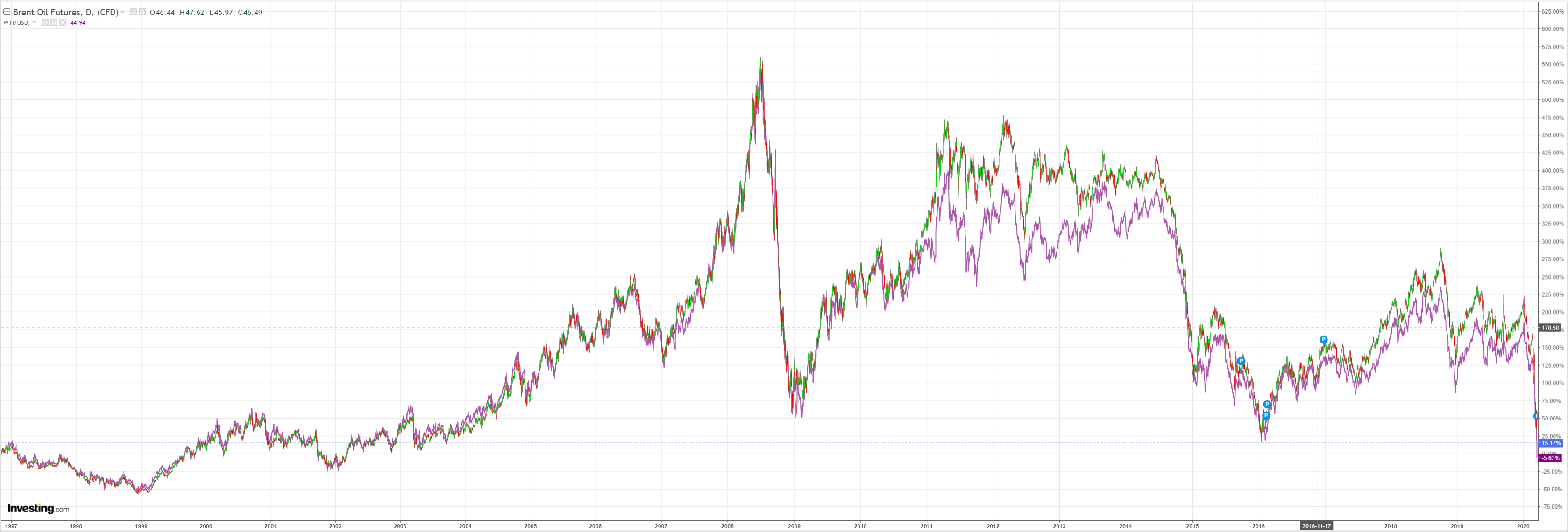

Oil is literally going to zero:

