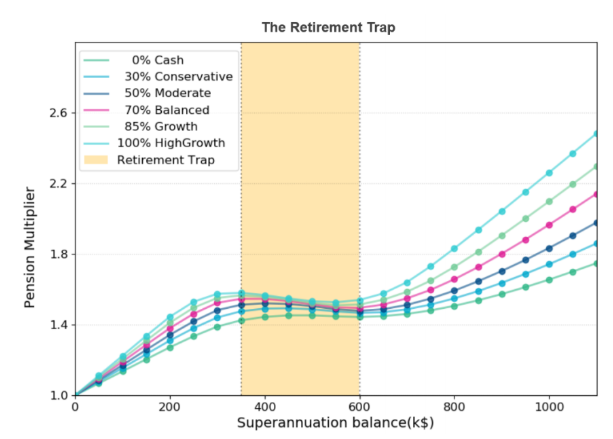

The fake outrage of the Aged Pension taper rate has continued in the New Daily, which claims that the tightened pension assets test is leaving a growing number Australians in a “retirement trap”:

Research by exchange-traded fund provider BetaShares found Australians with super balances between $350,000 and $600,000 at retirement age can shrink their income accidentally by saving more.

The “ironic” problem is caused by the pension asset test, which progressively decreases the benefits pensioners can receive based on their wealth…

“Common wisdom tells us that accumulating more savings through our working lives should result in higher income in our retirement years,” Dr Cohen said.

“However, our analysis shows that, for certain people, under the current system, accumulating more money can actually produce the reverse”…

“The transition from full entitlements to the age pension to no entitlements needs to be smoother,” Dr Cohen said.

What the article conveniently fails to mention is that the pension taper rate was merely restored to what existed prior to when Peter Costello halved it in 2006 – i.e. it was returned to $3 per $1,000 of assets over the threshold from $1.50.

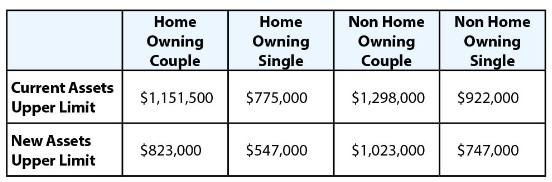

Costello’s halving of the taper rate to $1.50 led to the ridiculous situation whereby retiree home owning couples with $1.15 million in financial assets, and home owning singles with $775,000 of financial assets, could still qualify for the part Aged Pension along with the Pensioner Concession Card.

Advertisement

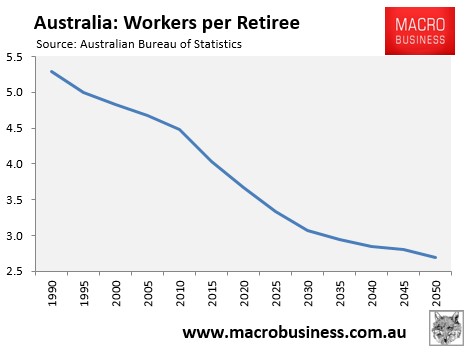

Accordingly, welfare was being lavished on a significant number of wealthy retirees – an unsustainable and inequitable situation given the rapid ageing of the population and the projected diminishing number of workers available to support retirees (see next chart).

The Coalition’s 2017 changes to the taper rate back to its pre-2006 level of $3 per $1,000 in assets meant that some financially wealthy retirees no longer qualified for the Aged Pension (but got to keep their concession cards):

Advertisement

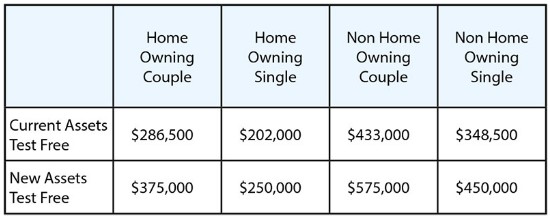

However, pensioners with fewer financial assets were also made better-off via an increase in the assets test:

Advertisement

Thus, the Aged Pension was arguably made much fairer, benefiting those at the lower end of the distribution.

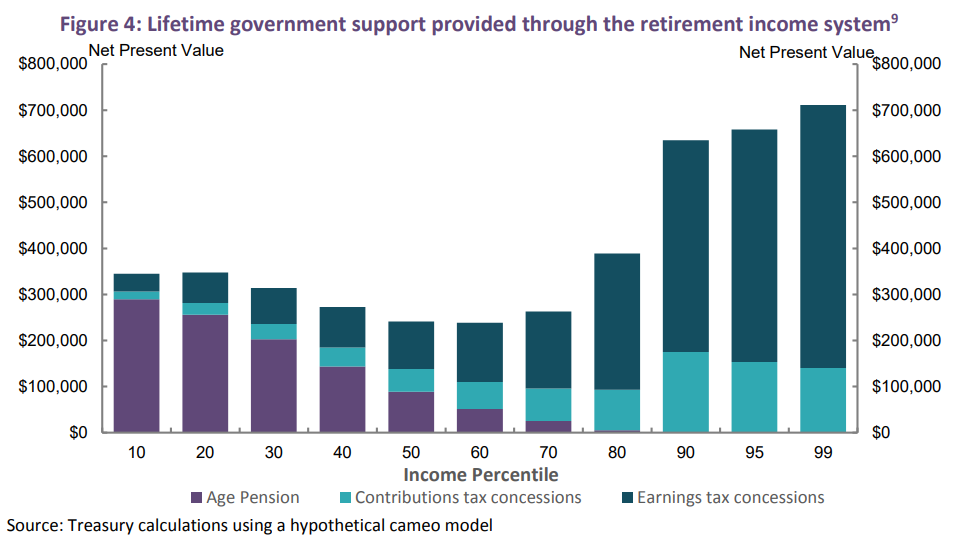

One thing that is also conveniently ignored is that Australia’s superannuation system is effectively preventing the Aged Pension from being lifted.

This poor targeting of tax concessions means that Australia’s superannuation system costs the federal budget more than its saves in Aged Pension costs, as explicitly noted by the Henry Tax Review:

“An increase in the superannuation guarantee would … have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in Age Pension costs).”

…both the short and long term, superannuation tax breaks cost the budget more than they save in pension payments:

It also means that there are less funds available in the Budget to lift the Aged Pension.

Advertisement

Put another way, if the superannuation system was abolished, the Aged Pension could be lifted significantly without creating any net costs to the Budget.

It would also make the retirement system more equitable and efficient, since higher-income earners would no longer receive the bulk of taxpayer’s support and overall administration costs would be significantly lowered.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.