Several groups are urging the federal government’s Retirement Income Review to recommend cutting the taper rate for the pension assets test, which was raised from $1.50 to $3.00 in 2017:

The taper rate is part of the assets test used to determine eligibility for the age pension. For every $1000 of assets above the relevant threshold, the age pension payment tapers off (or is reduced) by $3 a fortnight…

In 2017, Scott Morrison (who was then social services minister) presided over a change which made the taper rate significantly steeper, rising from $1.50 to $3…

Industry Super Australia wants the taper rate reduced from $3 to $2, which would expand access to the part age pension to couples with just over $1 million in assets, up from about $877,500 at present…

The Council on the Ageing, better known as COTA, is urging the retirement income review panel to look closely at the taper rate for the assets test.

“Some argue there is a clear disincentive to save, leading to over-investing in the family home, or gifting to family members, or engaging in major discretionary expenditure that they would not otherwise have done,” COTA’s submission says.

“We note that the Actuaries Institute, Rice Warner and the Grattan Institute are all calling for the taper rate to be reassessed and softened…

But others, including the Centre of Excellence in Population Ageing Research (CEPAR) at the University of NSW, say steep taper rates are the best way to direct scarce government resources to those who need them most.

“[Research shows a] sharp taper is superior to a shallow taper, and any means-testing is superior to a universal pension,” CEPAR’s submission says.

It is important to note that the pension taper rate was merely restored to what existed prior to when Peter Costello halved it in 2006 – i.e. it was returned to $3 per $1,000 of assets over the threshold from $1.50.

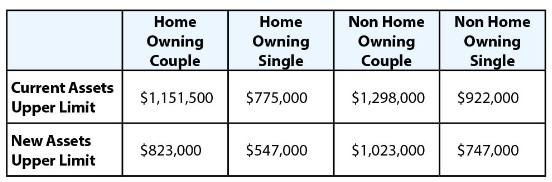

Costello’s halving of the taper rate to $1.50 led to the ridiculous situation where retiree home owning couples with $1.15 million in financial assets, and home owning singles with $775,000 of financial assets, could still qualify for the part Aged Pension along with the Pensioner Concession Card.

The Coalition’s 2017 changes to the taper rate back to its pre-2006 level of $3 per $1,000 in assets meant that some financially wealthy retirees no longer qualified for the Aged Pension (but got to keep their concession cards):

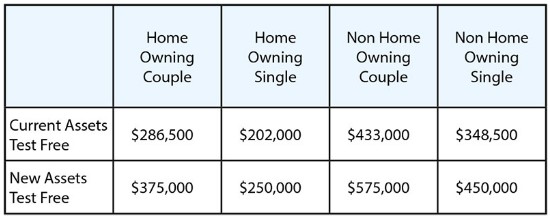

However, the financial situation of pensioners with fewer financial assets was also improved via an increase in the assets test:

Therefore, the Aged Pension was arguably made fairer by these reforms, benefiting those at the lower end of the asset distribution.

While there is probably a case for a middle ground – for example, the Grattan Institute has suggested the taper rate be cut to $2.25 per fortnight for each $1,000 of assets above the threshold – this should only take place in concert with abandoning the scheduled lift in the superannuation guarantee to 12%, alongside reforming Australia’s superannuation concessions so that they are made progressive.

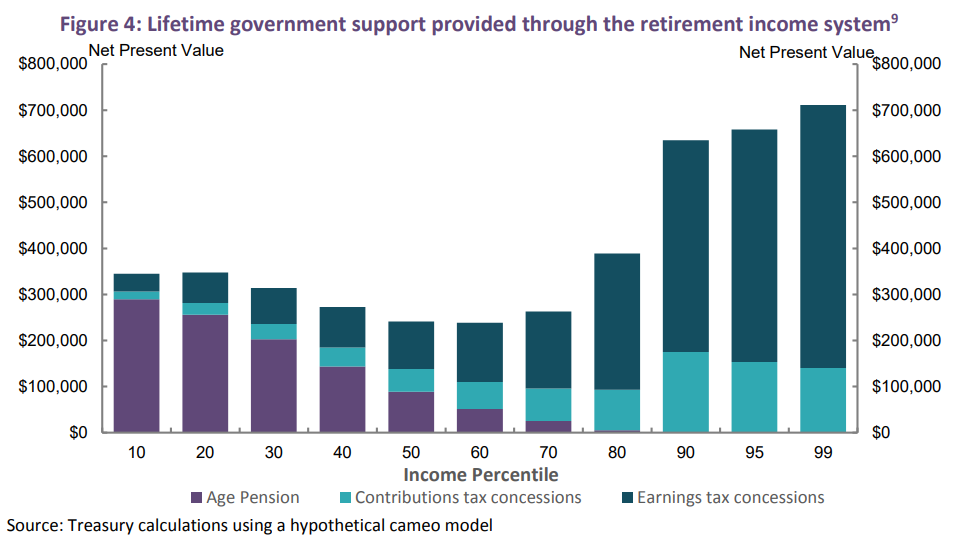

Superannuation concessions cost the Budget $43 billion a year and are very poorly targeted to high income earners, who receive the lion’s share of taxpayer assistance:

This poor targeting of tax concessions means that Australia’s superannuation system costs the federal budget more than its saves in Aged Pension costs, as noted explicitly by the Henry Tax Review:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

The Grattan Institute noted similar:

…both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments:

By extension, the current superannuation arrangements means there are less funds available in the Budget to lift the Aged Pension.

Reforming the superannuation system so that it better targets concessions towards those in need would lighten the cost on the federal budget, leaving funds available to cut the taper rate for the Aged Pension.

Ultimately, it is the high cost of superannuation concessions that is preventing the pension from being lifted.