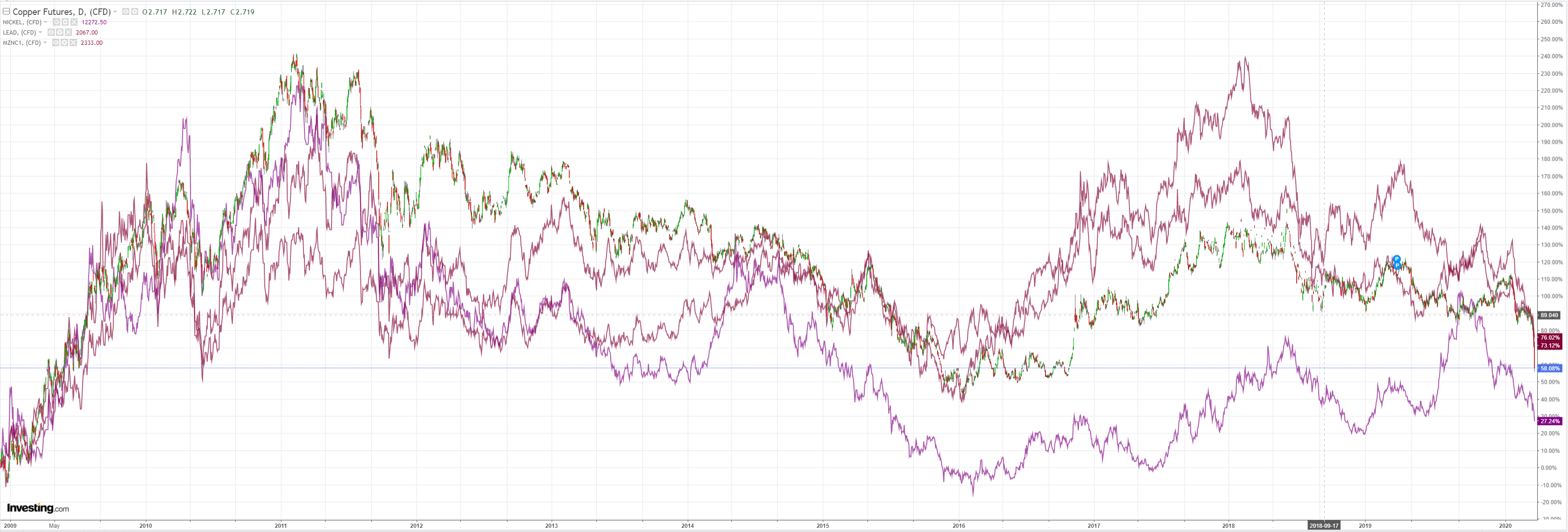

Base metals are next:

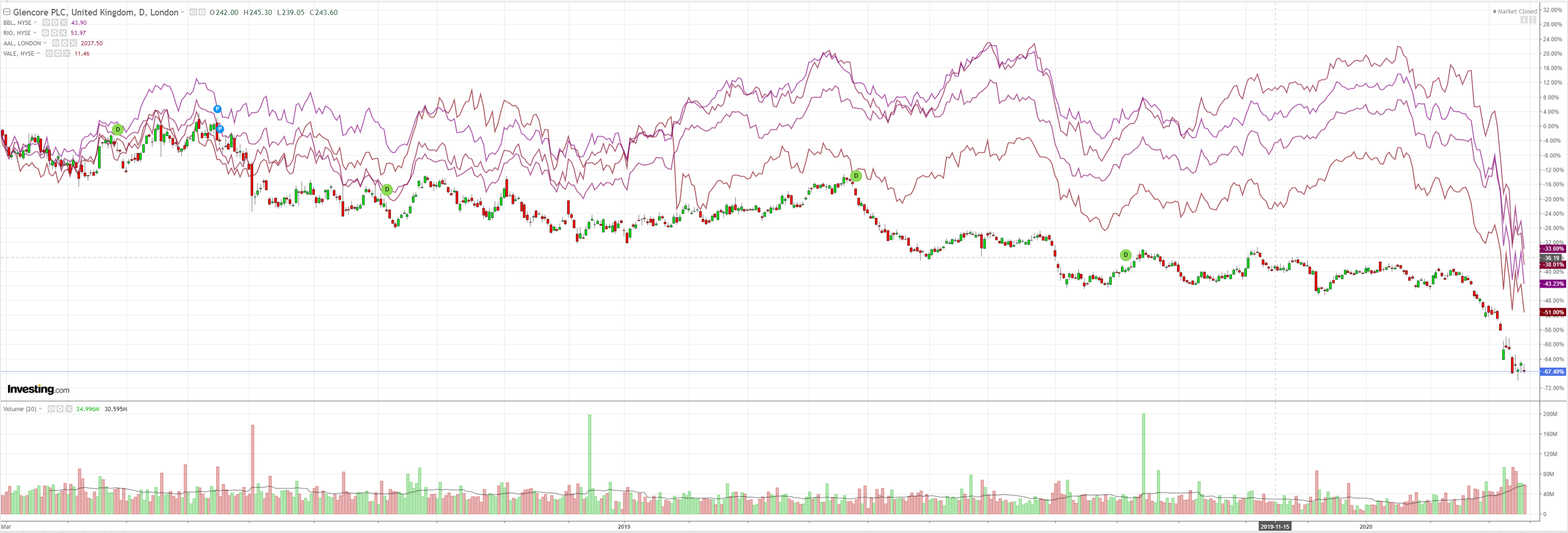

Miners are now iron ore pure plays. Good luck with that:

EM stocks are about halfway down:

Junk is further along the path:

