Stephen Koukoulas (“the Kouk”) has once again claimed that housing affordability is no worse today than 20 or 30 years ago:

About 30 years ago, 20 years ago and 10 years ago, a median income household buying a median priced house with an 80% LVR paid around 22-25% of their disposable income to pay off a house in 25 years.

Today, those numbers are pretty much unchanged.

I find that interesting.— Stephen Koukoulas (@TheKouk) February 18, 2020

As usual, The Kouk has focused on one thing only – initial mortgage repayments – while ignoring all other factors, including:

- The size of the deposit required;

- Repayment size over the full 25 to 30 year loan term; and

- How long it take to repay the mortgage.

I comprehensively debunked the Kouk’s faulty methodology in 2016.

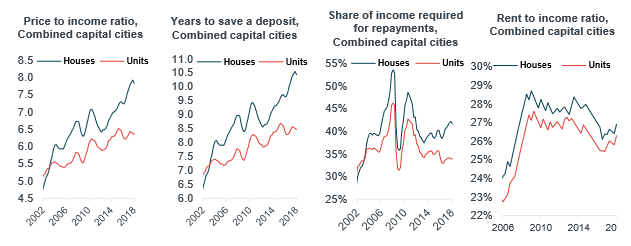

CoreLogic has also debunked The Kouk’s claim, showing that the number of years required to save a deposit has ballooned:

In short, today’s home buyer are facing a difficult loan repayment schedule due to the combination of high home prices, low inflation and low income growth.

Because of these factors, a massive mortgage today will remain a very big mortgage in a decade’s time.

Der.