Via Michael Wilson, Morgan Stanley chief equity strategist:

Almost two years ago, we published a report titled The Great Cycle Debate. In that report, I argued that US equities were likely to experience a cyclical bear market that would take several years to complete. This bear market would play out as a consolidation rather than a wipeout, affecting different stocks and sectors at different times. I later called it a rolling bear market that would leave both bears and bulls unsatisfied.

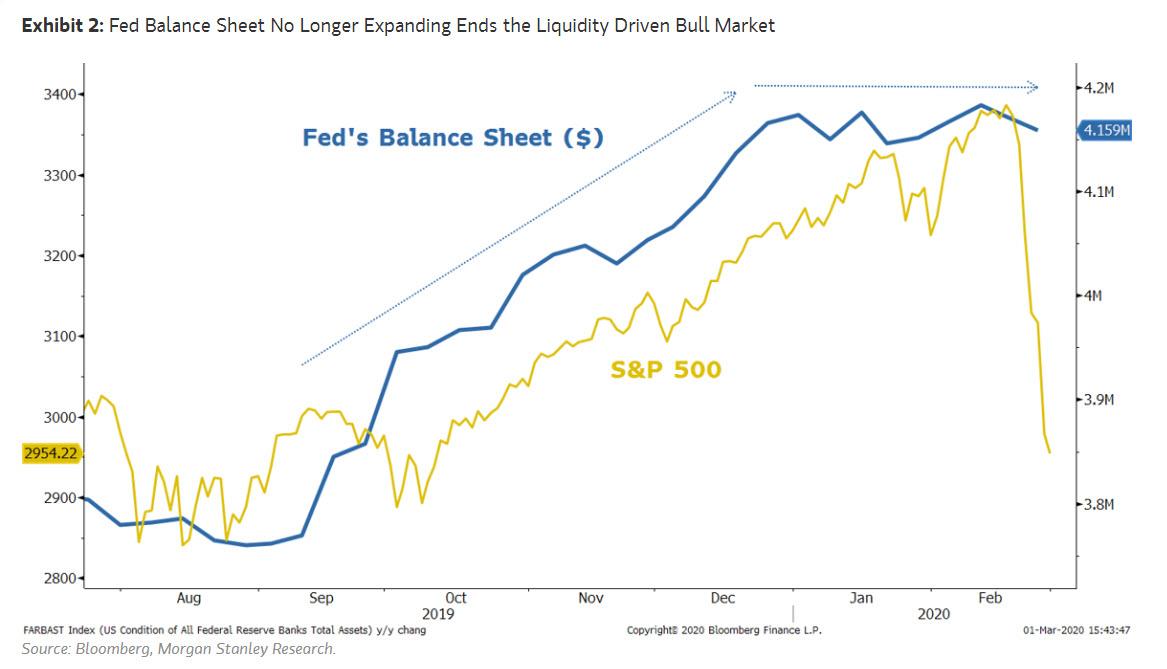

I always viewed last year’s 4Q rally as more about liquidity than fundamentals and thought it could last into April/May when the Fed was scheduled to curtail its latest balance sheet expansion program. However, the unexpected COVID-19 outbreak has brought that timing forward, and the recent correction in equity markets makes the entire rally since last October look like a false breakout.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.