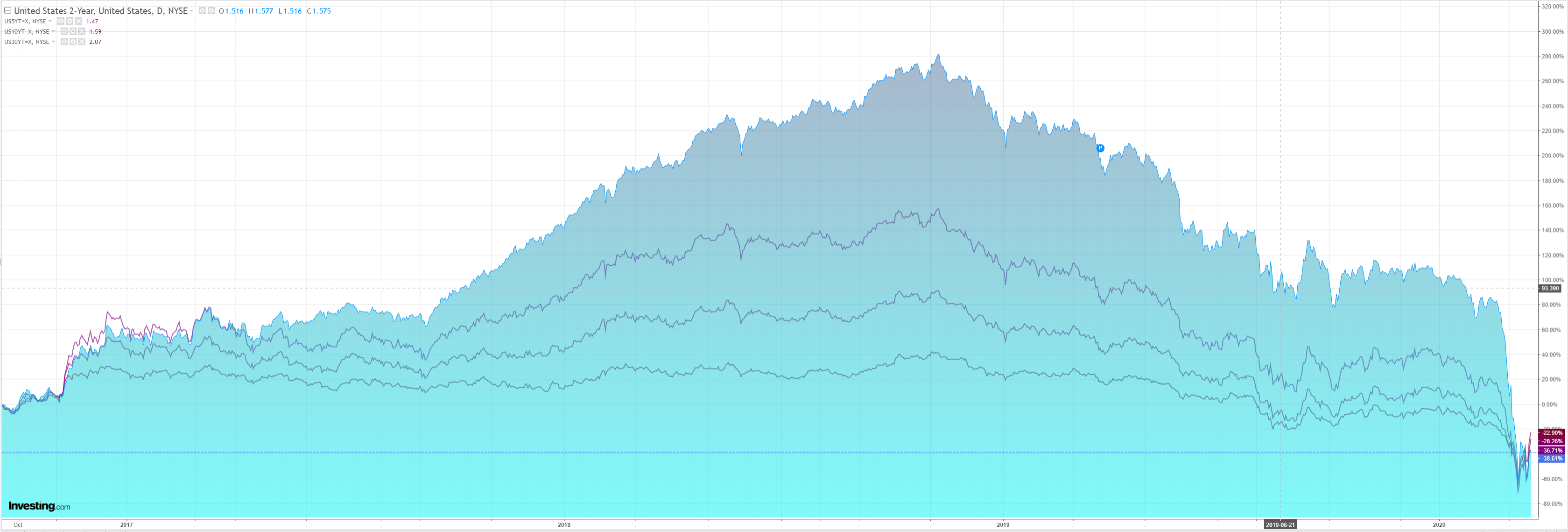

DM bonds all sold again:

Stocks were slaughtered again and took out 2018 lows:

It is pure and simple sell everything. So, let me explain as best I can on what I think is happening.

Global markets are siezed by an immesne margin call around the US dollar. RaboBank explains this:

Does anybody seriously think this [fiscal spending] will ever be repaid in taxes by an economy that will emerge with higher levels of debt, and the same structural low productivity and inflation and growth? No. Given this is “war”, the BOE and the Fed, etc., will be called in for fiscal support instead – as a slew of talking heads on Bloomberg TV–none of whom had ever previously supported MMT before as far as I am aware–all came out to demand yesterday morning.

After all, it isn’t like the Fed isn’t already offering trillions to the markets via an ever-expanding alphabetti spaghetti of channels. One can hardly keep up with the scale and breadth of them. The minutiae are covered superbly in the US by Philip Marey, who rightly saw yesterday’s expansion, or rather retreat, back to the kind of Fed primary dealer support available in 2008; and in the Eurozone by Elwin de Groot and Bas Van Geffen, who have been writing on TLRTOs and their ilk. Yet at root, each mechanism is merely a pipeline from the central bank and its fiat money power to various interest groups who need cash. For example, the new Primary Dealer Credit Facility lets the Fed lend USD against stocks, whose value–in a world where markets go and down 10% a day–will be determined by the Bank of New York Mellon. If we are already going that route, why not the Yang/UBI one too – especially if it is the only thing that is actually going to work?

Meanwhile, ticking away in the background is the USD64trn question of the most important pipeline. Not oil, with which we are choked, and where some are talking about the need for negative prices to stop the stuff flowing(!) Rather, Fed swap lines.

As we have repeated endlessly, the USD is THE global currency and Eurodollar is absolutely vital to understand. When you have an economic and financial crisis, everybody wants to tap local central bank liquidity; but when you have a global economic and financial crisis, everybody wants to tap US central bank liquidity. We live in a world in which emerging markets, now a huge slice of the economy, are addicted to USD borrowing, and have more outstanding USD debt than ever. They are desperate for dollars, and won’t be earning many from trade as global demand collapses.

The Fed has already opened swap lines with the major western central banks and Japan to ensure that they can get access to USD, which they can then use to swap with local currency, so easing USD funding pressures there. Yet the Fed has NOT offered this swap facility to emerging markets. Pressure is building on it to do so in order to prevent a USD liquidity squeeze hitting them on top of real economy damage from the virus: but can it and will it?

Consider that a Fed swap line is a precious political commodity. It says that your currency is, when needed, as good as USD: it has value in an emergency like this. Yes, the Fed would generate a lot of good will by offering swap lines to EM, and it would cement the USD’s global role even further. Yet money is power, and some critics allege the US has long manipulated the USD global liquidity cycle to first flood EM with liquidity, and then take advantage of the inevitable cyclical liquidity retreat to pick up assets at pennies on the dollar. Does it want to give that up?

Crucially, is the Fed going to extend swap privileges to the PBOC? The same China that was in a trade war and is still is in an undeclared Cold War with the US? That just announced it will kick out a slew of US journalists from both the mainland AND supposedly-autonomous Hong Kong? That has had officials publicly claiming COVID-19 is a US military operation? The implications of doing it and not doing it needs a whole report in itself – but either way there is a whiff of fin-de-regime about it.

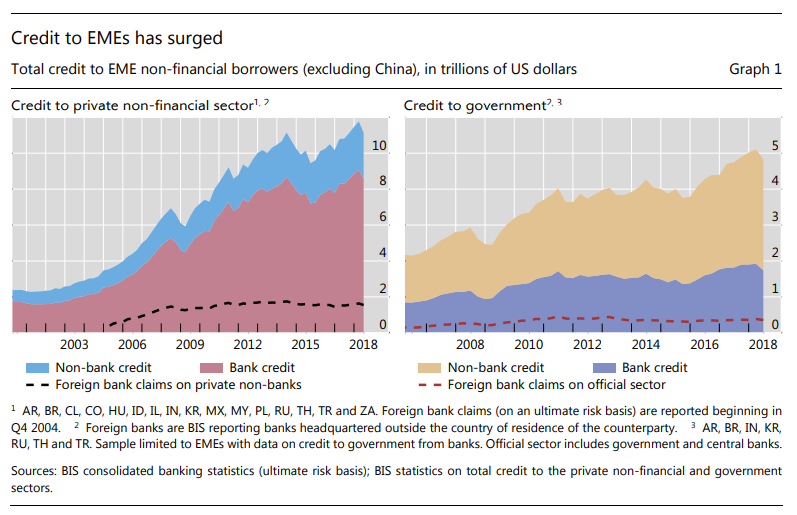

Emerging market now have foreign borrowings approaching $20tr USD:

Some large portion of this is denominated in USD.

But, as Rabo says, and as Zoltan Pozsnar has been screaming about, many of these do NOT have USD swap lines with the Fed. So, as global markets go to shit, credit markets sieze up along with local bank funding costs and lending, everybody needs to get their hands on USDs to unclog systemic margin calls.

Because they don’t have swap lines, they are forced instead to sell USD assets, even Treasuries, to get the USDs that they need.

The rising yields spook markets and force further liquidation of equities which, in turn, triggers even more liquidation of Treasuries as the trade of the cycle – risk parity – convulses through forced deleveraging.

In short, the entire viruous cycle of reflation of the past cycle is now in a dramatic, accelerated and self-re-enforcing unwind.

The Federal Reserve can manage this and slow it down but it has two problems in doing so:

- first, it is moving too slowly and is way behind the curve, and

- second, it does not have the swap lines and to get them into place is, in part, a geopolitical decision.

For instance, why would the White House, or any American for that matter, want to offer the PBOC a USD swap line today? To do so will literally be re-liquifiying its major geopolitical rival just as it tries to blame the US for the very Chinese virus that is killing Americans.

And many of the dollar-dependent EMs are stragetically aligned with China as well as its commodity demand has drawn them in over a decade.

What we have here is a catastrophic mismatch between reserve currency status and geopolitical reality.

This is both an immense risk and opportunity for the US. The Fed might re-liquify those nations that are US-aligned or teetering between the US and China, while ignoring those that have flown the strategic coop to China and China itself. That can win some nations back to the US sphere of influence, as well as punish those that don’t, and it may be enough to short-circuit the Treasury liquidation.

The risk is that such geopolitcally selective swap lines are not enough to end the liquidation and everything that prices off a skyrocketing risk free rate goes to zero. Including the Australian dollar.

Then the world finds its own new reserve currency and the US empire collapses.

Enter Donald Trump – the man, the legend, the scandalous buffoon – to make the fateful call.